Three June 2026 switches: $1,200, $1,752, and $2,340 saved

Three publicly disclosed Reddit switch cases from May 27 – June 3, 2026 show drivers cutting $1,200 to $2,340 per year without reducing coverage — set against a soft market where none of the six major carriers filed rate changes in 30 days, and three states (NY, IL, OK) enacted consumer-protection rate reforms. Includes the four-step pre-flight checklist, life-stage quoting benchmarks, the retention-department gambit, and three anti-patterns.

No major carrier filed a rate increase in May. The industry just finished its best underwriting quarter in 25 years. And three drivers publicly documented switching out of Geico and State Farm — saving $1,200 to $2,340 per year without cutting a single limit. The market is calm. That's the best time to shop.

Rate climate: soft market, no new hikes filed

In the 30 days ending June 3, 2026, none of the six major carriers — Geico, Progressive, State Farm, Allstate, Liberty Mutual, or USAA — filed a rate increase or decrease with state regulators. 1 The national average full-coverage premium is $2,236 per year ($186/month) as of June 2026 — essentially flat from the May 27 checkpoint of $2,238. 1

The backdrop: the U.S. P/C industry posted $22.1 billion in underwriting profit in Q1 2026 — the best first-quarter result in 25 years. 2 Rates peaked at $2,294/year in March 2025 and have since declined about 6% through 2025 before stabilizing. 1 Insurify projects 2026's full-year increase at just 0.6% — the smallest since 2022. 1

Three legislative shifts from the past week affect what future renewals will look like:

- New York (signed May 27–28): Governor Hochul's auto insurance reforms ban certain rating factors (occupation, education, housing tenure), require 30-day advance notice for renewals with 10%+ increases, and create an excess-profit refund mechanism. The Citizens Budget Commission estimates a ~10% premium reduction for New York drivers, who currently average $1,896/year — 32% above the national average. 3

- Illinois (passed May 29, pending governor signature): gives the state insurance department authority to review and reject excessive rate filings before they take effect, plus 30-day advance notice for 10%+ renewal increases. Illinois had operated under open-competition rules since 1971. 4 State Farm publicly opposed the change, warning it "will undermine rate predictability, market stability, and reduce competition." 5

- Oklahoma (signed May 14, effective July 1, 2027): shifts from use-and-file to file-and-wait, giving the insurance commissioner authority to reject filings before they take effect. 6

None of this changes a quote you can pull today. But if you're in New York, Illinois, or Oklahoma, the regulatory tide is now running toward more consumer notice before your next renewal hike.

One carrier highlight: Progressive is returning nearly $1 billion to approximately 2.7 million Florida policyholders under the state's excess-profit law, averaging about $300 per policy. 7 If you hold a Progressive auto policy in Florida and had active coverage as of December 31, 2025, check your mail for a check or billing credit.

Three cases from this window

All three meet the hard filter: both old and new premiums publicly disclosed by the policyholder, annual savings of at least $300, coverage confirmed equivalent (or explicitly stated as same coverage), and switch path named. Window is May 27 – June 3, 2026, with one case expanded to the nearest qualifying post.

Case 1: Geico → Travelers, Maryland, 2013 Hyundai Sonata, ~$1,200/year saved

Driver profile: u/InvestmentMindless41 on r/Insurance. Location: Maryland. Vehicle: 2013 Hyundai Sonata with software anti-theft lock. No at-fault accidents, no moving violations. Two theft-attempt claims filed in October 2025. 8

| Geico (old) | Travelers (new) | |

|---|---|---|

| Monthly premium (pre-claims) | ~$300 | — |

| Monthly premium (post-claims) | >$500 | ~$400 |

| Annual savings vs. post-claims Geico | ~$1,200+/year |

Switch path: Geico raised the monthly premium from ~$300 to over $500 following two theft-attempt claims in the same month, citing the vehicle as "high risk." The driver shopped independently and switched to Travelers, landing just under $400/month with equivalent coverage. 8

"I was previously with Geico paying ~$300/month then I had two attempted thefts in the same month last October, both of which I had to file claims for. Fast forward a few months and they raised my rate to over $500/month and said it was because my vehicle is high risk. I then switched to Traveller's last month and am now paying just under $400/month."— u/InvestmentMindless41 8

Coverage note: The driver did not detail the specific liability limits on both policies. Coverage equivalence is stated as intent ("sought the same protection") but is unconfirmed at the limit level — flag this if you're in a similar post-claim situation. Verify that UM/UIM, comp/collision deductibles, and liability limits match before binding.

