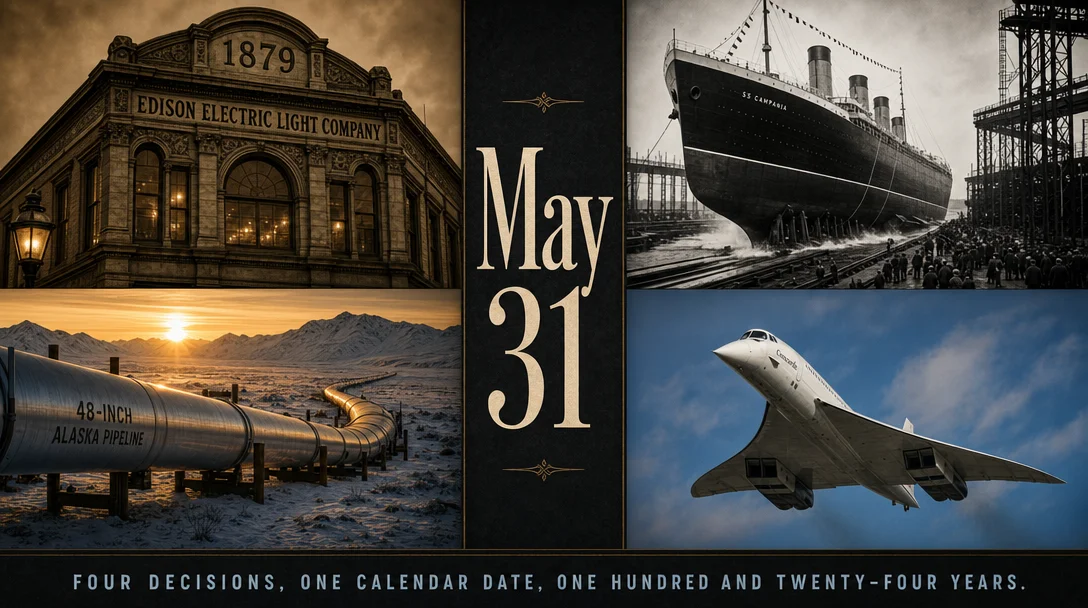

Four decisions, one date: what May 31 teaches about cost, risk, and the names that outlive the buildings

Four May 31 decisions across 124 years — Madison Square Garden's 1879 opening (brand equity as permission structure), the Titanic's 1911 launch (tail risk suppressed for product narrative), the Trans-Alaska Pipeline's 1977 completion ($863M estimate → $8B actual), and Air France's 2003 Concorde retirement (sunk-cost fallacy institutionalized in supersonic flight).

May 31 appears on four very different business certificates of birth and death — 1879, 1911, 1977, 2003 — and each one carries a different species of warning.

1879 — William Kissam Vanderbilt names an arena and accidentally creates a 147-year brand

On May 31, 1879, William Kissam Vanderbilt (grandson of Commodore Cornelius Vanderbilt) held a gala ceremony at the open-air arena on the northeast corner of East 26th Street and Madison Avenue in Manhattan, renamed it "Madison Square Garden," and opened it to New York society. 1 The structure itself was a leaky, roofless box — Harper's Weekly called it a "patched-up, grimy, drafty, combustible old shell." 2 Vanderbilt did not build something great that day. He named something.

The name borrowed the cachet of the adjacent Madison Square Park — itself named after a Founding Father — and it signaled permanence, civic importance, and New York identity before a single event was sold. That brand equity proved durable enough to survive everything that followed:

Vanderbilt found the economics thin and sold to a syndicate that included J.P. Morgan, Andrew Carnegie, and P.T. Barnum, who tore MSG I down in 1889 and erected a Beaux-Arts replacement on the same site. 3 MSG II — designed by Stanford White and topped with an Augustus Saint-Gaudens gilded statue of Diana — was widely hailed as one of the great institutions of New York. 4 It was also never profitable and was razed in 1926 for an insurance company's office tower. MSG III ("The House That Tex Built," by boxing promoter Tex Rickard) opened in 1925 for $4.75 million and was completed in 249 days. 5 It sat 24 blocks from Madison Square. The name stayed anyway. The current MSG IV opened in 1968 above Pennsylvania Station and cost $123 million ($1.14 billion in 2025 dollars). 6 Four buildings, three locations, twelve ownership changes. The brand never changed hands.

