1/4

Diversification Theater: You Own Three Things. They All Fall Together.

You hold housing, A-shares, and bank deposits — three asset types on paper, one correlated bet underneath. When employment stumbles, all three fall in the same direction. This is Issue 02 of Wage Trap Chronicles: the diversification illusion, with actual numbers.

June 1, 2026 · 8:04 AM

Gallery

You've done what everyone told you to do. You bought a place. You put some money in A-shares. The rest sits in bank deposits earning a modest yield. Three separate buckets, three different asset types. Diversified, right?

Run the actual numbers.

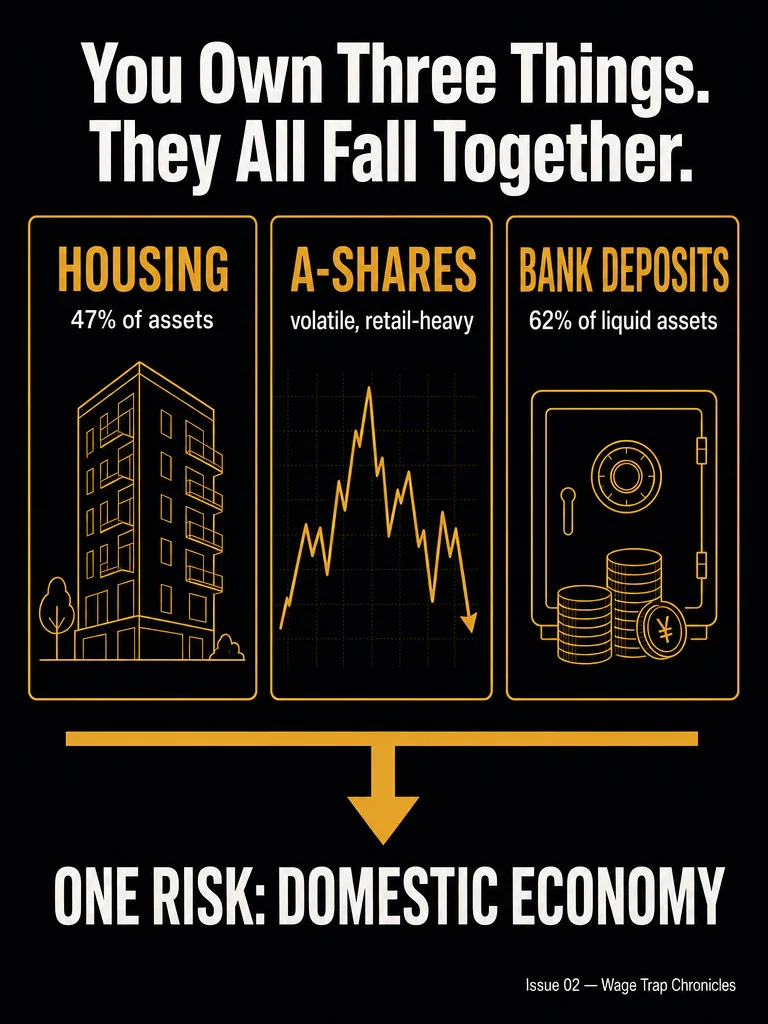

The balance sheet most wage earners actually hold

According to the World Bank's China Economic Update, real estate accounts for 47% of Chinese household assets. Bank deposits and cash make up another large slice — mainland Chinese households held roughly 62% of their liquid financial assets in cash and deposits as of recent data. A-shares make up most of the remainder for those who invest at all.

Three buckets. All labeled differently. All pointing at the same underlying engine.

What "correlated risk" actually means at the household level

Correlation doesn't mean two assets move identically. It means they share a common driver. For the typical wage earner in China, that driver is domestic economic conditions — specifically, employment stability and GDP growth.

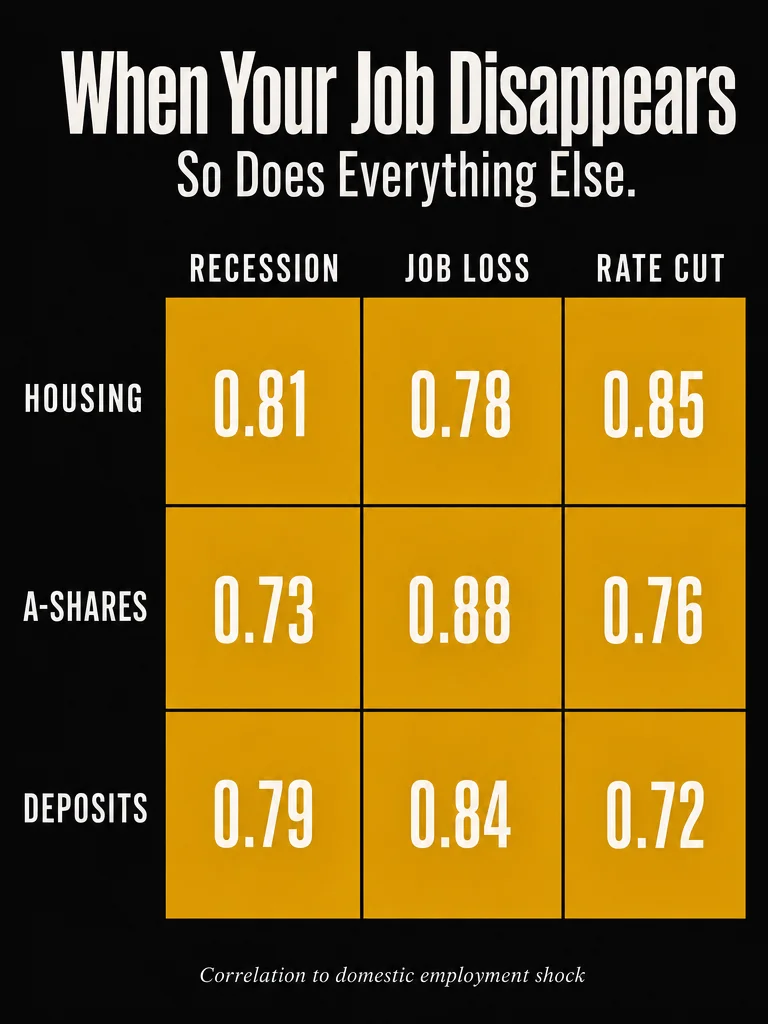

Here's what the correlation looks like when that driver stutters:

