Prime Day eve radar: five cold-start categories with the sharpest evidence this week

Issue #6 surfaces five DTC niche signals for June 15–22: silicone air fryer liners, insulated tote + dispenser, kids' furniture (week 5), GLP-1 supplements (week 5), and levitating home decor. Prime Day opens June 23 — three of the five entries have a direct Prime Day demand tailwind.

内容来源:...

Prime Day opens tomorrow — five niche categories with the strongest cold-start evidence this week, plus four persistent watchlist signals that are moving.

Rating key

| Rating | Demand signal | Competition density | Cold-start readiness |

|---|---|---|---|

| ⭐⭐⭐⭐⭐ | Multi-source, 40%+ listing growth or 5+ week AliDropship recurrence | Zero dominant brand; fragmented or absent | Low MOQ, workable margin, clear acquisition channel |

| ⭐⭐⭐⭐ | Strong single-source with corroborating signals; 3–5 week recurrence | 1–2 known brands, no DTC-native position | Some friction (compliance, certification, brand investment) |

| ⭐⭐⭐ | Moderate signal; 2–3 week recurrence | Growing competition; quality variance high | Entry possible but narrower window |

| ⭐⭐ | Weak or single-source signal | Established brands present | High barrier; requires significant brand investment |

Quick-scan overview

| Category | Demand signal | Competition density | Cold-start rating | Prime Day angle | Status |

|---|---|---|---|---|---|

| Silicone air fryer liners | ⭐⭐⭐⭐⭐ | Low (no DTC brand) | ⭐⭐⭐⭐⭐ | Kitchen appliance halo; repeat-purchase moat | New this week |

| Insulated tote + drink dispenser | ⭐⭐⭐⭐ | Low–medium (mid-tier gap) | ⭐⭐⭐⭐ | Outdoor/hydration Prime Day board; demand peaks June 23–July 4 | New this week |

| Kids' furniture small-SKU | ⭐⭐⭐⭐⭐ | Medium (sub-niches open) | ⭐⭐⭐⭐ | Back-to-school Prime Day deal category confirmed | Recurring (week 5) |

| GLP-1 muscle preservation supplements | ⭐⭐⭐⭐ | Zero DTC brands — white space confirmed | ⭐⭐⭐⭐ | None direct; urgency from week 5 escalation | Recurring (week 5) |

| Levitating / magnetic home decor | ⭐⭐⭐⭐ | Low (TikTok-native, pre-brand) | ⭐⭐⭐⭐ | None direct; TikTok-native organic channel | New this week |

Silicone air fryer liners — the repeat-purchase sleeper

Demand signal: ⭐⭐⭐⭐⭐ · Competition: Low · Cold-start rating: ⭐⭐⭐⭐⭐

Most kitchen gadget plays are a one-purchase ceiling. This one is not.

Silicone air fryer liners experienced a 300% search volume spike in Q4 2025, and that spike did not decay — the category held flat through Q2 2026 as a stable demand plateau rather than a post-viral comedown. 1 That demand persistence is the category's main structural argument. A typical household replaces 4–6 liner sets per year, meaning a first purchase at $14–22 retail converts into $96–120 in annualized customer value on repeat buys alone. 1 2

The Prime Day angle is indirect but real. Amazon's Prime Day 2026 deal board explicitly covers kitchen appliances — Ninja, Black+Decker, Cuisinart, Hamilton Beach are all confirmed deal categories with up to 40% off. 3 When air fryer units move at volume during the next four days, accessory demand follows. A seller already ranked for liner searches on June 26 is positioned to capture that halo traffic rather than scrambling to list into it.

Gross margin runs 55–70% at the $14–22 price point, which is unusually high for a consumable. 1 The optimal channel structure is Amazon Subscribe & Save for the repeat-buy economics, with TikTok Shop for first-purchase discovery. Sourcing requirement: LFGB or FDA food-grade silicone certification, heat resistance to 230°C minimum, pre-shipment burn-off QC to clear any residual odor.

