2026/6/21 · 20:18

Good to Great: what holds, what collapsed

A practitioner close-read of Jim Collins's Good to Great (2001). Collins's central argument unpacked: 1,435 companies screened → 11 selected → seven frameworks claimed as immutable laws. All seven frameworks at operational depth. A company-fate table tracks what happened to all 11 after publication: Circuit City bankrupt, Fannie Mae federally conserved, Wells Fargo erupting in scandal. The critique is unflinching: Rosenzweig's Halo Effect, two AOM peer-reviewed papers calling the methodology "devastating," the survivorship bias argument. Closes with five Monday moves — one per major framework — grounded in what practitioners report actually working.

Jim Collins opens Good to Great: Why Some Companies Make the Leap... and Others Don't (HarperCollins, 2001) with a sentence that reads like a dare: "Good is the enemy of great." 1 He spent five years with a 21-person research team screening 1,435 Fortune 500 companies, whittling the list to 11 that met a strict standard — mediocre performance for 15 years, then a sustained transition to returns at least three times the stock market average for another 15 years. Those 11 companies, Collins argued, had cracked something fundamental: "timeless, universal answers" to why some companies make the leap and others don't. 1 The book sold more than four million copies, became mandatory reading on MBA syllabi worldwide, and lodged seven frameworks into the management vocabulary that practitioners still use today. 2

Then Circuit City — Collins's single best-performing "great" company, which had delivered an 18.5-times market return during the study window — filed for bankruptcy in November 2008. Fannie Mae, another of the 11, was placed into federal conservatorship a month earlier, requiring what would become hundreds of billions of dollars in government bailout funds. 3

That is the tension this book hands you. The frameworks are real and practitioners keep using them. The research method was fundamentally broken. A manager who reads the book as inspiration and a diagnostic lens gets genuine value. A manager who reads it as a predictive playbook gets the Circuit City problem.

Here is what each delivers.

Collins's central argument

The research design had two gates. A company had to show cumulative returns at or below the market average for 15 years — demonstrating it was stuck in mere goodness — and then deliver at least 3x the market return over the following 15 years, demonstrating a transition to greatness. From 1,435 candidates, 11 survived: Abbott Laboratories, Circuit City, Fannie Mae, Gillette, Kimberly-Clark, Kroger, Nucor, Philip Morris, Pitney Bowes, Walgreens, and Wells Fargo. 1 Each was matched with a "comparison company" that operated in the same industry, had similar resources during the transition period, but never made the leap.

Collins's team then conducted 6,000 articles' worth of analysis — executive interviews, financial data, archival research — looking for the patterns that separated the 11 from their direct competitors. What they found, Collins announced, were not transient management trends but "the immutable laws of organized human performance." 2 Seven frameworks emerged. They are worth understanding on their own terms before examining what the critics found wrong with the method.

The seven frameworks

Level 5 Leadership. At the top of a five-level hierarchy sits the "Level 5 leader": someone who combines fierce professional will with deep personal humility. These leaders, Collins found, directed their ambition toward the institution rather than themselves, set up successors for even greater success, and attributed company victories to others while taking personal responsibility for failures. The canonical example is Darwin Smith, who as CEO of Kimberly-Clark sold the company's prized paper mills — "the very definition of the company" — to focus entirely on consumer products. Analysts mocked the move. Kimberly-Clark went on to beat Procter & Gamble, Scott Paper, and Kimberley-Clark's comparison companies over the following years.

"The good-to-great leaders never wanted to become larger-than-life heroes. They never aspired to be put on a pedestal or become unreachable icons. They were seemingly ordinary people quietly producing extraordinary results." 1

First Who, Then What. Before setting a new direction, great companies focused on getting the right people "on the bus" and the wrong people off. Collins inverts the intuitive startup assumption — that you find a vision, then staff to it. His finding: the great companies first built teams of self-motivated, capable people, then figured out where to drive. The implication is that if you have the right people, the motivational problem largely disappears; they will find the best path.

