2026/6/26 · 8:23

The $115B deal regulators killed

A business-school-style case study on why the WorldCom-Sprint merger collapsed after DOJ and EU intervention, and how the same Internet-backbone scale that made the deal attractive became its fatal antitrust risk.

In October 1999, MCI WorldCom and Sprint announced a stock-swap merger valued by contemporary reports between $108 billion and $129 billion, with Bernard Ebbers staying on as CEO and Sprint chief William Esrey becoming chairman. 1 Nine months later, the companies abandoned the deal after the U.S. Department of Justice sued to block it and the European Commission declared it incompatible with the common market. 2 3

The managerial lesson is sharper than "regulators said no." WorldCom and Sprint negotiated as if antitrust risk was a closing obstacle. The regulators behaved as if antitrust risk was the deal itself. The asset that made the acquisition attractive, WorldCom's UUNet Internet backbone plus Sprint's own backbone position, was also the asset the regulators were least willing to let the combined company keep.

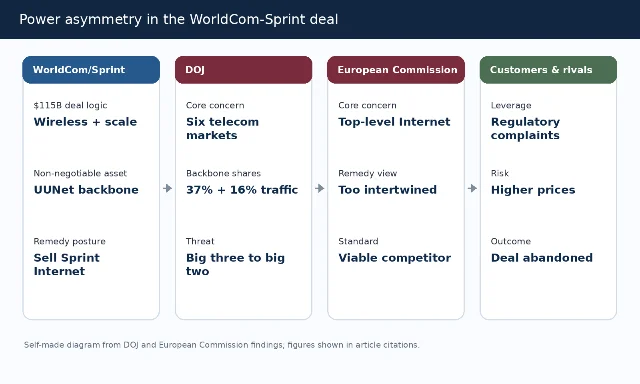

| Player | What the player wanted | What blocked the player | Practical BATNA |

|---|---|---|---|

| WorldCom | Add Sprint's wireless and telecom assets to a company built through roughly 70 acquisitions; keep UUNet as the growth engine. 4 | Regulators saw WorldCom's backbone position as already dominant or close to dominant. 3 | Walk away and look for smaller wireless alternatives. |

| Sprint | Sell into a richer strategic combination while keeping a plausible independent story. 1 | Sprint's Internet business was not cleanly separable from the rest of the company. 5 | Remain independent or invite another buyer with fewer regulatory conflicts. |

| DOJ | Preserve competition across residential long distance, Internet backbone, international services, and enterprise telecom markets. 2 | The parties did not offer a remedy that solved all six markets. 2 | Sue for a permanent injunction. |

| European Commission | Prevent a dominant position in top-level universal Internet connectivity. 3 | The proposed Sprint Internet divestiture did not create a strong standalone competitor. 5 | Prohibit the transaction under Article 8(3). |

Background: a merger built to solve two different problems

WorldCom entered the Sprint talks as a serial acquirer. Bernard Ebbers had built the company through deals, including the 1996 acquisition of MFS, which brought UUNet, and the 1998 acquisition of MCI. 4 Sprint entered with a different problem: it had a national wireless asset in Sprint PCS, a long-distance business, and shareholders who could compare a stand-alone path with competing strategic offers.

The announced bargain tried to satisfy both sides. Sprint's FON long-distance and local shares would be exchanged for MCI WorldCom stock, while Sprint PCS shareholders would receive a new WorldCom PCS tracking stock plus MCI WorldCom stock. 1 The merged company would keep the WorldCom name, report annual revenue above $50 billion, employ about 140,000 people, and hold about 35% of the U.S. long-distance market, close to AT&T's roughly 42%. 1

Sprint had another live option. BellSouth made an unsolicited bid of roughly $100 billion over the October 2-4 weekend in 1999, and BellSouth chairman F. Duane Ackerman negotiated with Esrey before Sprint's board chose WorldCom. 4 Sprint's board viewed the BellSouth path as carrying its own regulatory and strategic complications, including BellSouth's need to enter long distance and overlapping wireless licenses in the Southeast. 1

The public language was pure strategic optimism. Ebbers said, "This merger is about a lot more than wireless," and called the combined company "the most dynamic, most creative, most growth-oriented company in the world." 4 Esrey said, "Each of us had a chance to go it alone, but together we will be more effective competitors." 4 Those statements framed the deal as pro-competitive scale. The regulators would frame the same scale as a market-structure problem.

