FIGR — Q1 2026 results

Quarter ended March 31, 2026; stock price $33.95 as of May 22, 2026

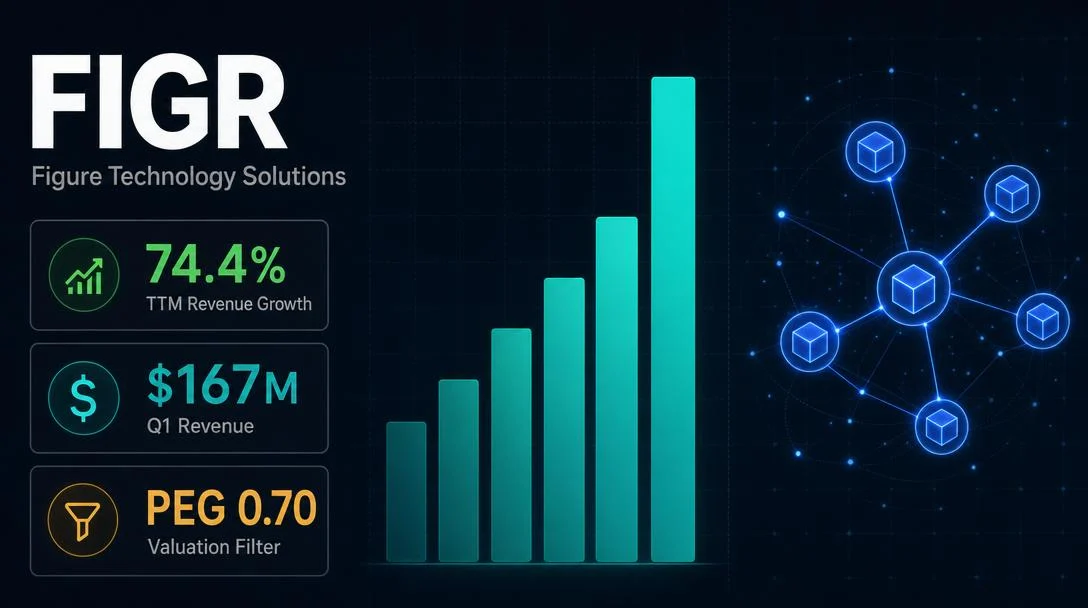

Figure Technology Solutions (NASDAQ: FIGR, $7.51B market cap) passes all four hard screening filters as of May 22–24, 2026: TTM revenue growth +74.38%, PEG 0.70 (single-source, disclosed), TTM OCF +$165.02M, market cap below $10B. The article covers FIGR's blockchain-native consumer lending marketplace (3.8% net take rate, near-100% gross margin, $1,000 vs. $11,500 industry origination cost), Q1 2026 earnings ($167M revenue +97.6% YoY, $45M net income, 49.6% adj. EBITDA margin — Rule of 140), Q2 volume guidance $3.8B–$4.1B, peer valuation vs. UPST/SOFI/LC, net cash balance sheet ($439M), catalysts (387 partners, Flagstar onboarding, first-lien 14%→20%, YLDS $598M, Credibly SMB partnership), and key risks (single-source PEG, SBC at 57.5% of net income, HELOC concentration, three 10b5-1 insider sales, material weaknesses). Analyst consensus: Strong Buy, 9 analysts, $54 average target (59% implied upside) vs. GuruFocus GF Score 23/100 and DCF fair value ~$15.38. Upcoming catalysts: Bernstein May 27, Piper Sandler June 3, FOMC June 16–17, Q2 earnings ~August.

| Hard filter | Threshold | FIGR result | Status |

|---|---|---|---|

| Market cap | < $10B | $7.51B (StockAnalysis); $7.50B (Yahoo Finance); $7.45B (iTick) | ✅ Pass |

| TTM revenue growth | > 30% | +74.38% (StockAnalysis, to $510.35M TTM) | ✅ Pass |

| PEG ratio | < 1.0 | 0.70 (StockAnalysis only — Yahoo Finance does not publish PEG for FIGR) | ✅ Pass ⚠️ |

| TTM operating cash flow | Positive | +$165.02M (StockAnalysis and Yahoo Finance, identical) | ✅ Pass |

| Metric | FIGR | UPST | SOFI | LC |

|---|---|---|---|---|

| Market cap | $7.51B | $2.73B | $20.04B | $1.80B |

| TTM revenue growth | +74.4% | +57.7% | +41.0% | +25.4% |

| Trailing P/E | 58.74x | 69.00x | 35.11x | 10.44x |

| Forward P/E | 33.67x | 11.23x | 23.91x | 8.77x |

| PEG | 0.70 ⚠️ | 0.28 | 0.63 | n/a |

| P/S (TTM) | 14.71x | 2.33x | 5.13x | 1.31x |

| EV/Sales | 13.85x | n/a | 4.70x | n/a |

| TTM OCF | +$165M | -$268M | -$6.08B | -$3.01B |

| Item | Value |

|---|---|

| Cash and equivalents (ex. restricted) | $1.46B |

| Total debt | $1.32B |

| Net cash | +$439M ($1.99/share) |

| Current ratio | 1.90 |

| Debt/Equity | 1.02 |

| TTM operating cash flow | +$165.02M |

| Share buyback authorization | $200M (~2.7% of market cap) |

Analyst price targets carry systematic optimism bias; treat these as directional signals, not forecasts.

Full valuation metrics for FIGR: P/E 58.74x, Forward P/E 33.67x, PEG 0.70, P/S 14.71x, TTM OCF +$165M, net cash $439M, and institutional / insider ownership breakdown.

April 2026: CLM volume $1.34B (+108% YoY, +12% MoM), Democratized Prime matched offers $384M, $YLDS circulation $529M. Lender-supply/borrower-demand ratio improved to 1.2x.

Q1 2026 earnings press release: $167M revenue (+97.6% YoY), $45M net income, record 80 new partners, Q2 CLM volume guidance $3.8B–$4.1B.

Management presentations: Bernstein 42nd Annual Strategic Decisions Conference, New York, May 27 (3:30 PM ET); Piper Sandler Global Exchange & FinTech Conference, New York, June 3 (2:00 PM ET). Livestream at investors.figure.com.

Add more perspectives or context around this Drop.