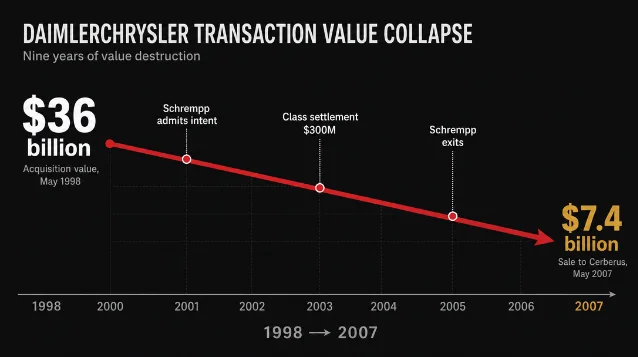

"This isn't an acquisition": how DaimlerChrysler's merger of equals became a $36 billion admission

In April 1998, Jürgen Schrempp suppressed Chrysler's acquisition premium from 40% to 28% using a single categorical argument: "this isn't an acquisition, it's a merger." Internal Daimler notes from February already read "de facto: We take over [Chrysler]." The tactic saved Daimler billions in deal cost — until October 2000, when Schrempp told the Financial Times exactly what he had done, triggering $8 billion in securities fraud claims, a $300 million class settlement, and nine years of litigation. This case traces the full arc from the London premium negotiation through the Third Circuit's 2007 affirmance and the eventual sale of Chrysler to Cerberus for $7.4 billion.

May 27, 2026 · 10:07 PM

1 subscriptions · 10 items

On November 4, 2000, Jürgen Schrempp sat for an interview with Barron's magazine and said, plainly, what had been true all along: "We said in spirit it was a merger of equals, but in our minds we knew how we wanted to structure the company, and today I have it. I have Daimler, and I have divisions." 1

Twenty-three days later, Kirk Kerkorian's holding company Tracinda filed suit in Delaware federal court, alleging $8 billion in securities fraud. It was the opening shot of a seven-year legal war that would involve four federal courts, a $300 million class settlement, and a 123-page trial opinion. Schrempp had closed a $36 billion deal using one of the most effective — and legally dangerous — framing tactics in M&A history. Then he explained it to the press.

The deal that shouldn't have been possible

In May 1998, Daimler-Benz AG and Chrysler Corporation announced what was described as the largest industrial merger in history to that point: an all-stock transaction valuing Chrysler at approximately $36 billion, creating a combined entity called DaimlerChrysler AG 2. Chrysler was the third-largest U.S. automaker; Daimler-Benz was the maker of Mercedes-Benz. The combination was framed, consistently and publicly, as a "merger of equals" — two companies joining as partners to compete globally.

The framing was improbable from the start. Three years earlier, in 1995, Lee Iacocca — the former Chrysler CEO who had saved the company in the 1980s — had joined forces with Kirk Kerkorian, Chrysler's largest single shareholder, in a hostile takeover attempt that rattled Chrysler's management. Chrysler survived, but the experience left its board acutely aware of the company's vulnerability. When Schrempp eventually approached Chrysler's chairman Robert Eaton in early 1998, he arrived with a company that had studied Chrysler's acquisition potential for years through internal projects codenamed "Project Blitz" (1995, Goldman Sachs) and "Project Dutch Boy" (1997, TransAtlantic Consulting) 3.

Bill Vlasic and Bradley Stertz, two Detroit News reporters who conducted more than 200 interviews for their subsequent book Taken for a Ride, described the combination as "a marriage of opposites" — German formality and hierarchy confronting Chrysler's informal cross-functional teams that "favored open collars and free-form discussions." 2 The cultural gap was visible before the ink dried. One Chrysler lawyer called the process "German merger hell." 2

