25/6/2026 · 7:24

Burry on LULU: "Bad management is a value investor's best friend"

Michael Burry published a full-length Substack thesis on Lululemon on June 24, arguing the stock is the only U.S. apparel retailer of scale trading below 3× tangible book and 10× earnings — a valuation he frames as a screen result, not a story bet. He attributes the 75% decline from the 2025 high to management missteps, a failed product launch, and tariff headwinds, and positions incoming CEO Heidi O'Neill's September start as the catalyst that ends the stall.

Just after midnight on June 25, Michael Burry (Scion Asset Management — the hedge fund manager whose 2007–08 subprime short was chronicled in The Big Short) announced a new Substack post with eleven words: 1

Cargando tarjeta de contenido…

The piece, titled "lululemon athletica (LULU): Where is John Galt?" with the subtitle "In Defense of an 800lb Gorilla Overstretching its Leggings," makes the case that Lululemon is a sound business temporarily buried under a pile of own goals — and that the market has mispriced the difference. 2

The valuation screen

Burry's entry point is a filter most screens would never run. He writes that LULU is currently "the one and only U.S. clothing retailer of any market capitalization trading at less than 3× tangible book and less than 10× earnings." 3

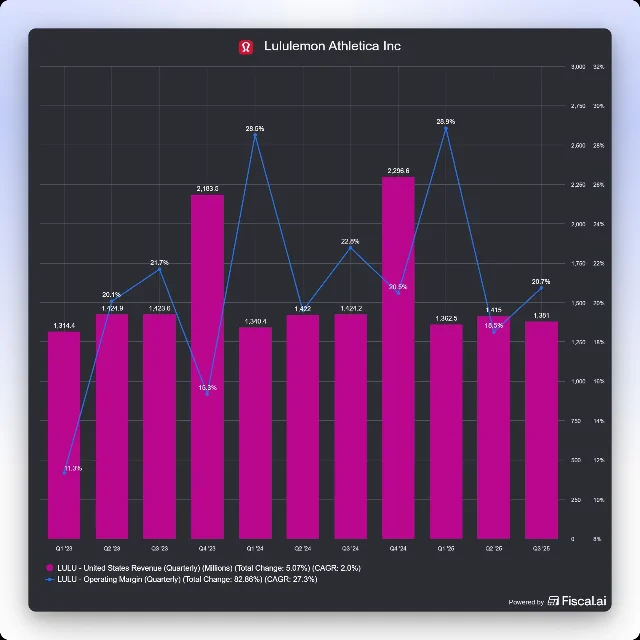

The stock trades near $104 as of the post — down more than 75% from its early-2025 high of $423, sitting at a seven-year low, and off roughly 45% year-to-date. 3 For a company with no debt and positive free cash flow, that combination of price-to-book and price-to-earnings is unusual enough that Burry frames it as a screen result, not a narrative bet.

He also disputes the competitive threat thesis directly: "LULU is not losing too many people who like to sweat to ALO or Vuori, and in fact at least 95% of LULU's customers are not customers of either of the upstarts." 4

A recurring crisis pattern

The article's organizing frame is a historical cycle: Lululemon has broken down before, recovered, and broken down again — with management failure as the recurring cause and brand resilience as the recurring floor.