"The executives who ignited the transformations from good to great did not first figure out where to drive the bus and then get people to take it there. No, they first got the right people on the bus (and the wrong people off the bus) and then figured out where to drive it." 1

Confront the Brutal Facts (the Stockdale Paradox). Collins named this principle after Admiral James Stockdale (United States Navy), who survived eight years as a prisoner of war at the Hanoi Hilton. Stockdale's observation, which Collins uses as a management frame: the prisoners who didn't survive were the optimists — the ones who said "we'll be out by Christmas" and then couldn't handle it when Christmas came and went. Stockdale himself maintained two simultaneous beliefs: he would never lose faith in his eventual release, and he would confront the brutal facts of his situation every single day. Collins translates this into a corporate imperative: create a culture where truth can be heard, but maintain absolute confidence in the outcome.

"You must never confuse faith that you will prevail in the end — which you can never afford to lose — with the discipline to confront the most brutal facts of your current reality, whatever they might be." 1

Nucor Steel's confrontation with its brutal facts is the clearest case in the book. When it faced a steel industry in structural decline, CEO Ken Iverson did not pretend otherwise. He restructured aggressively, invested in minimills when the conventional wisdom was to defend the legacy blast furnace model, and built the most productive workforce in American steel.

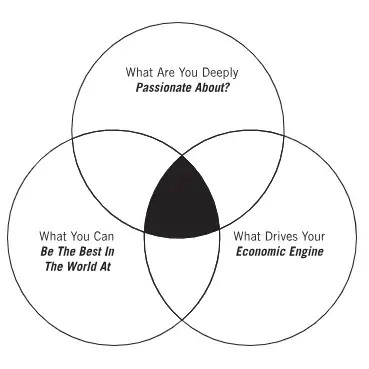

The Hedgehog Concept. Collins draws on Isaiah Berlin's essay dividing thinkers into foxes (who know many things) and hedgehogs (who know one big thing). In business terms, the Hedgehog Concept is the intersection of three circles: what you can be the best in the world at, what drives your economic engine, and what you are deeply passionate about. Collins argues that great companies find this intersection and stay inside it with almost religious commitment.

Walgreens' Hedgehog in the book: "the best, most convenient drugstores, with high profit per customer visit." Every decision was measured against that. When the CEO was offered a chance to acquire a competitor that would have required complexity and distraction, he passed.

"A Hedgehog Concept is not a goal to be the best, a strategy to be the best, an intention to be the best, a plan to be the best. It is an understanding of what you can be the best at." 1

Culture of Discipline. Great companies didn't use bureaucratic rules and hierarchies to force disciplined behavior. They hired disciplined people who then created disciplined thought and took disciplined action. The discipline was self-organizing rather than imposed. Collins distinguishes this sharply from "rigorous" discipline, which he calls ruthlessness — firing people indiscriminately. His concept is about consistent adherence to the Hedgehog Concept and the refusal to diversify beyond it, even when the diversifying opportunities look attractive.

Technology Accelerators. Great-to-great companies were neither technology pioneers nor technology laggards. They used technology as an accelerator of momentum already built, never as a creator of that momentum. When Walgreens rolled out a web presence, it fit perfectly within its Hedgehog. When a comparison company chased e-commerce as a diversification strategy, it created distractions that eventually cost it.

Flywheel vs. Doom Loop. The most frequently quoted framework in the book, and the one Collins later expanded into a standalone monograph. A flywheel is a massive, heavy wheel that requires enormous effort to push at first — but once moving, the momentum compounds. No single push is responsible for its speed; it's the cumulative effect of consistent, aligned effort. The Doom Loop is the opposite: companies that abandon a direction that isn't producing quick results, reorganize, launch new initiatives, reorganize again, never build momentum.

"There is no single defining action, no grand program, no one killer innovation, no solitary lucky break, no miracle moment; rather, the process resembles relentlessly pushing a giant heavy flywheel, turn upon turn, building momentum until a point of breakthrough, and beyond." 5

What actually happened to the 11 companies

Seven years after publication, the research had a natural field test. Here is how the 11 performed.