Parties and leverage

| Jürgen Schrempp / Daimler-Benz | Robert Eaton / Chrysler | Kirk Kerkorian / Tracinda | |

|---|---|---|---|

| Stated objective | Global automotive leadership; American distribution and platform reach | Protect Chrysler from hostile takeover; secure Chrysler's independence under a strategic partner | Maximize shareholder value; protect investment |

| Hidden objective | Acquire Chrysler outright; install Daimler management control; preserve Mercedes premium brand purity | Avoid a repeat of the 1995 Kerkorian attack; secure a rich premium for shareholders | Ensure governance commitments, not just price |

| BATNA | Continue as a mid-tier European luxury maker without scale in the U.S. Americas market; the "Project Dutch Boy" acquisition scenario | Continued exposure to hostile acquirers; Kerkorian still held a major stake and had allied with Iacocca once already | Sell his stake to a different acquirer or force a different transaction at a higher premium |

| Key leverage | Premium brand equity; no debt; European regulatory goodwill; "merger of equals" framing suppresses control premium | Profitable truck and SUV platform; lean product development teams; no defensive deal available | Largest individual Chrysler shareholder; board-level access via Aljian on the Chrysler board |

The asymmetry that mattered most was BATNA. Chrysler's board had reason to fear a hostile approach from any direction, and Eaton personally carried the memory of the 1995 scare. Schrempp understood this. The February 1998 notes of Rüdiger Grube, a senior Daimler executive, capture the internal view with unusual precision: "de facto: We take over [Chrysler] (de facto no merger)." 3 These notes were written in the same month Schrempp was publicly promising Eaton a "merger of equals."

"This isn't an acquisition"

The most consequential room in this deal was a meeting in London on April 9, 1998. Schrempp and Eaton had been negotiating for two months. The deal's strategic logic was settled; the one remaining open question was the premium Chrysler's shareholders would receive.

Eaton opened at 40%. Schrempp offered 20%. After roughly two hours of debate, Schrempp made the move that defined the entire transaction.

"Look, if I was acquiring you, I could understand giving that kind of premium. But this isn't an acquisition. It is a merger. Therefore, we shouldn't be looking at anywhere near that kind of a premium." 1

Eaton pushed back: "It's all based on the amount of earnings we're bringing in. We'll be bringing in half the profits. We deserve that kind of a premium." 1

Schrempp prevailed. The parties agreed to $57.50 per share — a 28% premium over Chrysler's pre-announcement stock price.

The 12-point gap between the 40% Eaton demanded and the 28% he accepted had a specific economic value. Class action plaintiffs later argued, in filings before Judge Joseph Farnan of the U.S. District Court for the District of Delaware, that had Eaton known Daimler-Benz did not intend a merger of equals, he would have either canceled the deal entirely or insisted on a full change-in-control premium — which, for a transaction of Chrysler's size, would have been materially higher than what was paid 1. Schrempp's framing tactic, in other words, was not cosmetic — it may have saved Daimler-Benz several billion dollars in acquisition cost by removing the premium category that justifies the largest payouts in M&A.

Judge Farnan, in his 2002 opinion denying Daimler's motion to dismiss, accepted this logic as a cognizable legal theory. The court found that "merger of equals" representations, if made with no intention to honor them, constituted potentially actionable securities fraud — citing In re BankAmerica Corp. Securities Litigation and the Supreme Court's The Wharf (Holdings) Ltd. decision for the proposition that a promise of future conduct can be fraudulent if the promisor never intended to perform 1.

The proxy and the written record

The "merger of equals" framing moved from oral negotiation into the official proxy and prospectus that Chrysler shareholders received before voting. The document described a governance structure where management decision-making would be shared between American and German executives — co-CEOs, a supervisory board with balanced representation, Chrysler's Auburn Hills headquarters maintained as a center of operations.

What the proxy also disclosed, in language that would become legally significant, was that the governance structure could change after closing. U.S. and Delaware courts ultimately found this disclosure critical: the proxy had not actually promised that the co-CEO structure or the geographic balance would persist. The proxy also did not define "merger of equals" with legal precision — a term that, the Third Circuit confirmed in 2007, "had no fixed legal meaning" in the context of securities regulation 4.

The EU Commission approved the merger in July 1998 without conditions (Case M.1204). The FTC cleared the transaction under HSR review in the same period. Chrysler shareholders voted for the deal. The companies merged in May 1998 under a German Aktiengesellschaft holding structure, with Schrempp as chairman of the management board.

