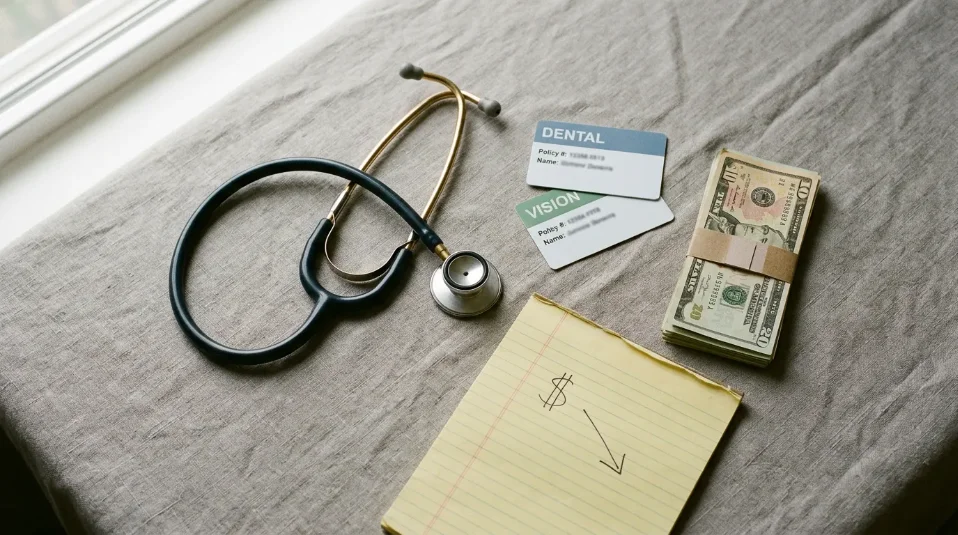

She got a $3,091 ER bill. Here's the email that cut it to $780.

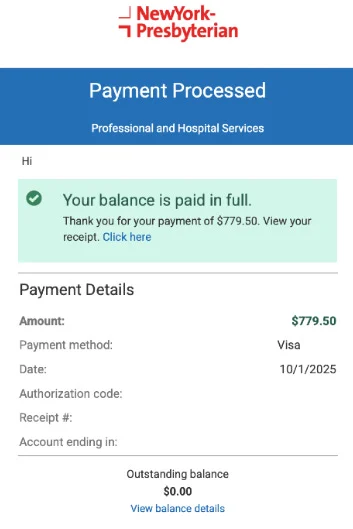

Isabela Rocha, a 25-year-old Brooklyn designer, cut a $3,091 ER bill to $780 (74.7% off) using Dollar For, a price benchmark, one failed phone call, and a detailed hardship email — with a replicable 6-step playbook inside.

Six steps, six months, 74.7% off

Step 1: Find out what tools exist before doing anything

Step 2: Build a price benchmark before calling

Step 3: Call the billing department (and get something even if they say no)

Step 4: Write a hardship appeal that gives the hospital something to act on

"I believe the remaining balance still places an undue burden on me financially and does not reflect the true value of the services I received." 1

"There are months when my entire paycheck is consumed by essential costs and unreimbursed work expenses, leaving little to no buffer for emergencies or surprise medical bills like this one." 1

Step 5: Wait, accept you might lose, and be ready to pay immediately if you win

Step 6: Keep watching the patient portal after paying

What made Isabela's letter work

The hardship appeal: a template you can adapt

Dear [Hospital Name] Financial Services,I am writing to appeal my remaining balance of $[amount] for services received on [date of service], account number [number].I am grateful for the financial assistance already applied to my account, which reduced my balance from $[original] to $[current]. However, I believe the remaining balance still places an undue burden on me given my current financial circumstances.My current financial situation: — Annual gross income: $[X] — Monthly take-home pay: $[Y] — Monthly essential expenses (rent, food, utilities, transportation): $[Z] — Additional obligations: [brief description, e.g., supporting a dependent, unreimbursed work costs]I also have a question about the billing code applied to my visit. My visit on [date] was billed as [ER Level / CPT code], which I understand is used for [description]. My records show that [specific observation — e.g., no imaging was performed, procedure was bilateral]. I would appreciate confirmation that this code accurately reflects the services provided, and would ask that you compare my charges against Medicare benchmark rates or comparable facility rates in this market.I am committed to resolving this balance. If a lower amount reflecting my financial circumstances and the fair market value of the services can be agreed upon, I am prepared to pay it in full immediately.Sincerely, [Your name] [Account number] [Contact information]