| Company | Collins's return multiple | Fate after 2001 |

|---|---|---|

| Circuit City | 18.5× | Bankruptcy, November 2008. Final liquidation 2009. 3 |

| Fannie Mae | 7.56× | Federal conservatorship, September 2008. Bailout cost: hundreds of billions of dollars. 6 |

| Gillette | 7.39× | Acquired by Procter & Gamble for $57 billion, 2005. No longer an independent company. 3 |

| Wells Fargo | 3.99× | Fake account scandal, 2016: millions of unauthorized accounts opened without customer consent, billions in fines, CEO John Stumpf resigned. 3 |

| Pitney Bowes | 7.16× | Down roughly 80% from peak share price. 3 |

| Nucor | 5.16× | Still outperforming; one of the few that held up. 3 |

| Abbott Labs | 3.98× | Solid long-term performance; held up. 3 |

| Kroger | 4.17× | Solid long-term performance; held up. 3 |

| Kimberly-Clark | 3.42× | Solid long-term performance; held up. 3 |

| Philip Morris / Altria | 7.06× | Strong total return; tobacco litigation remains an ongoing variable. 3 |

| Walgreens | 7.34× | Ongoing difficulty; facing structural pressure in retail pharmacy. 3 |

Economist Steven Levitt, co-author of Freakonomics, assessed the portfolio in 2008: an investor who bought all 11 companies at publication and held them would have underperformed the S&P 500 from that point forward. 7 Of the 11, only Nucor consistently delivered on Collins's own benchmark.

Collins's explanation for Circuit City's collapse: the company's leaders "abandoned the very practices that made them great." That move — attributing failures to deviation from the framework while attributing successes to adherence to it — is precisely what makes the theory unfalsifiable.

The critique, unflinchingly

The survivorship problem. Collins began by identifying 11 companies that had already achieved spectacular stock returns, looked backward at what they shared, and concluded those shared traits caused the returns. This is the exact error statistician Abraham Wald identified during World War II when analyzing which parts of returning aircraft to reinforce. Wald's insight: you're only seeing the planes that came back. The ones that were hit where your data shows no damage never returned to be counted.

Shah Mohammed, writing on LinkedIn, put the analogy cleanly: "Collins began by identifying 11 companies that had already achieved spectacular stock returns. Then he looked at what they had in common... He never asked the question that Wald would have asked immediately: Did companies that failed look exactly the same?" 6 If 200 companies had humble leaders, disciplined cultures, and focused Hedgehogs, and 150 of them still underperformed the market, the framework is statistically worthless. Collins never established that base rate.

The Halo Effect. Phil Rosenzweig (professor at IMD Business School in Switzerland, former Harvard Business School faculty member) published The Halo Effect in 2007, systematically dismantling Good to Great and similar books. His core finding: Collins's research team relied heavily on magazine articles and analyst reports about the companies — sources that are themselves distorted by how successful those companies already were. When a company is doing well, its culture gets described as strong and cohesive; when it's doing badly, the same culture gets described as insular and rigid. The observations don't explain performance; they're explained by it.

Rosenzweig summarized: "These sorts of data are seen through the lens of the company's success. They don't explain the company's success, they are explained by it." 9 His broader framework identified nine "business delusions" that books like Collins's routinely commit, including the post-hoc attribution of success to observable traits without testing whether those same traits existed in failed companies.

The academic verdict. In November 2008, the Academy of Management Perspectives — a top peer-reviewed management journal — published two independent papers specifically critiquing Good to Great. Bruce Resnick and Timothy Smunt (Wake Forest University) found that if Collins moved his 15-year observation window by just a few months in either direction, "the superior stock market performance that supposedly distinguishes the great companies from the comparison companies almost disappears." Under modern portfolio theory, which adjusts returns for risk, none of the 11 companies outperformed. Their conclusion was direct: "We found that only one of the 11 companies continues to exhibit superior stock market performance according to Collins' measure, and that none do so when measured according to a metric based on modern portfolio theory." 8

Bruce Niendorf and Kristine Beck found that the long-term stock returns of the 11 GTG companies showed no statistically significant difference from S&P 500 averages. Their summary: "Good to Great provides no evidence that applying the five principles to other firms or time periods will lead to anything other than average results." 8 Baylor professor Peter Klein called the two papers together "devastating" in a way that Rosenzweig's earlier critique only threatened to be. 8

Collins's own retreat. In How the Mighty Fall (2009), Collins included a research note that received less attention than it deserved. He wrote: "Correlations, Not Causes: The variables we identify in our research are correlated with the performance patterns we study, but we cannot claim a definitive causal relationship." 2 This is a substantial retreat from a book whose jacket copy promised "the immutable laws of organized human performance." Stanford professor Bob Sutton responded: "I think that Collins needs to say — 'this is just one study, we learned a lot from it, but it isn't definitive… and it has flaws.'" 2

The horoscope problem. Management consultant Graeme Codrington put the framework critique with a directness that practitioners rarely voice publicly: "The good-to-great principles are true in the same way a horoscope is true." 10 The principles are real enough and open enough to interpretation that almost any successful company can be read as having followed them, and almost any failed company can be read as having deviated. Codrington also noted that Collins, when asked whether Jack Welch — one of the most celebrated CEOs of the book's era — qualified as a Level 5 leader, gave an answer that exposed the concept's operational limits: "Well, only Jack really knows whether he was or not." 10 A framework that can't be applied to the most studied CEO in American business history is a framework with a context problem.