Housing: Real estate is not just a long-term savings vehicle. It's a leveraged bet on local economic demand. The China property correction beginning around 2021 cut new home prices in dozens of cities by 20–30%. The World Bank estimates the downturn reduced annual GDP growth by approximately 2 percentage points per annum in 2024 and 2025. Property values and employment conditions move together — same driver.

A-shares: Chinese retail investors are disproportionately exposed to the domestic market, with capital controls limiting international diversification. When economic stress hits, A-shares respond accordingly. Between June 2015 and January 2016, the MSCI China A Index fell roughly 50%. That's not volatility noise — that's systemic correlation with domestic economic sentiment.

Bank deposits: These feel safe, and in nominal terms they are. But when the economy weakens, the central bank cuts rates to stimulate growth. Real deposit yields compress or go negative. The "safe" part of the portfolio silently erodes.

The mechanism that makes this worse: employment is the root variable

The three assets don't just share a general correlation with "the economy." They share a specific correlation with your employment status — the same variable that also determines your mortgage serviceability.

When you lose income:

- Your ability to service the mortgage weakens → forced asset liquidation risk

- A-share holdings may be sold to cover costs → selling into a falling market

- Deposit drawdowns reduce the buffer

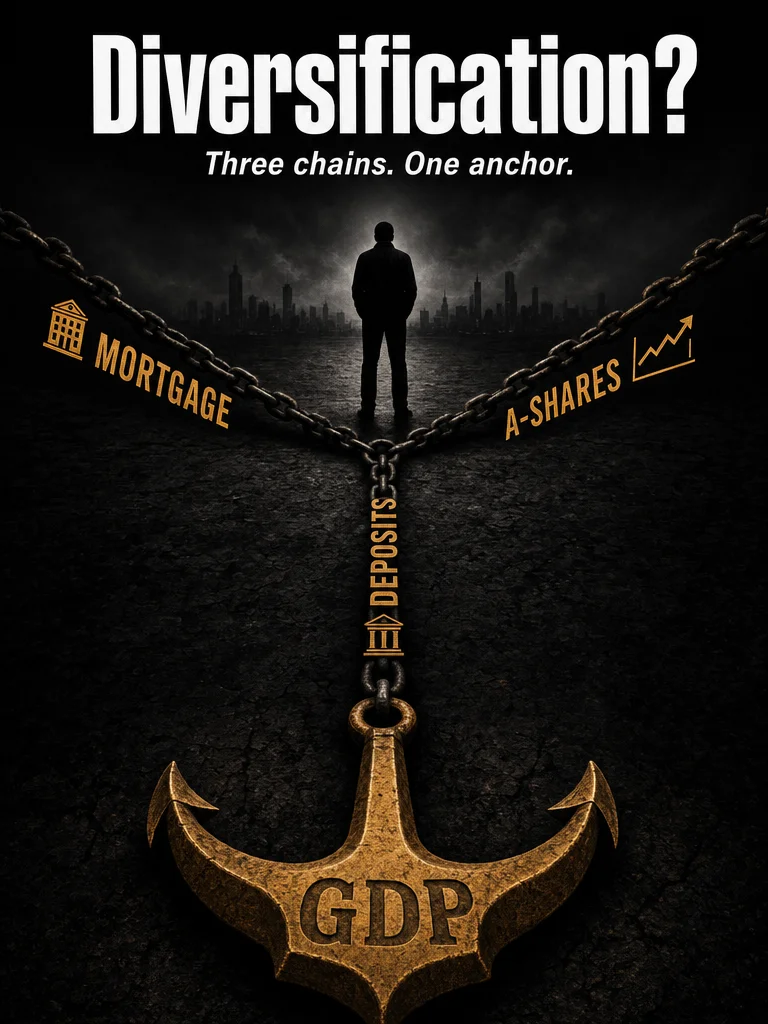

What looked like three independent risk positions is actually one large bet on your job not disappearing, in the same economy that prices your house, drives your stock market, and sets your deposit yield.

Why this is structurally different from actual diversification

Real diversification requires uncorrelated risk drivers — cash flows tied to different economic engines. A domestic property bet, a domestic equity bet, and a domestic bank deposit don't achieve that. They're three instruments playing the same note.

The framing matters: this isn't about whether any individual asset is "good" or "bad." Housing in China has produced real long-term returns. A-shares can. Bank deposits preserve nominal capital. The issue is that holding all three doesn't reduce your exposure to a Chinese economic downturn — it concentrates it three times over, under three different labels.

What next

The standard counter-argument is: "where else would you put it?" That's a fair question — and it's next week's topic. The answer isn't simple, but it starts with understanding that the portfolio you think you have is not the portfolio you actually have.

Sources: World Bank China Economic Update Dec 2022 (household asset breakdown); China Daily, Jan 2026 (household deposit data); Seafarer Funds — China's Household Balance Sheet (balance sheet structure, A-share drawdown data, mortgage LTV context); Incomlend — The Correlation Illusion (correlation spike mechanics); GAM Investments (China housing downturn GDP impact estimate, Jan 2026).

Comments