"I am a chess player"

By late 2000, the "merger of equals" had quietly dissolved. Chrysler's co-CEO James Holden had been forced out in November 2000. Most of Chrysler's top American executives had departed or been sidelined. Chrysler operated, as Schrempp had always intended, as a Daimler division.

On October 30, 2000, Schrempp gave the London Financial Times a wide-ranging interview ahead of a two-day management board meeting. Asked about the post-merger structure, he explained:

"Me being a chess player, I don't normally talk about the second or third move. The structure we have now with Chrysler (as a standalone division) was always the structure I wanted. We had to go a roundabout way but it had to be done for psychological reasons. If I had gone and said Chrysler would be a division, everybody on their side would have said: 'There is no way we'll do a deal.' But it's precisely what I wanted to do." 1

Five days later, in Barron's, he restated the point: "We said in spirit it was a merger of equals, but in our minds we knew how we wanted to structure the company, and today I have it." 1

Schrempp never denied making these statements, never issued a correction, and never demanded a retraction. The Third Circuit later noted this silence as a factor weighing against any claim that the press had misquoted him 4.

On November 27, 2000, Tracinda filed suit in Delaware federal court, alleging violations of Sections 10(b), 14(a), and 20(a) of the Securities Exchange Act of 1934, plus common law fraud and civil conspiracy. The complaint sought $8 billion in damages 1. By March 2001, 23 putative class actions had been consolidated alongside Tracinda's complaint and a parallel suit by investor James Glickenhaus.

Three courts, nine years, one verdict

The litigation moved through three distinct phases, each with a different outcome.

Phase 1 — Motion to dismiss (March 2002). Judge Farnan denied Daimler's motion to dismiss Tracinda's complaint in substantial part, finding that the FT and Barron's admissions, accepted as true, were sufficient to allege that defendants had misrepresented the deal's nature from the beginning 1. In the summary judgment phase in November 2003, the Grube notes, combined with the Project Blitz and Project Dutch Boy evidence, created a genuine factual dispute about whether the "merger of equals" framing was a knowing misrepresentation — precluding dismissal without trial 3.

Phase 2 — Class settlement (August 2003) and trial (2004–2005). In August 2003, the consolidated class plaintiffs — shareholders who alleged they had been misled by the proxy representations — settled for approximately $300 million 5. Tracinda opted out and pressed its claims through a 13-day bench trial held in December 2003 and February 2004.

In a 123-page opinion issued on April 7, 2005, Judge Farnan dismissed all remaining claims. The core findings were surgical 5:

- Eaton's oral statements were not attributable to Daimler-Benz. Eaton had told Kerkorian that the deal would be a genuine merger of equals — but the evidence showed Eaton had not reported those conversations to Schrempp, and his statements were not made at Schrempp's direction. The misrepresentation, if there was one, was Eaton's, not Daimler's.

- Tracinda did not rely on governance representations. Its internal documents showed Kerkorian cared about the economics: the price, the tax treatment, the financial structure. He had supported the merger before any governance discussions occurred, and when management changes happened post-close, Aljian — Tracinda's representative on the Chrysler board — either supported them or Kerkorian ignored them.

- Reliance was unreasonable for a sophisticated investor. Tracinda had board-level access via Aljian throughout the post-merger governance changes. The Stockholder Agreement contained an integration clause. The proxy had disclosed that governance could change.

The court found Schrempp's post-merger admissions were "plainly damaging in PR terms" — but that was not the same as proving actionable fraud against Tracinda specifically 5.

Phase 3 — Third Circuit (September 18, 2007). The U.S. Court of Appeals for the Third Circuit affirmed the district court in full on all issues Tracinda raised on appeal 4. Tracinda had appealed only the Section 14(a) written misrepresentation claim. The Third Circuit upheld the jury waiver in the Stockholder Agreement as valid and binding, including on non-signatory individual defendants Schrempp and Gentz under traditional agency principles. The $8 billion Tracinda claim was finished.