Stefan Stern, writing in The Conversation in 2024, identified the structural gap precisely: "The startling black hole at the centre of the book is context." 11 The same leader who would look like a Level 5 hero in a stable industry during an economic expansion might look like a complacent sleepwalker during a technological disruption.

The Deloitte research team that reviewed 13 major success books in 2009 offered the most useful reframe: "Their value is not what you read in them, but what you read into them." 2 The same team made the fable analogy explicit: no one reads The Tortoise and the Hare and then bets on the tortoise at actual races. People extract the idea that perseverance has merit. Collins's frameworks should be read the same way.

What practitioners actually did with it

The most honest field report on Good to Great may come from Joelle Nole (managing partner at Larj Media, former Gates Foundation employee), who wrote in a 2022 essay that she had read the book in the early 2000s, remembered none of the specific frameworks years later, and then — after hearing Collins on a podcast — realized she had been applying "First Who Then What" and the Hedgehog Concept for years. She had just assumed those were her own ideas. "Somewhere along the way, without realizing it, I internalized what I learned from Good to Great and baked it into my own leadership truths so deeply that I thought they were my own!" 12 Her specific application: "Hiring has become a superpower of mine and I owe much of that to Jim Collins." 12

Brené Brown (author of Dare to Lead, University of Houston researcher) has described using the Hedgehog Concept as a decision filter for every major organizational choice. When her team was evaluating whether to launch a podcast, the test was literal: "Is the podcast a hedgehog for us? Are we super passionate about it? Can we do it better than anyone?... And does it drive an economic engine?" 5 The framework became the filter for what her organization said yes to.

Rand Fishkin (co-founder of Moz, the SEO software company) attempted a systematic application of all six GTG concepts to his seven-person startup in 2007 and published his self-assessment. His verdict was honest: a C/C+. On Level 5 Leadership he wrote: "I know that I, myself, am almost an anti-hero here, embodying qualities that are at complete odds with Level 5 leadership." 13 He speculated that SEOmoz might need a different CEO at some point and that he would "be relegated to the role of evangelist." His broader take: "To me, the compelling part isn't the advice, but the research itself." 13

In a 2025 Hacker News discussion on business books, Good to Great drew a split verdict that captures the practitioner landscape well. One user ranked it as one of five core "must-reads" for small business owners. Another called it "classic survivorship bias in book form" and suggested it be renamed "Built to Fail." A third placed it in the "interesting as a history book but not as an actual analysis" category. 14 All three positions are defensible because they are describing different reads of the same book.

"A theory that cannot be proven wrong isn't a theory. It's a belief system." 6

The practitioner consensus that has settled over 25 years: use the Hedgehog Concept and the Flywheel as diagnostic tools and decision filters. Treat Level 5 Leadership as an aspiration with limited real-world measurement. Be skeptical of First Who Then What when it becomes an excuse to delay strategic clarity. Don't cite the book as evidence that your organizational practices will produce great returns. Use it as fuel for introspection, not as a prediction.

Five Monday moves

Each is tied to one of Collins's major frameworks, translated into what practitioners have actually found useful rather than the most idealized reading.

1. Run a Hedgehog audit on your team's work. Before your next planning cycle, ask three questions: what can this team be genuinely best at (not aspirationally, but realistically, given our specific capabilities)? What drives our unit's economic or organizational output? What do the people on the team actually care about?

