US cyber insurance: 2024 snapshot

Key market metrics, full-year 2024

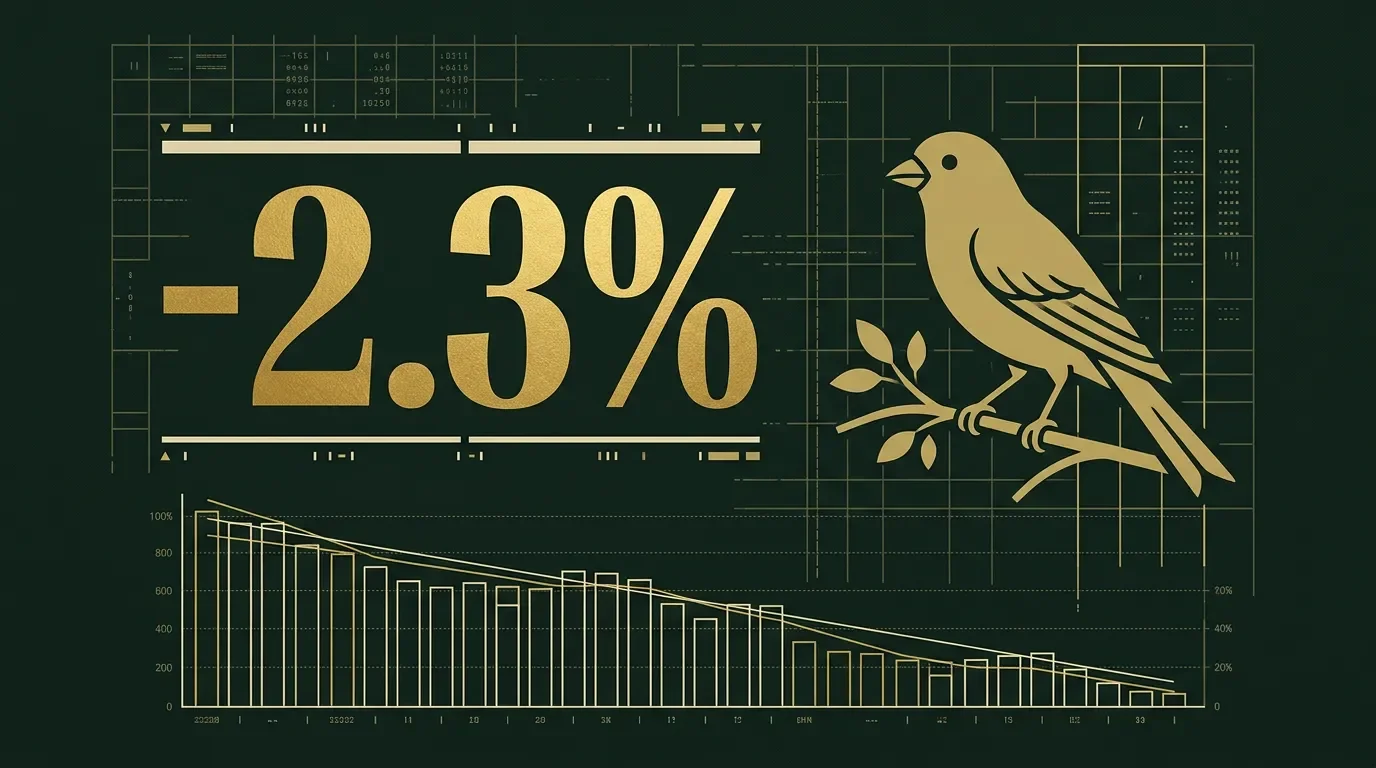

US cyber insurance direct premiums declined 2.3% to $7.08B in 2024, the first drop since NAIC tracking began. The cause is competitive capacity, not lower risk. Loss ratios are creeping toward 50%, the best commercial risks are leaving for captives, and threat severity is rising. This issue reads the move as a forward signal and maps three concrete planning scenarios for policyholders and SMB owners.

围绕这条内容继续补充观点或上下文。