Decision point 1: owning the network versus renting the option

The first negotiation failure happened before the government filed anything. WorldCom wanted Sprint because Sprint could give it wireless scale and another Internet backbone position. Mark Winther of IDC summarized Ebbers's posture this way: "Bernie doesn't like resale deals, that's not his style. He likes to own it all." 4

That preference mattered because UUNet was not a side asset. It was WorldCom's Internet backbone business and, according to the European Commission's later decision, a central reason the merged company would control top-level universal Internet connectivity. 3 A Wired report captured the company's internal red line before the formal block: an unnamed MCI WorldCom insider said WorldCom would cancel the deal before giving up UUNet because "that's the heart of the growth going forward." 6

The issue was not simply market share. The Internet backbone market depended on peering, traffic exchange, customer reach, and the ability to degrade rivals' connection quality without an obvious refusal to deal. The European Commission later found that MCI WorldCom had 32-36% of global Internet traffic and 40-50% of global Internet backbone revenue, and that the merged company could control 37-51% of traffic depending on measurement method. 3 The Commission also found that MCI WorldCom charged 20-100% higher prices than competitors for equivalent Internet backbone connectivity. 3

For deal-makers, this is the central asymmetry: the buyer's most valuable synergy was also the regulator's core harm theory. A buyer can negotiate price around a marginal asset. A buyer has a harder problem when the remedy demanded by the regulator cuts into the reason the buyer signed.

Decision point 2: when two regulators see different cases

The DOJ filed its civil antitrust suit in U.S. District Court in Washington, D.C., on June 27, 2000, seeking a permanent injunction against the proposed $115 billion merger. 2 The DOJ identified six markets where it said the deal would harm competition: residential long distance, Internet backbone services, international long distance to more than 50 countries, international private lines to more than 60 countries, data network services for large business customers, and custom network services for very large businesses. 2

The DOJ's numbers made the case legible to non-specialists. In residential long distance, WorldCom had about 19% of residential lines, Sprint had about 8%, and the three largest carriers together had about 80%. 2 In Internet backbone services, WorldCom carried about 37% of all Internet traffic and Sprint about 16%, giving the combined company roughly 53%. 2 Attorney General Janet Reno said the merger "threatens to undermine the competitive gains achieved since the Department challenged AT&T's monopoly of the telecommunications industry 25 years ago." 2

The European Commission made a narrower but deeper case one day later. On June 28, 2000, the Commission adopted an Article 8(3) decision declaring the MCI WorldCom/Sprint concentration incompatible with the common market and the EEA Agreement. 3 The Commission focused primarily on top-level universal Internet connectivity and concluded that the deal would create or strengthen a dominant position. 3

Those were not identical theories. The DOJ saw a multi-market horizontal merger that would reduce the big three to the big two in several telecom markets. The European Commission saw an Internet infrastructure bottleneck that could let the combined company set terms for rivals and customers. The parties had to solve both theories, in two jurisdictions, on overlapping but not identical timelines.

Decision point 3: the remedy that did not restore competition

WorldCom and Sprint tried to solve the European problem by proposing to divest Sprint's Internet business on June 8, 2000. 3 The European Commission rejected the proposal because Sprint's Internet business was "completely intertwined with its traditional telecoms activities," and the Commission said the divested business could not be guaranteed to become a strong, viable competitor. 5

This was the practical remedy problem. A divestiture works only if the buyer receives a business that can compete immediately, not a bundle of customers, contracts, employees, network interfaces, and transition-service dependencies that require years of reconstruction. The Commission found that the divested entity would depend on Sprint or the merged company for transition resources for two to four years, and that the separation would carry execution and monitoring risks. 3

The 1998 WorldCom/MCI remedy also weakened the parties' credibility. In that earlier deal, regulators required MCI Internet assets to be sold to Cable & Wireless, and later disputes over that divestiture ended with WorldCom paying $200 million to settle Cable & Wireless claims in March 2000. 7 A regulator evaluating the next Internet-backbone divestiture could not ignore the last one.

Sprint began to signal the problem publicly before the final block. At Sprint's annual meeting on June 13, 2000, Esrey said, "The staff of the Department of Justice has recommended the merger be blocked," and added that senior officials were taking that recommendation seriously. 8 Once a seller starts telling shareholders that the buyer's regulatory theory may fail, the negotiation has moved from price and governance to salvage.

Decision point 4: litigate, restructure, or walk away

After the DOJ sued and the European Commission blocked the transaction, WorldCom and Sprint had three broad choices. They could litigate in the United States while trying to revive the European filing. They could restructure the deal around a much more aggressive divestiture package. Or they could terminate and preserve what remained of management bandwidth and market credibility.