As of May 2026, MSG Sports (NYSE: MSGS) carries a market cap of approximately $9 billion, MSG Entertainment (NYSE: MSGE) $3.3 billion, and the Dolan family-controlled Sphere Entertainment spinoff $5 billion — all traceable back to a railroad-depot site that was once described as unworthy of serious attention. 7 Madison Square Garden has been described in the 20th century as "more a state of mind than a building." 2

The mirror: The original property — a vacated railroad depot — was commercially marginal. What Vanderbilt created was a permission structure: a name that told audiences and future investors this was where New York gathered. Before you evaluate whether a brand justifies its premium, ask whether it functions as a permission structure. If removing the name would force customers to re-evaluate the proposition from scratch, the brand has real value. If it's just a label on a commodity, you're renting it, not owning it.

1911 — RMS Titanic slides into the water with 28 lifeboats fewer than the davits could carry

At 12:13 p.m. on May 31, 1911, the RMS Titanic — hull No. 401 at Harland & Wolff's Belfast shipyard — took 62 seconds to enter the River Lagan. 8 More than 100,000 spectators watched, including J. Pierpont Morgan and J. Bruce Ismay. 9 The hull weighed 24,360 tons; the ship still needed ten more months of fitting-out before it could sail. What it did not receive in those ten months was adequate lifeboats.

The decision had already been taken. Harland & Wolff's chief draughtsman Alexander Carlisle had presented plans for 48 lifeboats to Ismay and Harold Sanderson in October 1909 and again in January 1910. Each meeting lasted 5–10 minutes. 10 Titanic's 16 sets of Welin davits were engineered to hold three boats each — 48 total. The ship sailed with 20. Carlisle later testified before the British inquiry: "Personally I consider there were not enough. There were not enough boats." When pressed, he added: "I thought there ought to be three on each set of davits — forty-eight boats." 10 He also acknowledged he never forced the issue with the owners.

The explanation given at the time was that more lifeboats would "look unsightly" on the open promenade deck and obstruct the views first-class passengers paid for. The Board of Trade required only 16 boats for a vessel over 10,000 tons. Titanic carried 20 — technically exceeding the legal requirement — while leaving 58% of its lifeboat capacity unused. 11

The construction cost was £1,500,000 (approximately £190 million in today's terms). 11 The cost of 28 additional lifeboats against that total was negligible. The decision was not about cost. It was about the narrative the product was selling — invincibility and luxury — and how that narrative made the downside look implausible.

The aftermath was swift and structural. By 1913 a permanent International Ice Patrol was established in the North Atlantic. 11 The SOLAS Convention (International Convention for the Safety of Life at Sea), drafted in 1914 and ultimately effective from 1980, now requires adequate lifeboats for everyone aboard — a rule that exists because of one set of 5-to-10-minute meetings in Belfast. 12 White Star Line never recovered its market position; it merged into Cunard in 1934 under government pressure and was absorbed entirely by 1950. 13 Harland & Wolff, the yard that built the ship, entered bankruptcy in 2019 and was acquired by Spanish state-owned Navantia in 2025. 14

The mirror: Two patterns are worth separating here. The first is the "acceptable risk" trap: individually rational decisions (stay legal on lifeboats, maintain speed for schedule, market invincibility) aggregated into catastrophic exposure. The second is captured well in Carlisle's own testimony — the safety professional who presented the risk, saw it dismissed in ten minutes, and did not press further. The institutional pressure to absorb a downside-case argument into the product narrative is not confined to Edwardian shipbuilding. Ask yourself: in the last month, was there a Carlisle in your organization who got ten minutes?