The net legal result: Daimler won in court, but paid $300 million to settle the class claims. Schrempp's admissions never crossed the legal threshold for fraud against Tracinda. They did, however, produce years of litigation, substantial legal costs, and destroyed whatever remained of the merger's cooperative premise.

The merger that never integrated

While the courts were working, the business was failing.

The integration problem was structural. Schrempp had never intended a real merger, which meant there was no integration mandate — no shared incentive to make the combined organization work as a unit. Chrysler's lean, cross-functional product development teams, which had produced the Dodge Viper, the original Jeep Grand Cherokee, and the LH platform cars in record time on lean budgets, found themselves operating inside a German bureaucracy that valued hierarchy and formal approval chains. Vlasic and Stertz documented the friction in Taken for a Ride as "German formality and hierarchy" smothering the "informal, entrepreneurial culture" that had made Chrysler competitive 2.

Michael Watkins, writing in Harvard Business Review in May 2007 — days after Daimler announced the sale — gave the cleanest diagnosis: "The two organizations never were integrated into anything that approached a cohesive whole. The potential synergies that were used to justify the deal went unrealized." 7 Watkins added an observation that cuts directly to the governance structure Schrempp had designed: the fact that Daimler could sell Chrysler as a more-or-less intact unit to a private equity firm tells you what you need to know about why the combination failed. Integration and separation had been simultaneously impossible — Chrysler was isolated enough to be sold whole, but subordinated enough to have lost its management culture.

In May 2007, Daimler sold 80.1% of Chrysler to Cerberus Capital Management (a private equity firm) for approximately $7.4 billion 7. Against the $36 billion transaction value in 1998, the implied loss on the equity position — before accounting for any distributions or operating performance during the nine years — was staggering. Schrempp had left the company in 2005, replaced by Dieter Zetsche, who had spent time running the Chrysler unit and had a more practical view of what the combination actually was.

Frameworks you can use

Framing as premium suppression — and its legal residue

The London negotiation on April 9, 1998, illustrates a precise tactic: the party with more bargaining leverage reframes the transaction category to change the implicit premium benchmark. In a pure acquisition, a control premium of 30–40% was standard market practice for a target of Chrysler's profile. In a "merger of equals," no such precedent applies — the parties are ostensibly contributing assets at comparable value, so the premium logic dissolves.

Schrempp used this reframing explicitly in the room: if I was acquiring you, I could understand the premium. But this is a merger. The tactic worked because Eaton accepted the categorical premise before disputing the percentage.

The legal risk this creates is specific and durable. The categorical claim — "this is a merger, not an acquisition" — becomes part of the publicly filed proxy, the voting record, and the factual predicate for every subsequent lawsuit. If the transacting party later demonstrates (or admits, as Schrempp did) that the category was false, the premium argument becomes the damages theory. The gap between what was paid and what would have been paid in an acknowledged acquisition is not abstract — it is calculable, plaintiff counsel will calculate it, and courts will permit that calculation to reach a jury unless threshold elements of reliance and attributable misrepresentation can be defeated.

The tactical lesson: framing the deal category is one of the highest-leverage moves in M&A negotiation. The legal lesson is that this framing, once written into official filings, cannot be unwound by a subsequent interview.

The "admitted intent" problem

Schrempp's FT and Barron's interviews are the clearest example in recorded M&A history of a counterproductive post-deal disclosure. He was confirming something he apparently felt was obvious — Chrysler was now a Daimler division, as it had always been intended to be — and the interviews were likely understood internally as a confident statement of achieved strategy.

The problem is that in securities litigation, what a party intended is ordinarily the hardest element to prove. Plaintiffs must typically rely on circumstantial evidence: internal documents, post-deal behavior, anomalous governance decisions. Schrempp's interviews handed plaintiffs a direct admission, in his own words, that the "merger of equals" framing was adopted "for psychological reasons" as a "roundabout way" to achieve a predetermined end.

The 2002 district court opinion found this sufficient to state a claim. The litigation that followed — across four courts, from 2000 to 2007 — cost Daimler $300 million in class settlement, years of management distraction, and reputational damage that likely contributed to the governance difficulties of the combined entity.

