hbsp.harvard.edu

Sprint: Turnaround in the U.S. Telecom Industry (HBS W16323)

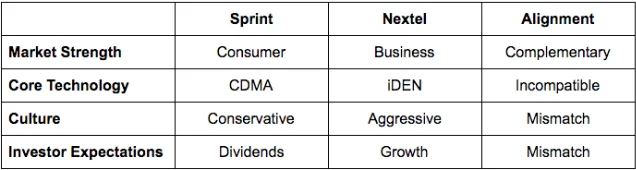

Harvard Business School case study examining Sprint's post-merger turnaround under Marcelo Claure, opening with the observation that Sprint had 'been losing customers and suffering financially since its merger with Nextel in 2005.' A useful sequel analysis to the merger failure examined here.

围绕这条内容继续补充观点或上下文。