1977 — The Trans-Alaska Pipeline's golden weld: a $900M estimate became $8B

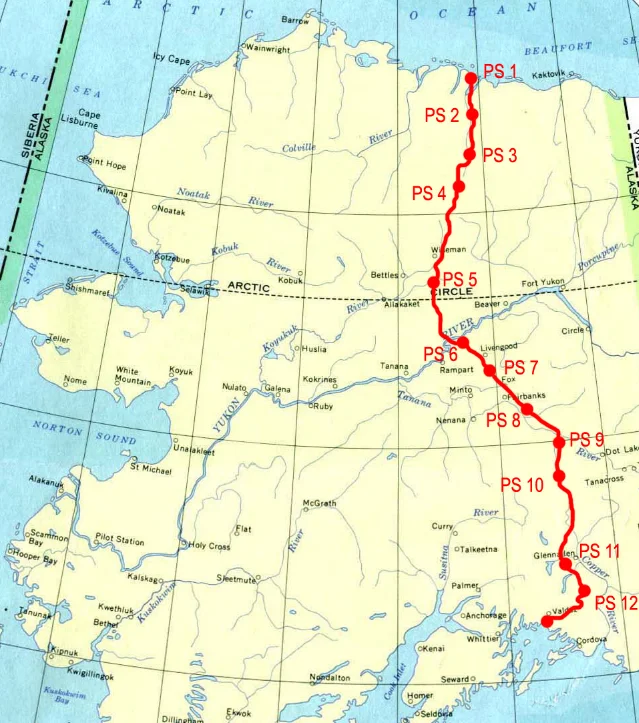

On May 31, 1977, the last segment of the Trans-Alaska Pipeline System (TAPS) was welded at Pump Station 3, near Atigun Pass in the Brooks Range — a ceremony Alyeska Pipeline called the "Golden Weld." 15 The project ran 800 miles from Prudhoe Bay on Alaska's North Slope to the ice-free port of Valdez in the south, crossing three mountain ranges, 34 major rivers, and three active earthquake faults. 15 At its peak in 1975, 28,000 workers were on site simultaneously across 31 construction camps. Thirty-two workers died in the build. 16

The cost story is the point. The 1968 feasibility study estimated the pipeline at $863 million. 15 The final tally for the full system — including the Valdez Marine Terminal and 12 pump stations — came to approximately $8 billion, or about $428 billion in 2025 dollars. 15 That is a 9× overrun on an already complex project, against an estimate developed by people who knew what Arctic engineering entailed.

The legal and regulatory delays compounded the cost severely. After ARCO and Humble Oil discovered Prudhoe Bay — North America's largest oil field, with over 25 billion barrels in place — in March 1968, the pipeline was stalled for five years by environmental litigation under the new National Environmental Policy Act. 16 The decisive vote came on July 17, 1973, when the Senate deadlocked 49–49 on a bill to override NEPA challenges. Vice President Spiro Agnew cast the tie-breaking vote — one of the last significant acts of his tenure before he resigned on tax fraud charges that October. 16 The October 1973 OPEC oil embargo settled the political argument: domestic Arctic oil was now a matter of national security.

The pipeline peaked at 2.1 million barrels per day in 1988 — roughly 25% of total US oil production at the time — and has since declined to approximately 463,000 barrels per day by 2025–2026. 17 The Prudhoe Bay resource has been effectively drained through 47 years of production; two new fields, Willow and Pikka, are under development and are forecast to bring throughput back to around 650,000 barrels per day by 2034.

One genuinely smart downstream decision happened in parallel. In November 1976 — before the first oil even flowed — Alaska voters approved a constitutional amendment establishing the Alaska Permanent Fund, a sovereign wealth fund that receives at least 25% of all mineral revenue. 18 The fund's first deposit was $734,000 in February 1977. It stood at $89.3 billion as of April 2026, provides over 50% of Alaska's unrestricted general fund revenue, and pays an annual dividend to every Alaska resident — typically between $1,000 and $1,600. 18 The recognition behind it was plain: "Alaska's new oil wealth will not last forever." Depositing while the money flowed was the only moment it could be done.

The mirror: Two separate lessons live here. The megaproject cost overrun (9× the estimate, before a single barrel flowed) is partly explained by regulatory complexity, but it also reflects a well-documented pattern in large capital projects: initial estimates are made at the stage of maximum optimism and minimum information, then revised upward as commitments accumulate and reversibility falls. If your organization is using a first-pass estimate to secure project approval, build in a floor assumption for regulatory and environmental delay — even where you think the path is clear. The second lesson is about sovereign wealth discipline: Alaska's decision to capture resource revenue into a permanent fund while the resource lasted now funds most of the state's government even as the resource depletes. The optimal moment to build that buffer was before the dependency was complete.

2003 — Air France retires Concorde: when physics is the business constraint

At 08:15 on the morning of May 31, 2003, Air France flight AF001 — a Concorde, registration F-BTSD, commanded by Captain Jean-François Michel — departed New York's JFK Airport for Paris Charles de Gaulle. 19 Three fire trucks sprayed red, white, and blue arcs of water over the aircraft as it left. Several thousand fans lined the runway at CDG when it touched down at 17:44, 3 hours and 40 minutes later, holding banners that read "Thank you Concorde, we love you." 20 It was the end of 27 years of French supersonic passenger service.

Air France chairman Jean-Cyril Spinetta had announced the decision on April 10, 2003: "Operating Concorde has become a severely and structurally loss-making operation. In these circumstances, it would be unreasonable to continue operating it any longer." 19 British Airways followed on October 24, 2003. The program was over.