The principle: the completion of a deal does not reset the legal exposure created by how it was framed during negotiation. Post-deal public statements about what you "really meant" will be read by opposing counsel as admissions, not as candor.

Integration mandate requires structural alignment of incentives

The DaimlerChrysler case sits in a category of its own in M&A failure analysis precisely because the integration failure was deliberate by design. Schrempp did not want to integrate Chrysler — he wanted a division. A company structured as a "division" has no seat at the table for its management, no shared bonus pool, no career paths that cross the organizational boundary, and no cultural logic for why German engineers should listen to American product development teams who report to a separate subsidiary.

Watkins' 2007 HBR observation — that the two organizations were never integrated — is better understood as a description of the structure Schrempp chose, not a diagnosis of poor implementation. The question for acquirers who contemplate minority integration (preserving target autonomy while capturing cost synergies) is whether the target's management has any affirmative reason to cooperate. At DaimlerChrysler, the answer was no: the "merger of equals" framing had attracted Chrysler's executives on a promise that was revoked in the first two years, and the executives who understood what had happened voted with their feet.

The academic framing from Schühly, Becker, and Klein (2020) describes DaimlerChrysler as "a total failure and a costly disaster" 8. That language, while accurate in its retrospective judgment, misses the structural point: the failure was designed into the transaction from the day Grube took his notes.

What to remember

- Using the deal category as a negotiating lever — "this is a merger, not an acquisition" — directly affects the premium calculus. Schrempp's explicit argument in London suppressed the premium from a potential 40% to 28%. That tactic was legally cognizable as potential fraud: Judge Farnan found in 2002 that a categorical representation made with no intent to honor it can be actionable. Acquirers who use structural framing to suppress premiums should understand that the framing becomes part of the written record and every subsequent lawsuit.

- Admitted intent after closing is not a candor bonus — it is evidence. Schrempp's FT and Barron's interviews, confirming that the "merger of equals" was a psychological tactic, provided plaintiffs with exactly the subjective intent evidence that courts normally require circumstantial proof to establish. The class action settled for $300 million. Tracinda's $8 billion claim ultimately failed on different grounds — the reliance of a sophisticated investor with board access — not because the admissions were legally irrelevant.

- Courts distinguish between "an admission that framing was tactical" and "a proven misrepresentation to a specific plaintiff." Tracinda lost at trial because Eaton's oral representations to Kerkorian were not attributable to Daimler-Benz, and Tracinda's own documents showed Kerkorian cared about price, not governance. The $300 million class settlement is the better measure of what the framing cost Daimler in legal exposure — Tracinda's loss does not mean the tactic was legally safe.

- A company you acquire while pretending to merge will behave like neither a division nor a partner. The isolation that allowed Daimler to sell Chrysler intact to Cerberus in 2007 is the same isolation that prevented the synergies from being realized over nine years. Integration requires that the acquired entity's management has a stake in making the combination work. At DaimlerChrysler, the management who understood what was happening left. The ones who stayed had no mandate to integrate.

Cover image: AI-generated editorial illustration

References

- 1Tracinda Corp. v. DaimlerChrysler AG, 197 F. Supp. 2d 42 (D. Del. 2002)

- 2Taken for a Ride: How Daimler-Benz Drove Off with Chrysler — Publishers Weekly Review

- 3In re DaimlerChrysler AG Securities Litigation, 294 F. Supp. 2d 616 (D. Del. 2003)

- 4Tracinda Corp. v. DaimlerChrysler AG, 502 F.3d 212 (3d Cir. 2007)

- 5Tracinda Corp. v. DaimlerChrysler AG, 364 F. Supp. 2d 362 (D. Del. 2005)

- 6Taken for a Ride: How Daimler-Benz Drove Off with Chrysler — Google Books Preview

- 7Why DaimlerChrysler Never Got into Gear

- 8Google Scholar: Schühly, Becker & Klein (2020) — DaimlerChrysler citation

Add more perspectives or context around this Drop.