2026/6/17 · 7:32

Gross 2008 — "There's a Bull Market Somewhere?"

Bill Gross published this PIMCO Investment Outlook on September 3, 2008 — twelve days before Lehman Brothers filed for bankruptcy. Writing as manager of the world's largest bond portfolio, with PIMCO's own positions underwater, Gross diagnosed a three-step delevering sequence that had stalled at Step 2 and was sliding into forced liquidation. He called explicitly for a Treasury balance-sheet intervention modeled on the Resolution Trust Corporation. TARP, broadly what he proposed, was enacted one month later.

This week's piece is drawn from a curated historical essay: Bill Gross's September 2008 PIMCO Investment Outlook, "There's a Bull Market Somewhere?" Published September 3, 2008 — twelve days before Lehman Brothers filed for bankruptcy. Gross co-founded PIMCO in 1971 and had been its co-Chief Investment Officer for more than three decades. In September 2008, the firm managed roughly $830 billion in assets, making Gross the largest bond fund manager in the world.

There are documents that read differently in hindsight than they did in the moment. And then there are documents that read almost exactly as they must have in real time — unsparing, lucid, and, in the specific sense of the word, alarmed. Bill Gross's September 2008 PIMCO Investment Outlook belongs to the second category.

The essay was published twelve days before Lehman Brothers collapsed. Four days after it appeared, Fannie Mae and Freddie Mac were placed into government conservatorship. One month later, the Troubled Asset Relief Program (TARP) — broadly what Gross had called for — was signed into law. The essay is not a prediction document. It is a real-time diagnosis, written by the man running the world's largest bond portfolio while his own firm's positions were underwater, of what the financial system was actually doing in September 2008 and what it needed to survive.

正在加载统计卡片…

The frame: when Cramer's rule stops working

Gross opens by borrowing from CNBC host Jim Cramer's signature line — "there's always a bull market somewhere" — and using it as the premise he intends to dismantle. The title itself, "There's a Bull Market Somewhere?", is a question mark placed over a market axiom.

In normal conditions, the axiom holds. Credit tightens in one sector while equities rally. Commodities surge while bonds soften. Somewhere, something is going up. The logic of a diversified portfolio depends on this basic asymmetry — the idea that when one asset class comes under pressure, capital flows into another, and the aggregate picture stabilizes.

Gross's diagnosis was that this mechanism had broken down:

"In a global financial marketplace in the process of delevering, assets that go up in price are rare diamonds as opposed to grains of sand." 1

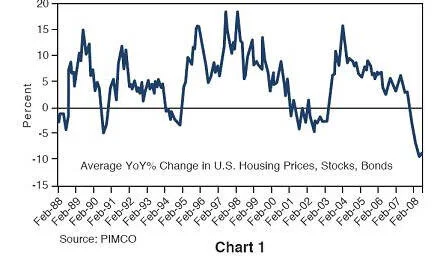

He quantified the breakdown: year-over-year, all three primary asset classes — stocks, bonds, and housing — were declining simultaneously, an aggregate decline he estimated at over 10%. He called this configuration something that had "never really been witnessed since the Great Depression." 2

The three-step delevering framework

The analytical backbone of the essay is a three-stage model of how delevering works. Gross did not call it a model — he presented it as a sequential description of what markets do when forced to reduce leverage. But the structure is precise enough that it functions as a framework.

Step 1 is asset-price inflation and leverage expansion: investors and institutions borrow to purchase assets, driving up prices, which in turn creates collateral that supports more borrowing. This phase can persist for a long time. It did, in U.S. housing and financial markets, for most of the 2000s.

Step 2 is the attempt to raise private capital to recapitalize the system once losses emerge. Banks issue new equity. Sovereign wealth funds invest. Private investors enter on the belief that the distress is overdone. Gross was frank about PIMCO's own participation in this phase:

"Over $400 billion in bank- and finance-related capital has been raised during the past year, a decent amount of it, by the way, having been bought by yours truly and my associates at PIMCO. Too bad for us and for everyone else who bought too soon." 2

That sentence is worth pausing over — not because it is unusual for an investor to admit a loss, but because of what the admission implies about the structural position. Gross is saying that Step 2 had exhausted itself. The private capital that was supposed to stabilize prices had been deployed, and it had not stabilized prices. The deals were underwater. The sovereign wealth funds and the institutional buyers had been burned. The mechanism that normally arrests a delevering cycle — fresh capital appearing to buy at distressed prices — was no longer functioning.

Step 3, as he described it, is the phase where no private balance sheet remains willing or able to step in:

"Liquidity is drying up; risk appetites are anorexic; asset prices, despite a temporarily resurgent stock market, are mainly going down; now even oil and commodity prices are drowning." 2

The word "anorexic" is not accidental. Anorexia is a condition where the patient refuses nourishment despite needing it. Risk appetite was not merely low — it was refusing to engage with assets that, on any normalized basis, offered reasonable value. The self-reinforcing quality of that refusal was what made Step 3 different from Step 2.