Competition check: No dominant DTC brand has been identified in this category across the June 15–22 scan window. The current supply side is fragmented: generic private-label sellers on Amazon and dropshipping commodity listings, no brand with a defined identity, a subscription model, or a distinct content strategy. That gap is what "cold-start friendly" looks like in practice.

Key risk: The product is commodity-shaped. A brand that prices the liner at $9.99 as a one-time purchase caps its own LTV at $9.99. The structural advantage only materializes if the seller builds explicitly for subscription from day one — the listing copy, the post-purchase email flow, and the Subscribe & Save setup are not optional add-ons to the business model; they are the business model.

Cold-start entry: Launch a 3-pack or 5-pack at $16–22 with an optional Subscribe & Save enrollment. COGS for a 5-pack: approximately $4–7 with LFGB-certified silicone from standard Chinese manufacturers (MOQ typically under 500 units). First-purchase breakeven is fast; the LTV story starts on order two.

Insulated tote + drink dispenser — the rare summer product that doesn't go dark in September

Demand signal: ⭐⭐⭐⭐ · Competition: Low–medium · Cold-start rating: ⭐⭐⭐⭐

Most summer products are purely seasonal — the signal vanishes by Labor Day. The insulated tote bag with a built-in drink dispenser has a structural reason to avoid that collapse: the tote itself is a year-round carrying object; the dispenser function is the seasonal differentiator. The consumer isn't buying a seasonal item; they're buying a tote that's also useful at cookouts.

Demand has grown for four consecutive weeks since mid-May 2026, with FFOrder and Tradelle identifying the category independently. 1 The search peak is projected to land in the June 23–July 4 window — which puts the opening of Prime Day tomorrow at the precise start of that peak. 1

Prime Day's outdoor and hydration board is directly adjacent. YETI, Stanley, and Hydro Flask are confirmed deal categories at up to 50% off. 3 That promotional volume signals active consumer intent around exactly the category of product a dispenser tote competes in — at a price point ($32–45 retail) well below the premium brand tier.

Gross margin estimate: 60–68% (USD, as of Q2 2026). 1 Sourcing specifications: triple-wall insulation, BPA-free PEVA lining, 48-hour valve leak test. TikTok Shop is the primary acquisition channel here — the product shows well on video (condensation visible on the exterior, clean pour from the spout), and the platform's audience skews exactly toward the outdoor lifestyle demographic.

Competition check: The mid-tier price band ($32–45) has a visible supply gap. Below it, cheap generic cooler bags. Above it, premium outdoor brands (YETI, Stanley) that are not positioned around the dispenser function as a primary feature. The hybrid product identity — tote that carries and pours — has no current brand claiming it.

Key risk: FFOrder's analysis is direct about the brand requirement: "Generalist stores without a lifestyle brand fail this SKU." 1 A product listing alone without consistent outdoor lifestyle content — picnic videos, farmers market routines, beach prep content — will not convert at the $32–45 price point. The ad CPM in this category rises sharply in June; sellers who haven't built any organic TikTok presence before running paid ads face a cost structure that erases the margin.

Cold-start entry: This is a TikTok-first build, not an Amazon-first one. Start with 3–5 organic posts (real-use outdoor settings, no heavy editing) before running any paid spend. Retail at $36–42. The supplier quality check on the valve mechanism is the one non-negotiable sourcing step — a leaking dispenser generates returns that destroy early unit economics.

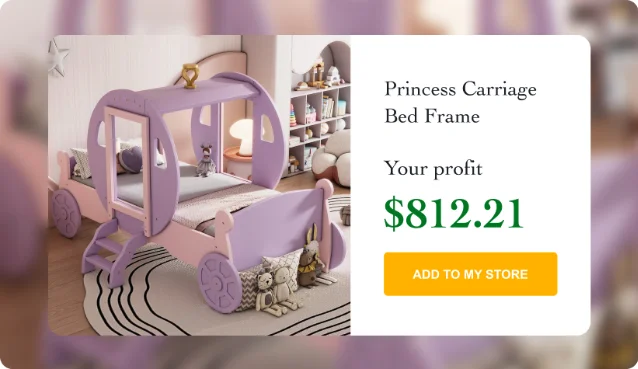

Kids' furniture small-SKU — five consecutive weeks

Demand signal: ⭐⭐⭐⭐⭐ · Competition: Medium (sub-niches open) · Cold-start rating: ⭐⭐⭐⭐

A product category cluster that has shown up on AliDropship's weekly bestseller list for five straight weeks without a single DTC brand filling the space is unusual enough to take seriously.