Post-claims context: The $1,200/year savings is measured against Geico's inflated post-claim rate of $500+/month, not the original $300/month baseline. The real story is escaping Geico's theft-claim surcharge by moving to a carrier that priced the same risk differently. At $400/month, this driver sits above Travelers' national average of $1,664/year ($139/month), 9 which likely reflects Maryland's above-average rates and the two recent claims.

Loading content card…

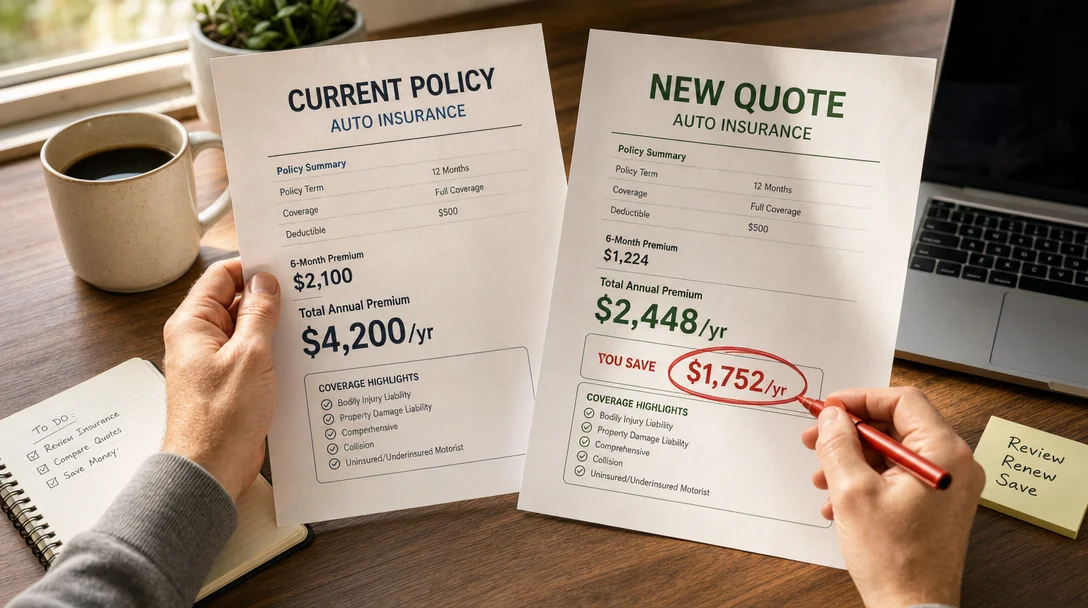

Case 2: Geico → Progressive, New York, two paid-off vehicles, ~$1,752/year saved

Driver profile: u/Dry-Week1919's brother and his wife, r/Insurance. Location: New York state. Vehicles: two average 10-year-old paid-off cars. No credit tier disclosed. Clean driving record implied. 10

| Geico (old) | Progressive (new) | |

|---|---|---|

| Monthly premium (couple, 2 vehicles) | $350 | $204 |

| Annual premium | ~$4,200 | ~$2,448 |

| Annual savings | ~$1,752 |

Coverage equivalence: explicitly confirmed. The OP stated the new policy carries "Same Injury/Property/Liability numbers." 10

Switch path: direct carrier-to-carrier comparison online. The OP's brother obtained a Progressive quote and switched in one step. Worth noting: in the same thread, u/Dry-Week1919 (the OP) was personally paying $330/month at Geico after 16 years of zero claims and zero violations, and held a Progressive quote of ~$200/month — a $1,560/year gap for a clean 16-year record. 10

"So my brother basically has the exact same policy with his wife with Geico just went to Progressive and is paying 204$ a month from Geicos 350 in 6 months."— u/Dry-Week1919 10

One warning to carry into your own switch: u/LeadershipLevel6900, who identified themselves as a former Geico employee, explained in the same thread: "Progressive also notoriously has a great new customer discount and then the first renewal comes…people then frequently come to this sub to ask what happened." 10 The first-year savings are real. Set a calendar reminder to re-quote 45 days before your first Progressive renewal.