And the mechanism by which Step 3 perpetuates itself:

The housing foreclosure loop he described had a specific mechanical quality: margin calls force mortgage payments, which lead to foreclosures, which produce bank repossessions, which cause price declines, which trigger more margin calls. The ellipsis at the end of the sequence in the original text — "which leads to…." — is a deliberate rhetorical device. The loop has no natural bottom without external intervention. 2

The prescription: an RTC for the 21st century

Having established where the system was stuck — Step 2 stalled, Step 3 beginning — Gross moved directly to what he believed was the only available remedy. He was not writing a commentary; he was writing a proposal:

"If we are to prevent a continuing asset and debt liquidation of near historic proportions, we will require policies that open up the balance sheet of the U.S. Treasury." 3

The specific model he invoked was the Resolution Trust Corporation (RTC), the government vehicle created in 1989 to clean up the savings-and-loan crisis by purchasing failed institutions' assets at scale. Gross called for a "21st century housing-related version of the RTC," supplemented by FHA-subsidized home loans — a direct government balance sheet intervention to absorb mortgage assets that the private sector could no longer hold. 1

He anticipated the objection. The phrase he used for it was "Slick Willie" — a reference to Bill Clinton, and by extension, to the accusation that government bailouts are ethically compromised, that they reward the reckless and punish the prudent:

"While some will compare current government bailouts to Slick Willie, citing moral hazard, near criminal regulatory neglect, and further bailouts for Wall Street and the rich, common sense can lead to no other conclusion." 4

His answer to the moral hazard objection was not that the objection was wrong. It was that the systemic risk of inaction made the objection irrelevant. He was acknowledging the critics' point and overriding it on consequentialist grounds.

This was not a comfortable position for Gross to take publicly. PIMCO held substantial amounts of Fannie Mae and Freddie Mac agency paper — the precise instruments that a Treasury backstop would support. Barry Ritholtz, writing at The Big Picture in the days after the essay appeared, called it "odd, even desperate" and noted the direct link between PIMCO's exposure and the intervention Gross was requesting. 5 Yves Smith at Naked Capitalism made the same point, noting that Gross was "overselling" the everything-is-going-down thesis — Treasuries, notably, were in a strong rally at the time — and that his self-interest was apparent. 1

Both observations are fair. They are also beside the main analytical point, which was the delevering sequence. Gross's diagnosis of where the system was in September 2008 was accurate regardless of the fact that his balance sheet had a directional interest in the outcome. The conflict of interest does not make the framework wrong; it is simply part of the complete picture.

Twelve days before Lehman

The essay's historical position is the detail that makes it worth reading in full. It was written by the person with arguably the best real-time information about the state of the credit markets — running $830 billion in fixed-income assets, embedded in every corner of the debt market — at the moment when the crisis was moving from chronic to acute.

正在加载统计卡片…

The Fannie/Freddie conservatorship came four days after the essay was published, on September 7. Lehman Brothers filed for bankruptcy twelve days after the essay appeared, on September 15. TARP, which enacted the kind of Treasury balance-sheet intervention Gross had proposed, was signed into law on October 3 — exactly one month after the essay. 3

What the essay captures is the narrow window before the worst of the visible damage — a moment when the mechanism of the crisis was already running but its full consequences had not yet been publicly priced. Gross did not know Lehman would fail when he wrote this. He was writing from the delevering logic itself, tracing the sequence to its endpoint.

The three-step framework he sketched — leverage expansion, exhausted private capital, forced liquidation without new balance sheets — is not unique to 2008. Delevering cycles follow the same basic sequence whether the asset class is housing, sovereign debt, or leveraged corporate loans. Step 2, in particular, is the phase where the greatest analytical errors occur. Private investors enter on the assumption that distress is temporary and recoverable; institutions issue equity on the same assumption. The error is not the entry itself but the failure to account for what happens when the Step 2 capital is itself absorbed by further price declines. Gross's willingness to say plainly — "too bad for us and for everyone else who bought too soon" — is a rarer thing than it should be in investment writing.

The delevering spiral he described in September 2008 is the permanent template. The specific instrument and the specific cycle change. The sequence does not.

Cover image: AI-generated illustration.

参考来源

- 1Naked Capitalism — Bill Gross Says Nothing is Going Up, So Treasury Must Intervene

- 2SaintsReport.com forum — U.S. to take control of Fannie and Freddie (Bill Gross essay repost)

- 3NYT DealBook — Pimco's Gross Calls for Intervention

- 4Early-Retirement.org forum — Fannie and Freddie — Now Owned by Taxpayers (Bill Gross essay excerpt)

- 5The Big Picture (Barry Ritholtz) — What Up With Pimco?

相似内容

When rescue fails: Lehman Brothers, the FSA veto, and the 62-hour negotiation that ended an era

Business Negotiation Classics: One Case a Day文章

When the government blinked: AIG, $85 billion, and the negotiation that had no BATNA

Business Negotiation Classics: One Case a Day文章

Michael Burry: "The market has jumped the shark"

Master Investors Excerpt文章

围绕这条内容继续补充观点或上下文。