The five entries across five weeks: Princess Carriage Bed Frame (June 17–23, first appearance), Kids Bunk Bed (June 10–16), Kids Bookshelf with Reading Nook (June 3–9), Montessori Floor Bed (May 27–June 2), and Wood Montessori Bed (April 22–28). 4 Five separate SKU entries, five consecutive weeks — the longest sustained cluster in the current scan dataset. The Princess Carriage Bed Frame is the fourth distinct SKU variant in this cluster, appearing for the first time this week.

Prime Day adds a seasonal catalyst. Amazon's back-to-school category is a confirmed Prime Day 2026 deal board — this overlaps directly with the mid-year furniture upgrade window that families undertake before the school year. 3 Retail price validation from adjacent channels: Montessori Floor Bed at Macy's retails at $431 (20% off original price), Etsy Montessori toddler floor bed listings at $648–810. 4 Demand is clearly there at price points that support real DTC margins.

The cold-start divide in this category is structural. Large items — full-size bunk beds, carriage beds, floor beds — carry high AOV but also high freight complexity, damage-in-transit risk, and assembly complaint rates. Those belong on a watchlist, not a cold-start entry list. The viable entry points are the parcel-shippable sub-niches:

- Kids' bookshelf + reading nook combos ($65–120): flat-pack, parcel-shippable, high visual appeal on Instagram and Pinterest

- Montessori-style low shelving units ($45–85): strong creator community around Montessori parenting content

- Wooden play kitchen accessories ($35–65 per piece): light, high AOV via bundling, gift-purchase friendly

Competition check: The broader kids' furniture market is established and competitive. But specifically within the reading-nook and Montessori-aligned sub-niches, no dominant DTC brand has been identified across this five-week tracking window. Amazon search results in these sub-niches show fragmented generic sellers — no brand with recognizable identity, content presence, or repeat-purchase positioning. The signal is currently AliDropship-only; independent Amazon BSR validation is recommended before scaling ad spend.

Key risk: Single-source demand signal. Freight logistics set a hard ceiling on which SKUs are viable — anything requiring LTL freight is off-limits for cold-start without prior fulfillment infrastructure.

Cold-start entry: Start with one flat-pack bookshelf or reading nook unit at $75–110 retail. MOQ under 100 units from AliExpress or a direct factory. Build the brand around educational-parenting content — Montessori philosophy, reading routine formation. The next four days are a useful window to test Amazon ad efficiency at lower CPCs before Prime Day pulls costs upward.

GLP-1 muscle preservation supplements — five consecutive weeks confirmed

Demand signal: ⭐⭐⭐⭐ · Competition: Zero DTC brands — white space confirmed · Cold-start rating: ⭐⭐⭐⭐

The core finding has not changed. For the fifth consecutive week, no DTC brand offering a creatine + leucine supplement bundle explicitly positioned for GLP-1 drug users has been identified across any search path. The white space is still open. What did change this week is the size of the market behind it.

Research Intelo published a GLP-1 Companion Nutritional Supplements market report on June 19, 2026. The figures: global market at $200M in 2025, projected to reach $1.1B by 2034, CAGR of 20%. 5 North America accounts for 62% of current revenue — approximately $124M. 5 US GLP-1 active users exceeded 9 million as of Q1 2026. 5 The report characterizes the segment as "what many industry analysts are calling the most consequential new segment in functional nutrition since plant-based protein." 5

Exploding Topics' June 2026 data reinforces the upstream search behavior: Creatine Gummies at +5,400% and Magnesium Glycinate at +3,900% are both top-100 trending topics. 6 Neither search trend has been converted into a GLP-1-positioned DTC brand. Creatine gummies in particular sit at the exact intersection of "existing consumer behavior" (familiar supplement form factor) and "new positioning opportunity" (GLP-1 muscle support framing).