The economics had never worked. The original 1962 development estimate was £70 million; the actual cost by 1976 was £1.5–2.1 billion — a 20–30× overrun — borne entirely by British and French taxpayers. 21 Airlines placed over 100 non-binding orders; every non-flag carrier cancelled through the 1970s. Five unsold aircraft were eventually handed to BA and Air France for £1 or one franc each in 1980. 22 Only 14 entered commercial service. The original market forecast had been 350 aircraft. 22

The core physics problem was permanent. Concorde achieved 15.8 passenger-miles per gallon; the Boeing 747 achieved 46.4. Per-seat fuel burn ran approximately 4× that of subsonic aircraft. 22 A US ban on overland supersonic flight (1973) eliminated transcontinental and trans-Pacific routes; the aircraft could only fly supersonic over water, confining it to the North Atlantic. 22 No engineering innovation could solve these constraints inside Concorde's operational lifetime.

British Airways did find a narrow path to operational profit. Research revealed that 80% of passengers did not know what the fare was — it was booked by their corporate travel desk or personal assistant. So BA raised prices to match what passengers assumed they were paying, eventually reaching a round-trip New York–London fare of approximately $12,000 in 2003 dollars. 23 At its peak, BA earned roughly £30 million per year in net operating profit from Concorde. 23 Operational profit, however, never touched the development cost. Total government subsidy over the program's lifetime is estimated at $40 billion in 2025 dollars — for a fleet that carried approximately 2.5 million passengers over 27 years, a subsidy of roughly $16,000 per passenger. 21

The July 2000 crash of Air France Flight 4590 — triggered by a strip of metal debris from a Continental DC-10 that had taken off minutes earlier, which blew a tire and ruptured a fuel tank — killed 113 people and grounded the fleet for 15 months. 24 Safety modifications cost roughly $50 million combined. When Concorde returned to service in November 2001, the post-September 11 aviation downturn had hollowed out premium travel demand. Air France sometimes flew with single-digit passenger counts. The retirement was structurally inevitable once the crash destroyed the one thing the product had unambiguously delivered: a perfect safety record.

The 1962 Anglo-French treaty included penalty clauses making unilateral cancellation effectively illegal — a mechanism that, in retrospect, is the cleanest illustration of the sunk-cost fallacy as institutional design. The commitment device locked both governments in for decades after the commercial case had evaporated.

Twenty-three years after Concorde's retirement, no commercial supersonic passenger service exists. Boom Supersonic's XB-1 demonstrator achieved its first supersonic flight in January 2025 over the Mojave Desert. 25 United Airlines CEO Scott Kirby put his assessment of Boom's full-scale Overture airliner at "50-50" in March 2026, noting the current design's range is too short for the routes where supersonic economics actually work. 26 BA chairman Lord Marshall predicted in 2003 that in the lifetimes of today's adults, "they probably won't see another supersonic commercial aircraft." 23 That forecast has held for 23 years.

The mirror: The Concorde program is the canonical demonstration of two things that are hard to keep separate in practice: the sunk-cost fallacy (continuing because of what you've already spent, not because of what lies ahead), and physics as a non-negotiable constraint. BA's pricing innovation showed that operational economics can sometimes be salvaged; it did not show that an unworkable physics problem can be solved with product repositioning. Before committing to a flagship program, identify the constraints that are structural (fuel burn at Mach 2, sonic booms over land) versus the constraints that are financial or regulatory. The first kind will not yield to better management. The second kind sometimes will.

Cover image: AI-generated composite illustration.

References

- 1Wikipedia: Madison Square Garden (1879)

- 2Ballparks.com: Madison Square Garden I

- 3Untapped New York: The Many Lives of NYC's Madison Square Garden

- 4Wikipedia: Madison Square Garden (1890)

- 5Wikipedia: Madison Square Garden (1925)

- 6Wikipedia: Madison Square Garden

- 7Long Island Press: The History of Madison Square Garden

- 8Titanic Belfast Museum: 31st May 1911 — On This Day

- 9Titanicandco.com: Launch of the Ship of Dreams

- 10Titanic Inquiry Project: Testimony of Alexander Carlisle, Day 20

- 11Wikipedia: RMS Titanic

- 12Wikipedia: SOLAS Convention

- 13Wikipedia: White Star Line

- 14Wikipedia: Harland & Wolff

- 15American Oil & Gas Historical Society: Trans-Alaska Pipeline History

- 16E&E News by POLITICO: How Spiro Agnew helped save the Trans-Alaska project

- 17Alyeska Pipeline: Historic Throughput

- 18Alaska Permanent Fund Corporation: History

- 19ConcordeSST.com: Air France Concorde Retirement

- 20Gulf News: May 31, 2003 — France bids farewell to Concorde

- 21Economics Explored: Concorde's economic lessons

- 22Wikipedia: Concorde

- 23Vanity Fair: The Final Flight of the Concordes

- 24Wikipedia: Air France Flight 4590

- 25Boom Supersonic: Year in Review 2025

- 26Forbes: United Airlines CEO Sets Boom Overture Odds At 50-50

Add more perspectives or context around this Drop.