GRND — hard screening metrics (TTM through March 31, 2026)

All four filters pass. TTM revenue growth is borderline at 31.02% — 102 basis points above the 30% threshold. PEG verified under two Forward P/E sources; both readings clear 1.0.

Grindr Inc. (NYSE: GRND) is Pass #24 in the daily small-cap screen — and the first pure social/dating platform in the series. The world's largest LGBTQ+ platform runs at 73% gross margins and 45% adjusted EBITDA margins on $475.9M TTM revenue, with $151M in operating cash flow generated by 165 employees. All four hard filters pass: $2.07B market cap ✅, 31.02% TTM revenue growth ✅ (borderline — 102bps above threshold, documented), PEG 0.57/0.73 dual-verified ✅, OCF +$151.19M ✅. The article fully documents the D/E 470× anomaly (buyback-driven negative equity artifact, actual Debt/EBITDA 2.55×), the 29.58% short float, the Match Group/$100M Sniffies competitive risk, and the 6-analyst consensus target of $18.20 (+56% upside).

| Filter | Threshold | Value | Source(s) | Status |

|---|---|---|---|---|

| Market cap | < $10B | $2.07B | Finviz, StockAnalysis | ✅ Pass |

| TTM revenue growth | > 30% | 31.02% | Finviz, StockAnalysis | ⚠️ Borderline — 102bps above threshold |

| PEG ratio | < 1.0 | 0.57 (Finviz) / 0.73 (manual) | Finviz; see decomposition below | ✅ Pass |

| Operating cash flow | Positive | +$151.19M TTM | StockAnalysis | ✅ Pass |

| Input | Value | Source |

|---|---|---|

| Forward P/E | 15.37× (Finviz) / 19.77× (StockAnalysis) | Finviz / StockAnalysis |

| EPS 5-year growth estimate | 27.12% | Finviz |

| PEG (Finviz method) | 0.57 | Forward P/E 15.37 ÷ 27.12% |

| PEG (manual cross-check) | 0.73 | StockAnalysis Forward P/E 19.77 ÷ 27.12% |

| TTM revenue | $475.90M | Finviz, StockAnalysis |

| TTM OCF | $151.19M | StockAnalysis |

| TTM FCF | $150.54M | StockAnalysis |

| Quarter | Revenue | YoY growth | Adj. EBITDA margin |

|---|---|---|---|

| Q1 2024 | $75.4M | +35.0% | — |

| Q2 2024 | $82.4M | +33.8% | — |

| Q3 2024 | $89.3M | +27.1% | — |

| Q4 2024 | $97.6M | +35.4% | — |

| Q1 2025 | $93.9M | +24.7% | ~43% |

| Q2 2025 | $104.2M | +26.6% | — |

| Q3 2025 | $115.8M | +29.6% | — |

| Q4 2025 | $126.0M | +29.0% | — |

| Q1 2026 | $129.9M | +38.3% | 45.0% |

| FY2026E | ≥$535M guided | ~+22% implied | ≥$227M guided |

| Metric | Finviz | StockAnalysis | Context |

|---|---|---|---|

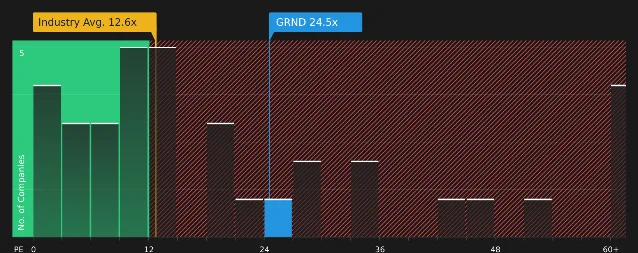

| Trailing P/E | 23.40× | 25.94× | Industry avg: 12.6× (see chart below) |

| Forward P/E | 15.37× | 19.77× | Convergence if FY2026 earnings meet guidance |

| EV/EBITDA | 15.86× | 16.05× | Two sources consistent |

| P/S (TTM) | 4.35× | 4.35× | Two sources consistent |

| P/FCF | 13.64× | 13.74× | Reasonable for a 45%-EBITDA-margin business |

| PEG | 0.57 | 0.73 (manual) | Both below 1.0 |

| Gross margin | 73% | — | SaaS-tier for a consumer app |

| Operating margin | ~31% | — | FY2025 TTM; Q1 2026 margins expanding |

| Metric | Value (Mar 31, 2026) | Context |

|---|---|---|

| Cash & equivalents | $23.81M | Down from $87.1M at FY2025-end; buybacks consumed ~$438M TTM |