Competition check: The landscape has not closed. Herbalife, currently the market's leading brand, operates via MLM rather than DTC. 5 General fitness brands (Transparent Labs, MuscleTech) are not GLP-1 positioned. GLP-1 weight-management products (Nutrex, Vitamin Shoppe's GLP-1 line) target appetite suppression and fat loss, not muscle preservation. No brand bridges both sides. Protein-focused formulations represent 48.5% of the current market by revenue — the positioning roadmap for a creatine + leucine bundle is clear. 5

Key risk: Week five is not week one. Any established supplement brand — Momentous, Thorne, Ritual — can enter this positioning with a single product launch and immediately outcompete a new DTC entrant on credibility and retail distribution. Five weeks of confirmed white space is meaningful. It is not indefinite.

Cold-start entry: Private-label creatine monohydrate + leucine + electrolyte blend from US or China-based contract manufacturers, MOQ under 500 units. FTC compliance requires positioning as "muscle support during caloric restriction" — the standard regulatory framing that avoids naming GLP-1 drugs directly. Retail: $38–55 per 30-day supply. The content path: r/Semaglutide and r/GLP1 have consistent creatine and leucine discussion threads where no brand is repeatedly named. That is a community waiting to be served.

Levitating / magnetic home decor — TikTok's current visual native

Demand signal: ⭐⭐⭐⭐ · Competition: Low · Cold-start rating: ⭐⭐⭐⭐

Some product categories earn their attention through search data. This one earns it through a different signal: a Quicksand Gravity Lamp video accumulating 3.3 million TikTok likes without a word of voiceover. 7 The content creator turned on the lamp and let the visual do the work.

AutoDS ranks Levitating Succulent as its #1 June 2026 dropshipping pick, citing the product's trifecta of minimal home decor appeal, novelty factor, and suitability for the exact aesthetic (apartment, desk setup, gift) that performs on TikTok. 7 TrueProfit independently named the broader "sustainable mushroom lamp" category — which overlaps with this decor segment — as one of 2026's ten low-competition niches. The category spans several related SKUs: levitating succulent planters, levitating candleholders, magnetic floating globes, and gravity/sand hourglass lamps.

Competition check: The category is pre-brand. AliExpress carries magnetic levitation base suppliers at commodity prices, and the current TikTok presence is overwhelmingly UGC and reseller content — no brand with a recognizable name, aesthetic identity, or direct-to-consumer website has claimed this space. The "gifting" angle (floating planter as a desk or housewarming gift) is particularly under-served: no brand has built around it.

Key risk: TikTok novelty categories have a specific failure mode — the product goes viral, 40 dropshippers immediately list it at $19.99, and price collapse follows within 30–60 days. The window between "this works on TikTok" and "everyone is selling it" is shorter than most sellers expect. Entry this week is closer to early than entry next week will be.

Cold-start entry: Source the levitation base mechanism from AliExpress (suppliers readily available, MOQ typically 20–50 units for base modules). Retail target: $35–55 for a levitating planter set, $45–70 for a gravity lamp. COGS: $8–15 depending on mechanism quality. The content strategy is the product — a single well-shot 15-second clip of the floating mechanism in a real home setting is the entire acquisition funnel. Build that first; don't run ads before it converts organically.