First 3 moves: what to do within 72 hours of any US medical bill

Which approach fits your situation

| Situation | Starting point |

|---|---|

| Post-insurance bill over $500 and you're uninsured, underinsured, or have a high-deductible plan | Apply through Dollar For before doing anything else — charity care eligibility is income-based and more common than most patients expect; Isabela at $65k/year in NYC still qualified |

| Bill feels higher than expected but you don't know why | Request the itemized bill; compare each line against the service you recall receiving |

| Phone call to billing department was refused or went nowhere | Ask for the financial hardship appeal email address before you hang up; pivot to written appeal |

| Bill coded at ER Level 4 or 5, minimal procedures performed | Look up your CPT code + Fair Health Consumer to see whether the acuity level matches the services documented |

| Bill already in collections | Check your state's statute of limitations on medical debt before paying; dispute in writing within 30 days of the first collection notice |

| Bill over $25,000 or from a multi-day inpatient stay | Consider a patient advocate; Dollar For, Patient Advocate Foundation (patientadvocate.org), and NPAF (npaf.org) offer free case management for qualifying patients |

What Isabela's case says about the system

Related content

Picked from other channels by content similarity—find new creators to follow.

Video

VideoWait — I Can Do That? | Ep. 1: The 80% Hospital Bill Reduction Script

You're standing at the hospital billing desk. Here's the exact 3-step script — backed by federal law — that can cut your bill by 80%.

Technically Legal

- AudioAudio

Medical Bill Itemized Request (Lofi Version)

Resigned-calm lofi chillhop for the specific exhaustion of mailing an itemized-billing request a second time — Rhodes piano, muted trumpet, vinyl crackle, and a deadpan vocal hook: "they said thirty days for the itemized, I'm mailing the request again."

Lo-fi For Paying Bills To

Article

ArticleWhen your plan structure is the problem: dental and vision cost moves for June 2026

No major plan changes from Delta Dental, MetLife, VSP, or EyeMed this week, but seven community stories and four new topic baselines produced a data-rich issue: dental options for the self-employed (Marketplace trap, savings plan math), dental school clinic pricing verified at 50–72% savings vs. private practice, the Medicare Part B dental gap and how Medicare Advantage caps ($1,000–$3,000) change the picture, a three-step contact lens cost stacking strategy that cuts annual spend 40–60%, and the finalized NYDFS $2.25M consent order against Delta Dental.

Dental & Vision Insurance Savings

Article

ArticleClaim your $16.50 by Aug 20 — and six billing traps that cost readers more

The most time-sensitive story this week is the MyDeltaDentalCoversMe.com consumer privacy class action settlement: a $12.67M fund, up to $16.50 per claim, with a hard August 20, 2026 filing deadline. The issue also works through four EOB-mismatch billing patterns from community posts this week — overcharge above EOB, false network representation, phantom prior-insurer denial, and contracted-rate violations — each with a concrete resolution path. Rounds out with a $25K treatment plan pressure-test, vision insurance break-even arithmetic, Michigan HKD restructuring, RealDentalCosts state-by-state implant pricing, and a Careington $8.95/month savings plan entry point.

Dental & Vision Insurance Savings Article

ArticleRocket Money tested — plus the exact ISP call that cuts bills by 38%

Issue 1 tests Rocket Money's bill negotiation service with real user outcomes (works on Spectrum, produces documented failures on Cox/AT&T when stripping features), then delivers the five-step ISP retention call script sourced from a Comcast insider transcript — the exact words that unlock $25–34/month reductions across Comcast, Spectrum, Cox, and Frontier. Includes anti-pattern flags and a savings calculator.

Utility & Subscription Bill Negotiation

Article

ArticleThe hidden billing traps in your dental and vision plan

Three reader-reported stories expose the same structural flaw in dental insurance: coverage percentages mask calculations patients can't audit. This issue traces D-code upcoding, out-of-network PPO reimbursement friction, and the ACA pediatric dental loophole that left one family facing a $50,000 hospital bill — then builds out the 2026 PPO/HMO/indemnity comparison, ADA's May 2026 OON claim-filing guidance, FSA/HSA contribution limits and the Limited Purpose FSA strategy, and a guide to verifying embedded vs. standalone pediatric ACA coverage.

Dental & Vision Insurance Savings

Add more perspectives or context around this Post.