| Total debt | $393.29M | $20M current + $371.1M long-term; credit facility expanded to $600M Dec 2025 |

| Net debt | $369.48M | Debt/EBITDA 2.55× |

| Interest coverage | 7.34× | Healthy relative to debt load |

| TTM OCF | $151.19M | Covers annual interest ~4.5× on annualized interest expense |

| TTM FCF | $150.54M | Near-perfect OCF conversion (minimal CapEx) |

| Current ratio | 1.32× | $104.5M current assets vs. $79.4M current liabilities |

| Book equity | $839K | Near-zero; consequence of $438M buyback program |

| Risk | Severity | Impact path |

|---|---|---|

| TTM growth deceleration below 30% | 🔴 High | FY2026 guidance implies ~22% full-year growth. If H2 2026 comes in at 18–20% YoY, TTM growth falls through 30% by Q3 2026 — the screen fails at that TTM snapshot. Growth-story premium on valuation would compress. |

| Match Group / Sniffies competitive threat | 🟡 Medium | On April 28, 2026, Match Group (Tinder/Hinge parent) invested $100M in Sniffies, a web-only LGBTQ+ cruising platform with ~3M MAU and 60M monthly page visits growing 60% YoY. Match also received a future acquisition option. Sniffies targets a distinct use case from Grindr's (anonymous, no app store restrictions), but Match's capital and distribution expertise behind a directly adjacent platform is the most concrete competitive development in at least three years. 12 |

| Insider selling with no offsetting buyer | 🟡 Medium | James Lu, a >10% beneficial owner, sold approximately $43M in shares in January–February 2026 at $10.01–$13.53. Following the Q1 2026 earnings beat on May 7, no insider executed any open-market purchase. Only equity grants (at $0 cost) appear in the Form 4 filings. The absence of any post-earnings insider buying at the current price (~$11.64) is not a positive sentiment signal. 13 |

| High short float — squeeze or fundamental signal | 🟡 Medium | Finviz reports 29.58% of float short (28.33M shares, days-to-cover ~5); StockAnalysis reports 17.50% (47.90M float, different float definition). Absolute short position: 8.38M shares (~$97.5M). The divergence in float definitions reflects the high insider ownership (~73–84%), which leaves a thin tradeable float. This is a two-sided dynamic: a sharp positive catalyst could compress short positioning quickly (84% insider ownership, thin float), but the short interest also represents informed bearish capital betting against the current price. |

| Debt-funded buyback strategy | 🟡 Medium | Grindr spent $438M on buybacks over TTM while generating $151M in OCF — implying ~$287M in buybacks was funded by the credit facility rather than cash flow. The $600M facility expanded in December 2025. If OCF compresses (e.g. growth slows, costs rise), the buyback program would need to pause, and the remaining credit facility draws would need to be serviced from reduced cash flow. Debt/EBITDA of 2.55× is manageable at current earnings; it is not manageable if EBITDA falls 40%+. |

| Regulatory and privacy exposure | 🟢 Low-medium | Grindr was fined by Norway's data protection authority (Datatilsynet) in 2021 for sharing user data without consent. The FY2024 10-K lists privacy/data security, GDPR compliance, and the global spread of anti-LGBTQ+ policies as material risk factors. Application bans or restrictions in new jurisdictions would reduce MAU directly. 14 |

| Catalyst | Expected timing | What to watch |

|---|---|---|

| Q2 2026 earnings | ~August 6–7, 2026 (estimated) | Revenue vs. implied run-rate of ~$133–135M (+27–30% YoY); whether 38% Q1 acceleration was a one-quarter anomaly or a sustained trend |

| Edge global launch | Late 2026 / early 2027 | Pricing tier, uptake rate, ARPU lift vs. Xtra; any early metrics from staged rollouts |

| Madonna Confessions II album release | July 3, 2026 | Whether the partnership drives measurable app installs or subscription conversions — a metric Grindr has not yet disclosed publicly |

| Sniffies product development | Ongoing | Whether Match Group's $100M investment accelerates Sniffies' user growth and competitive positioning vs. Grindr's core base |

| Short position resolution | Ongoing | 8.38M shares short with ~5-day cover at current volume; either a forced unwind (positive) or a fundamental disappointment driving further covering demand (negative) |

围绕这条内容继续补充观点或上下文。