Loading content card…

Case 3: State Farm → Travelers, Kansas, 65-year-old male, 2015 Toyota Highlander, ~$2,340/year saved

Driver profile: u/Material_Cook_4698 on r/Insurance. Location: Kansas. Age: 65. Vehicle: 2015 Toyota Highlander. Clean record. Switch occurred approximately four years ago (~2022); current renewal comparison verified June 2026. 11

| State Farm (old) | Travelers (current) | |

|---|---|---|

| Monthly premium at switch (~2022) | $280 | $95 (paid 6-month full) |

| Monthly premium today (Jan 2026 SF quote vs. June 2026 Travelers renewal) | $310 | $115 |

| Annual savings today | ~$2,340 |

Coverage equivalence: explicitly confirmed. The driver stated Travelers quoted "same coverage" at initial switch and has maintained that equivalence through renewals. 11

Switch path: a neighbor's recommendation → called Travelers directly → received a $95/month quote with 6-month prepay → switched. State Farm's agent has called approximately every six months attempting to win the business back. The most recent State Farm quote (January 2026) came in at $310/month. The current Travelers renewal is $115/month. 11

"Got a tip to call Travelers from my neighbor. Their quote four years ago for same coverage was $95/mo with paying full 6 months premium. My policy is renewing in June for $115/mo."— u/Material_Cook_4698 11

"About once every 6 months my old SF agent calls to get me back, he runs the SF numbers, and nope. Last Jan 2026 – July quote was $310/mo. I ain't never going back!"— u/Material_Cook_4698 11

This case's value is the four-year view. Travelers' initial $95/month rose to $115 — a 21% increase over a period when the national average climbed more than 40%. State Farm's quote for the same driver moved from $280 to $310. The gap widened, not narrowed. Staying with State Farm through those four years would have cost roughly $9,360 more than staying with Travelers.

Note on case timing: the switch itself occurred around 2022, predating the 2022–2024 rate spike. The current rate comparison (January 2026 State Farm vs. June 2026 Travelers) is fresh, but switching logistics at both carriers may differ from four years ago.

The four-step pre-flight checklist

Run all four before requesting any quote. Skipping one is how savings become surprises.

Step 1 — Pull your credit score. Credit-based insurance scoring applies in 46 states. Insurify's June 2026 data shows drivers with excellent credit averaging $131/month for full coverage; poor credit averages $191/month — a 46% premium on the same vehicle and coverage profile. 1 Know your tier before you quote. NerdWallet's June 2026 carrier comparison shows State Farm's rate for a driver with poor credit at $8,322/year versus $2,120/year for good credit — the steepest penalty of any major carrier. 9 If your credit is below good, start your comparison with carriers that weight credit less heavily: Progressive, American Family, or a telematics-based program that overrides credit with driving behavior.

Step 2 — Lock your current coverage limits. Pull your declarations page and write down every field: bodily injury liability (per person / per accident), property damage liability, UM/UIM limits, comprehensive and collision deductibles, and any add-ons (rental reimbursement, roadside, gap coverage). Each new quote must match these fields exactly. A quote that drops UM/UIM or cuts liability from 100/300 to 50/100 is not a comparable quote — it's a coverage reduction dressed as savings.

Step 3 — Document continuous coverage. A lapse of 30 or more days — from a missed payment, a gap between policies, or a period without a vehicle — can trigger a higher-risk pricing tier at any new carrier. Have your current policy's effective dates and a proof-of-prior-insurance letter ready before binding anything new. Insurify data shows a coverage gap can raise your rate by up to 25%. 1

Step 4 — Protect multi-car and bundle discounts. If you currently bundle home + auto or have two or more vehicles on one policy, quote the full household at the new carrier — not just the car you want to move. Quoting a single vehicle and switching it will typically break the multi-car discount on the remaining policies, erasing part of the apparent savings before the math even closes.

Quote-shopping path by life stage

Benchmark rates from Insurify, NerdWallet, and ValuePenguin's June 2026 data, organized by driver category.

25-year-old single driver. Your age bracket averages $196/month nationally. 1 Travelers and Geico each hold the cheapest full-coverage rate in roughly 12 states. 12 Start with both, plus any independent agent who can access Auto-Owners or USAA. If your record is clean, Progressive's Snapshot telematics program frequently produces 10–20% discounts for young drivers who demonstrate safe behavior.

30s family, multiple vehicles. NerdWallet's June 2026 baseline for a 35-year-old: Travelers at $1,664/year and Progressive at $2,006/year for full coverage on a single vehicle. 9 Multi-car discounts run 10–25% depending on carrier. Quote all vehicles and all drivers together — separating them misses the household discount structure. An independent agent can run Travelers, Allstate, and American Family simultaneously.