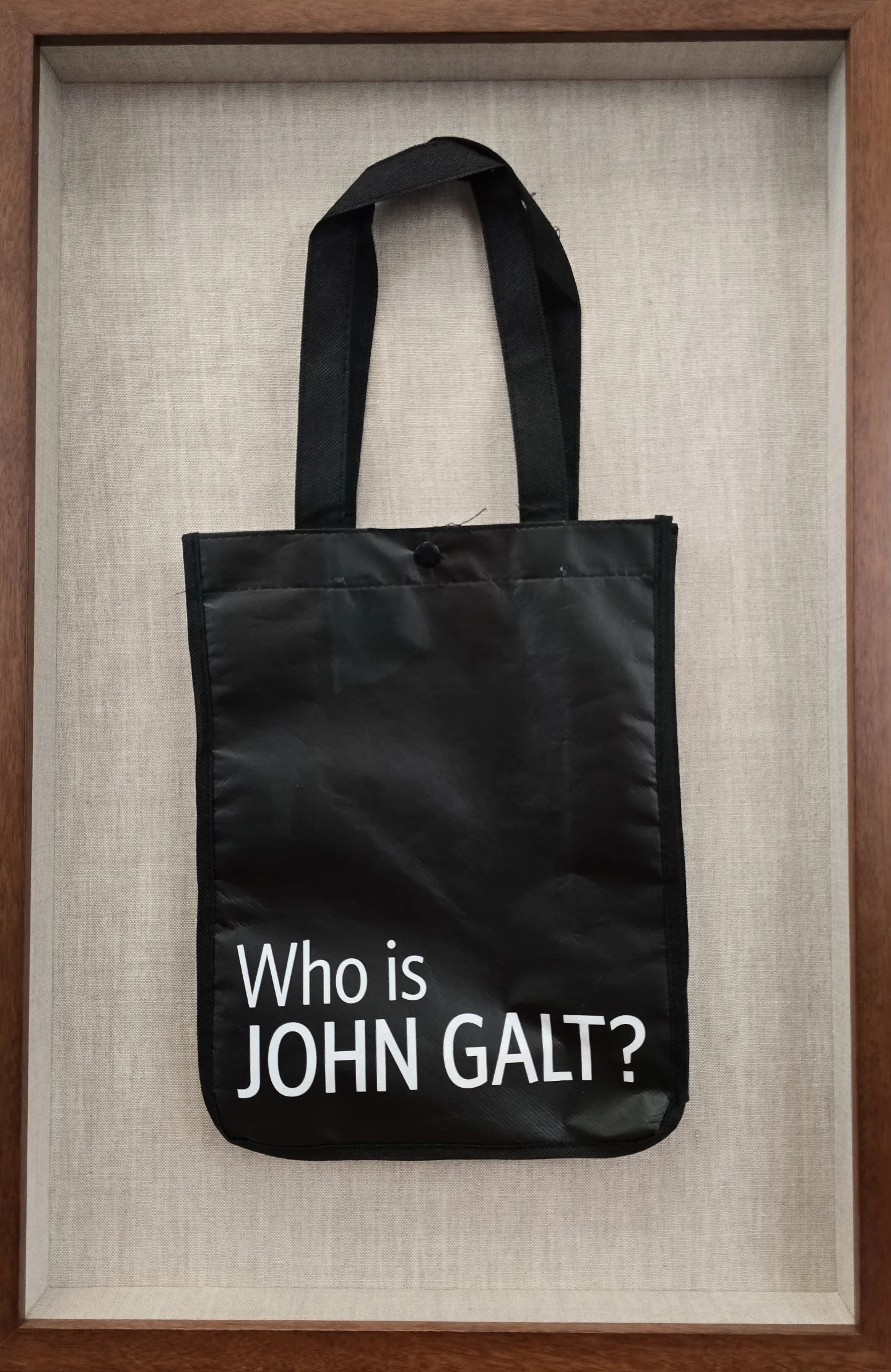

Burry traces the arc: the 2011 controversy when founder Chip Wilson printed "Who is JOHN GALT?" on shopping bags, alienating the brand's core customer of 25-to-45-year-old women practitioners; a first-term Trump tariff hit that shaved roughly 2.5 percentage points from gross margin; a revolving-door CEO period; then a full recovery under Calvin McDonald after 2018, with margins reaching historic highs. 2 3

Now the company is inside another version of the same cycle: the 2024 Breezethrough leggings launch failed and was pulled due to transparency and fit problems; the CEO seat is vacant; and second-term Trump tariffs knocked roughly three percentage points off product gross margin in the most recent quarter, with the removal of the de minimis import exemption adding further cost pressure. 3

Burry's summary of the damage is deliberately undramatic: "The business is not falling apart. It is simply not growing due to multiple mistakes, lack of management, lack of execution, and regulatory hits with tariffs and the extinction of the de minimis exemption." 3

The framed 2011 "Who is JOHN GALT?" shopping bag that Burry keeps in his conference room — a prop his wife retrieved and mounted — gives the post its title and its thesis in shorthand: the brand survived its own founder, and it can survive this. 2

The management quote and the catalyst

The post's most quotable line doubles as Burry's investment philosophy on management-driven drawdowns:

"Bad management is a value investor's best friend. If not for bad management, the world would be more boring, less colorful, and less undervalued. Of course, like all best friends, bad management should not overstay its welcome." 3

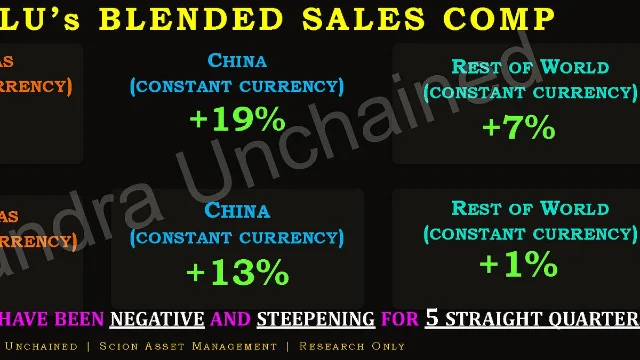

The incoming CEO provides the catalyst half of that equation. Heidi O'Neill — formerly a top executive at Nike — takes the role in September. 3 Meanwhile, Scion's own data shows China as a point of divergence: in the most recent quarter, China constant-currency sales grew 19% while the rest-of-world figure came in at 7%; the prior quarter showed +13% and +1% respectively. 2

What this means for readers

Burry's LULU call sits in a different part of his portfolio logic than his AI shorts. The Palantir and semiconductor puts bet on narrative multiples collapsing. The LULU long bets on a tangible brand with measurable cash generation being priced as though it is broken when, by his read, it is merely stalled.

The full post is behind Burry's Substack paywall (Cassandra Unchained, 290,000+ subscribers). 2 The valuation claim and direct quotes above have been amplified via Stocktwits and Yahoo Finance; the China sales data and deeper product analysis are in the paid section. For readers following Burry's positioning, the signal to watch is whether O'Neill's September start changes analyst sentiment — currently 2 out of 32 covering analysts carry a buy rating, a figure Burry has cited across multiple posts as the floor of bearishness on LULU. 3

Cover image: Lululemon "Who is JOHN GALT?" framed bag from Scion Asset Management's conference room, published in Michael Burry's Substack post on June 24, 2026. Image from Cassandra Unchained.

Fuentes de referencia

Contenido relacionado

LULU — priced for collapse, built like a compounder

US Stock Pick: 3-Year ROE > 15%Artículo

When the tide went out: Buffett's 2007 guide to great, good, and gruesome businesses

Shareholder Letters From Top LeadersArtículo

The $165 billion trap: how AOL bought the world's largest media company with casino chips

Business Negotiation Classics: One Case a DayArtículo

Añade más opiniones o contexto en torno a este contenido.