Work only emerges from the intersection. Anything you're currently doing that sits outside all three circles is a distraction worth questioning. Sean Overin (AMP Healthcare Education) frames this well: focus "is the antidote to drift. It helps you say 'no' to good opportunities so you can say 'yes' to the right ones." 4

2. Name one brutal fact your team is avoiding. Every team has a number, a trend, or a situation that is being collectively looked past. The customer retention rate that keeps softening. The performance gap on one product line. The process that everyone knows doesn't work but no one wants to be the person who names. Write it down explicitly before your next team meeting. You don't have to solve it Monday — but bringing it into the open is the prerequisite for the Stockdale Paradox to function: you can't maintain faith in eventual success while simultaneously avoiding the facts unless you've first confronted them.

3. Audit your last three hires against First Who principles — then stop using it as a delay tactic. Collins's insight that who comes before what is most useful at the diagnostic end: look at your current team and ask honestly whether the right people are in the right seats. Are there people whose best work isn't being unlocked because the role doesn't fit? Are there people in roles that require capabilities they don't have? On the other side, heed Shah Mohammed's warning: "Collins' bus metaphor has become the default excuse for leaders who have no idea where they're going." 6 First Who is a diagnostic, not a substitute for strategic clarity.

4. Map one flywheel turn in your current role. Collins's Flywheel insight is at its most useful when applied narrowly: pick one compounding dynamic in your team's work — a feedback loop where good output makes future output easier. Document it as literally as possible: we do X, which produces Y, which makes Z cheaper/faster/more visible, which creates more capacity to do X. If you can't draw the loop, it may not exist, which is diagnostic in itself. If you can, the question becomes: what is actually slowing the wheel right now, and is it a resource constraint, a process constraint, or a people constraint?

5. Apply Level 5's ego audit — without expecting to become Darwin Smith. Collins's finding that Level 5 leaders directed ambition toward the institution rather than themselves is most practically useful as a periodic self-check rather than a personality description. At the end of a difficult week, ask: in the decisions I made this week, was I solving for the team's long-term capability, or was I solving for how I'd be perceived? Where did I take credit that belonged to someone else, or deflect responsibility that was mine? The answers won't make you a Level 5 leader — but they'll surface the behavioral patterns that Level 5 is trying to describe.

Should you read it?

Good to Great is the most influential management book of the 2000s for a reason. The Hedgehog Concept is a genuinely useful tool for clarifying strategic focus. The Flywheel reframes how you think about momentum. The Stockdale Paradox names a real psychological trap that affects teams under sustained pressure. And Collins is an unusually good writer for a researcher — the case studies are vivid, the examples are memorable, and the book has a clarity of argument that most management texts lack.

The honest scope condition: this is a book about large, stable, capital-rich American public companies that operated in relatively mature industries between roughly 1965 and 1995. It has nothing to say about startups, about non-US markets, about companies navigating technological discontinuities, or about the 25 years since publication. When two of your 11 "great" companies are bankrupt or under federal conservatorship and three more have had serious governance or performance failures, the claim to have identified immutable laws doesn't hold.

Read it for the frameworks. Extract the diagnostic tools. Apply the Hedgehog concept to your team's actual situation. Build the flywheel you can actually describe. Confront the facts your team is avoiding. But if anyone in a planning meeting cites Collins's 11 companies as evidence that a particular leadership approach causes outperformance, ask them what happened to Circuit City.

Good to Great (HarperCollins, 2001) is available in hardcover, paperback, audio, and ebook. 320 pages.

Cover image: Good to Great by Jim Collins, photographed at Larj Media. 12

参考来源

- 1Good to Great — Wikipedia

- 2The Might and Myth of Good to Great — Todd Sattersten

- 3Good to Great Companies: fate of the 11 — Shortform

- 4AMP Healthcare Education: Hedgehog Concept and The Flywheel

- 5Brené Brown: Brené with Jim Collins on Curiosity, Generosity, and the Hedgehog

- 6Survivorship Bias Is the Most Expensive Mistake — Shah Mohammed M, LinkedIn

- 7Good to Great to Pretty Bad — Mike Crittenden

- 8Good to Great: Neither Good nor Great — Organizations and Markets

- 9The Halo Effect (book) — Wikipedia

- 10Good to Great to Gone! — TomorrowToday Global

- 11Books that shook the business world: Good to Great — The Conversation

- 12I Owe Jim Collins an Apology — Larj Media

- 13An Open Challenge: Applying Jim Collins' Good to Great — Moz

- 14Business books are entertainment, not strategic tools — Hacker News

- 15Good to Great summary — Probinism

围绕这条内容继续补充观点或上下文。