Watchlist updates

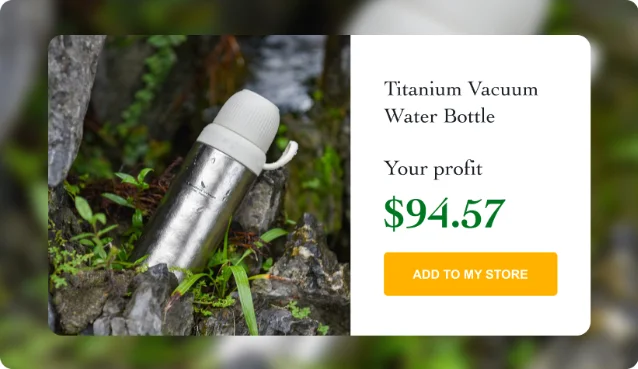

Titanium drinkware — restored to active watch. Last week's issue flagged the category as cooling after a one-week absence. The correction: Titanium Vacuum Water Bottle reappeared on the AliDropship May 27–June 2 list, confirming the prior week's absence was a gap in a biweekly recurrence pattern rather than a category cool-down. 4 No DTC brand launch has been detected in associated search paths. The material-differentiation thesis (titanium vs. stainless steel at a premium price point) remains unoccupied. Status: active watch, not a recommended cold-start entry this week but flagged for the next signal update.

LED smart vanity mirrors — week 9, new convergence signal. LED Lighted Vanity Mirror appeared on the June 10–16 AliDropship list. 4 That is nine consecutive weeks of LED or smart mirror variants on the list — 15+ appearances total across six months. New this week: a Modern Vanity Desk appeared for the first time on the June 17–23 list, described as a "multifunctional vanity combining storage, lighting, and style." 4 That is a convergence signal — two distinct product forms (mirror, desk) pointing toward the same home-beauty functional space. The $100–150 DTC premium tier remains vacant; the desk appearance suggests the addressable category may be broader than "LED mirror" alone.

Rattan/boho — week 8, signal shifting from organizers to furniture. The category persists on AliDropship: Rattan Coffee Table (June 10–16 and May 27–June 2), Rattan Shoe Cabinet (June 3–9), Rattan Furniture Set (May 20–26). 4 The organizer-specific signal (rattan storage baskets, desktop organization) has not strengthened; the broader rattan furniture signal has. The original entry thesis — small rattan organizers at $25–45 as a low-MOQ, aesthetic-led cold-start — remains structurally valid, but the category's AliDropship signal is now more accurately described as "rattan furniture" than "boho organizers." No dedicated DTC rattan brand identified this week.

HAP remineralizing gum — no change. ChewingGumReviews.com's "Top 10 Best Remineralizing Gums 2026" ranking was last updated January 23, 2026 and remains unchanged. 8 Approximately 10 brands, two nano-HA formulations (Underbrush, Enamio/Larine). Exploding Topics shows the Remineralizing gum search trend at +5,100%. 6 No new US-native DTC entrant was detected this week. The white space at the nano-HA end of the market persists, but competition is no longer sparse at the functional gum level.

Next watch

Prime Day is a category velocity test, not just a sales event. Watch which categories see listing volume and search ranking changes in the 48 hours after June 26 — that post-event data identifies which product types saw genuine conversion rather than browsing. The air fryer liner halo, the outdoor tote demand peak, and the kids' furniture back-to-school overlap will all be legible in the post-Prime Day signal within 72 hours.

GLP-1 week 5 is the harder constraint. Five consecutive weeks of confirmed white space is unusual in supplement categories where entry costs are low and market intelligence is widely available. That gap will close — the question is whether it closes because a new DTC entrant moves first or because an established brand (Momentous, Thorne, Ritual) publishes a single GLP-1-positioned SKU and captures the positioning with existing distribution. Week 6 is worth watching closely.

Cover image: AI-generated.

参考来源

- 1FFOrder: Best Dropshipping Products June 2026

- 2CJdropshipping: 10 Best Dropshipping Products June 2026

- 3About Amazon: Prime Day 2026 deals preview

- 4AliDropship: Best Dropshipping Products To Sell Now

- 5Research Intelo: GLP-1 Companion Nutritional Supplements Market Report 2034

- 6Exploding Topics: Top Trending Topics Jun 2026

- 7AutoDS: Best Items to Dropship in June 2026

- 8ChewingGumReviews.com: Top 10 Best Remineralizing Gums 2026

围绕这条内容继续补充观点或上下文。