50s household, two cars. Drivers in their 50s average $122/month nationally. 1 Case 3 is directly applicable: Travelers has beat State Farm's quote for the same driver on the same vehicle for four consecutive renewal cycles. Run that comparison in your state. If you have excellent credit, also quote USAA (if eligible) and Auto-Owners — both rank among the cheapest five in Insurify's 37-carrier table. 2

65+ retiree, low mileage. Average full-coverage rate at 65 is approximately $115/month nationally. 1 NerdWallet's June 2026 data: USAA at $1,584/year and Travelers at $1,664/year nationally. 9 If you drive under 7,500 miles per year, ask each carrier explicitly about low-mileage programs — the standard quote won't automatically reflect your usage. State Farm's Drive Safe & Save caps at 30% off for very low-mileage drivers.

The retention-department gambit

Before completing any switch, call your current carrier's retention department — not general customer service — and give them the lowest quote you have in hand. Name the carrier, the coverage limits, and the annual premium. Ask if they can match it.

Insurance companies don't "price match" the way a retailer does — rates are actuarially set and filed with state regulators. What retention departments can do is apply discounts you're not currently receiving (loyalty tiers, multi-policy adjustments, telematics enrollment) or flag that your profile now qualifies for a lower rate tier. 13 As u/Sam_At_Insurify (an Insurify employee) noted: "Some insurers have retention departments that can offer adjustments, but most won't beat a competitor's quote outright. If they do offer something, get it in writing before canceling on the new insurer." 13

Three things to know going in:

- An adjustment is most likely when your competing quote comes from a major national carrier with identical coverage limits — retention reps can verify it, and they know losing a long-tenure customer costs more than a modest discount.

- Some carriers have mid-term pricing rules that prevent changes until renewal. If you're told to call back at renewal, set a calendar reminder for 45 days before that date.

- If they won't adjust, your savings case is confirmed. Set your new policy start date equal to your old policy end date — same day, no gap — then cancel in writing.

Switches you should not make

Three documented anti-patterns from this week's research.

Letting your policy lapse on a billing quirk. A GM Insurance (OnStar product) customer this week found their policy lapsed because GM attempted to charge the renewal premium on the exact expiration date — a Sunday before a holiday weekend, with customer service closed and the online portal locked. 14 The driver had to bind a new policy immediately. As u/sarinavoss noted: "Even a one-day gap shows up on your CLUE report and follows you around on every quote for the next 3-5 years." 14 Set your auto-pay renewal at least 7 days before expiration, not on expiration day.

Switching mid-claim. If you have an open claim with your current carrier, do not switch until it closes. The new carrier did not underwrite the incident. Switching mid-claim doesn't transfer the claim — it just creates two policy relationships to manage on the same event. Wait for the claim to close, then shop.

Letting an unverified vehicle drag your bundle into cancellation. A Georgia driver this week received a State Farm termination notice for their home/auto/umbrella bundle because a 2008 Toyota sitting unused in the driveway had never been formally removed from the policy. 15 State Farm's notice cited "insufficient underwriting information." When you take a vehicle out of service, remove it from your policy in writing and confirm the change. A phantom vehicle is an underwriting question mark that can cascade into a full-bundle cancellation.

Cover image: AI-generated illustration.

References

- 1Insurify: Average Cost of Car Insurance (June 2026)

- 2Insurify: Compare Car Insurance Rates Online (2026)

- 3Insurance Journal: NY Lawmakers Agree to Governor's Auto Insurance Reforms in New Budget

- 4Insurance Journal: Illinois Passes Legislation to Give Insurance Department Oversight of Rate Changes

- 5State Farm Newsroom: Understanding the Issues in Illinois

- 6Insurance Journal: New Law Requires Insurance Rate Filings in Oklahoma to Undergo Review Process

- 7The Zebra: What to Know About Florida Car Insurance Refunds

- 8r/Insurance: Should I report a theft to my insurance

- 9NerdWallet: Average Cost of Car Insurance in 2026

- 10r/Insurance: What's up with the recent massive surge of policy holders going to Progressive from Geico

- 11r/Insurance: Best Auto Insurance??

- 12ValuePenguin: 10 Cheapest Car Insurance Companies (June 2026)

- 13r/Insurance: Car Insurance Increase

- 14r/Insurance: GM car Insurance Lapsed and can't renew today

- 15r/Insurance: State Farm sent a letter terminating my home/auto/umbrella insurance

Related content

- Sign in to comment.

More from this channel

- July 1: shop the quote, not the teaser

- June 24: 14-week filing drought, a 40% rate shock, what you forfeit

- Three switch cases for June 17, 2026: $1,178, $7,000+, and the one that was right not to happen

- Three June 2026 cases: $500, $1,500, $4,440 saved

- Three May 2026 switches: $720, $1,500, and $1,800 saved

- Three drivers saved $375–$4,200 by switching auto insurance — here's exactly how they did it