The parties chose termination. On July 13, 2000, WorldCom and Sprint announced that they had called off the merger. 9 Esrey said prolonged delay and uncertainty would not be in the best interest of shareholders, employees, or customers. 10 Ebbers blamed the outcome on what he called "Kennard-Klein policies," a reference to FCC chairman William Kennard and DOJ antitrust chief Joel Klein. 9

The walk-away decision was rational. The legal fight would not have solved the commercial problem that made UUNet non-negotiable. A remedy strong enough to satisfy both regulators could have cut away the growth asset WorldCom cared about most. A remedy weak enough to protect WorldCom's thesis would not clear the regulatory bar.

The market reaction showed the ambiguity. On the day of the termination, WorldCom's share price rose about 8% to $47.94, and Sprint's shares rose to $48. 9 Investors were not simply mourning a lost deal. Some were relieved that the companies had stopped spending time on a transaction that no longer had a credible path to closing.

What the case teaches managers

1. Treat regulatory approval as a negotiated term, not a condition at the back of the agreement

A regulated merger agreement should assign risk before the press release. Modern deal counsel now uses a menu of tools: efforts covenants, reverse termination fees, outside dates, fix-it-first divestitures, express litigation obligations, and interim operating covenants. 11 The WorldCom-Sprint case shows why those clauses are economic terms. They determine who bears the cost when the regulator asks for a remedy that changes the transaction's value.

The negotiation question is not "Will the parties use reasonable best efforts?" The better question is: "Which assets must the buyer be willing to sell, litigate for, or abandon the deal over?" If that list contains the asset that makes the deal attractive, the board should treat the transaction as conditional in substance even if the merger agreement is signed.

2. Build a remedy that a third-party buyer can run on day one

The European Commission did not reject divestiture as a concept. It rejected a divestiture that did not reliably restore competition because Sprint's Internet business was too intertwined with the rest of Sprint. 5 That distinction matters for managers designing remedies.

A viable remedy has four tests: the asset boundary is clear; the buyer can operate without long transition dependence; customers can move without destroying the revenue base; and the regulator can monitor compliance without becoming an operating supervisor. Sprint's proposed Internet divestiture failed too many of those tests.

3. Map veto players by theory of harm, not by agency name

The DOJ and the European Commission coordinated under the 1991 EU-U.S. antitrust cooperation framework, including information exchange and observers at hearings, while still running separate investigations. 12 The parties could not win by convincing one regulator that the other regulator's theory was too broad. The theories had to be solved independently.

This is the map managers should draw before signing: each regulator, each theory of harm, each remedy demanded, and the commercial asset each remedy touches. A transaction is in the danger zone when two regulators attack different parts of the same synergy stack.

4. Remember that rivals can appeal to the referee

Pankaj Ghemawat and Fariborz Ghadar later used MCI WorldCom/Sprint in Harvard Business Review as an example of "appeal to the referee," a strategy in which companies that cannot counter a rival's mega-deal directly can push regulators to open antitrust proceedings. 13 That strategy is not merely legal. It changes the buyer's negotiation environment by adding delay, discovery, remedy pressure, and public narrative risk.

Managers often model the seller, the buyer, and the regulator. They should also model competitors, customers, legislators, and foreign authorities as coalition players. Those players may not sit at the signing table, but they can change the closing table.

What to remember

WorldCom-Sprint was not a case where a good deal met a random political obstacle. The transaction's strategic logic and its antitrust problem were the same fact viewed from opposite sides. WorldCom wanted ownership and scale in backbone, wireless, and long-distance assets. Regulators saw ownership and scale in backbone, wireless, and long-distance assets as the harm.

For deal-makers, the reusable rule is simple: before signing a regulated merger, identify the asset that the buyer refuses to sell. Then ask whether that same asset is the one regulators are most likely to demand. If the answer is yes, the regulatory negotiation has already begun, and the price is only one part of the deal.

Cover image: self-made editorial illustration.

参考来源

- 1The New York Times: MCI Worldcom to Acquire Sprint in Stock Swap Valued at $108 Billion

- 2U.S. DOJ: Justice Department Sues to Block WorldCom's Acquisition of Sprint

- 3European Commission: Case No COMP/M.1741 - MCI WorldCom / Sprint

- 4CNET: MCI WorldCom buys Sprint for $129 billion

- 5European Commission: Commission prohibits merger between MCI WorldCom and Sprint

- 6Wired: Sprint, MCI Merger in Question

- 7Wired: Why the DOJ Killed MCI-Sprint

- 8BBC News: Sprint voices merger fears

- 9Los Angeles Times: WorldCom and Sprint Call Off Merger

- 10CNET: Sprint, WorldCom call off $120 billion merger

- 11Skadden: Managing Deal Risks in a Challenging Regulatory Environment

- 12UC Davis Business Law Journal: Cooperation Between Merger Control Authorities of the EU and the U.S.

- 13HBS Working Knowledge: The Dubious Logic of Global Megamergers

围绕这条内容继续补充观点或上下文。