June 18 settlements: oil bounces on Versailles, gold sinks on Warsh

COMEX Gold GCQ6 fell to $4,227.90 (−1.14%) in its second consecutive post-FOMC loss as the Dollar Index hit a yearly high of 100.82 and CME FedWatch repriced September rate-hike odds to ~67%. WTI CLN6 rebounded $1.03 to $76.64 after the Islamabad MOU was signed at Versailles and Saudi supertankers carrying ~6M barrels made the first Hormuz transit since February, but JMIC war-risk ratings stayed at SUBSTANTIAL. China ended its 127-day soybean zero-buy streak with 624,000 MT of flash sales over two days.

Data as of June 18, 2026 final settlements and electronic-session closes. All times ET.

Trump signed the 14-point Islamabad Memorandum of Understanding at the Palace of Versailles — not Geneva, not even close — skipping the planned June 19 ceremony and starting the 60-day negotiating clock two days early. 1 The reaction in commodity markets was messier than the headline suggests: oil recovered from a session low that touched the cheapest level since the war began, gold posted its second consecutive post-FOMC loss to close at $4,227.90, and corn gave back Wednesday's gains on a combination of profit-taking, bearish Corn Belt weather, and a macro backdrop that had traders squaring books before the Juneteenth holiday.

The through-line is the Federal Reserve. Fed Chair Kevin Warsh's debut FOMC press conference Wednesday stripped the policy statement from ~300 words to 130, removed forward guidance entirely, and signaled a committee that considers itself "unambiguous and unanimous" on price stability. 2 By Thursday afternoon the CME FedWatch tool showed a ~67% probability of a September rate hike, up sharply from roughly 40% before the June 17 FOMC decision, with December tightening probability at ~83–85%. 2 A dollar that hit its highest close in more than a year at DXY 100.82 did the rest of the damage to gold and grain-complex price signals. 3

June 18 settlement snapshot

| Contract | June 18 close | D/D change | D/D % |

|---|---|---|---|

| COMEX Gold GCQ6 (Aug) | $4,227.90 / oz | −$48.70 | −1.14% |

| NYMEX WTI CLN6 (Jul) | $76.64 / bbl | +$1.03 | +1.36% |

| ICE Brent BZN6 (Aug) | $79.26 / bbl | +$0.60 | +0.76% |

| CBOT Corn ZCN6 (Jul) | 417.50¢ / bu | −3.50¢ | −0.83% |

| CBOT Soybeans ZSN6 (Jul) | 1,122.00¢ / bu | −10.00¢ | −0.88% |

| COMEX Copper HGN6 (Jul) | $6.385 / lb | +$0.009 | +0.14% |

Baselines: Gold $4,276.60; WTI $75.61; Brent $78.66; Corn 421.00¢; Soybeans 1,132.00¢; Copper $6.376. Sources: 4 5 6 7 8 9

Macro backdrop: Warsh reprices the rate path

The equity side of Thursday's session looked almost festive — the S&P 500 closed at 7,500.58 (+1.08%), Nasdaq at 26,517.93 (+1.91%), and the VIX fell to 16.40, its largest single-day drop in weeks at −11.06%. 10 11 Semis led the recovery: Intel surged +10.6% on a Trump-announced Apple chip partnership, SNDK +11.5%, SMCI +10.4%. The Dow added only 72 points to 51,564.70. 12

That optimism did not reach the commodity complex. The dollar's surge to 100.82 and a 37bps repricing of cumulative Fed hikes through year-end act as a tax on every dollar-denominated raw material. The 10-year Treasury yield fell 4bp to 4.460% as risk-on rotation pulled capital out of safe havens, 13 while the 2-year held flat near 4.187%. 14 Weekly jobless claims came in at 226K, essentially in line with estimates of 225K. 12

The market's Warsh read continues to evolve in real time. Ed Yardeni (Yardeni Research) said he was "blown away" — he had expected a relatively dovish Fed chair who would emphasize AI-driven productivity, but instead got a "strict, orthodox message on inflation with a strong commitment to price stability." 2 Scott Clemons of Brown Brothers Harriman offered the counterpoint: "Far be it for me to disagree with the futures market, but I would be surprised if the Fed raises interest rates this year. It is an election year." 2 Scotia Wealth's morning note flagged the core tension: Warsh may be using hawkish signaling deliberately to establish initial credibility, with more flexibility available later. 15

Today was also the largest options expiration in history, with roughly $8.3 trillion in notional exposure rolling off — 18% larger than the prior December record of $7.1 trillion. 12 The Bank of England held at 3.75% in a 7-2 vote, with chief economist Huw Pill and Megan Greene dissenting for an immediate 25bp hike. 16

Oil: Versailles bounce off a four-month low

The MOU was signed at Versailles on the evening of June 17, with Trump and Macron present at the dinner table. 1

WTI CLN6 ended at $76.64, bouncing $1.03 from Wednesday's settlement after four consecutive losing sessions that had taken it down roughly 11% on the week. 5 Volume collapsed to just 49,400 contracts — about 30% of its 65-day average — as the contract heads toward its June 22 expiry. CLQ6 (August) is already the more actively traded WTI tenor at $75.57. Brent BZN6 finished at $79.26, after the intraday low of $76.54 became the cheapest Brent print since the war started in February. 6

The session's key catalyst was VP JD Vance, who issued an unexpectedly direct White House rebuke to Israeli officials criticizing the MOU, warning: "Donald J. Trump is the only head of state in the entire world who is sympathetic to the nation of Israel at this moment in time. If I was in the cabinet of the Israeli government, I might not be attacking the only powerful ally that I have anywhere left in the entire world." 17 Oil recovered on that statement — it briefly reduced the probability that Israel's Lebanon posture blows up the deal.

Three Saudi-flagged Bahri supertankers carrying approximately 6 million barrels transited the Strait of Hormuz on Thursday morning, the first Saudi crude movement since the US-Israeli strikes on Iran began on February 28. 18 The vessels ran dark — AIS transmitters off — reactivating after clearing into the Gulf of Oman. Windward reported 18 total transits in the roughly 20-hour window between 6 PM June 17 and 2 PM UTC June 18, of which 10 were outbound vessels that had been stranded inside the Persian Gulf for 109 days. 18

Windward chief analyst Michelle Wiese Bockmann called the transits "a very good sign, an early sign that there is confidence for outbound transits," while acknowledging it would "start as a trickle." 18 Ben Cahill (Atlantic Council) put the test more bluntly: "Agreements on paper don't matter much unless they really get oil moving again through the Strait of Hormuz, because that's what everyone will be monitoring." 18

Three major obstacles to full normalization remain, all visible today:

- Insurance: The Joint Market Intelligence Committee (JMIC) war-risk rating stayed at SUBSTANTIAL — two full grades above the MODERATE threshold that would trigger premium normalization. War-risk surcharges remain at 3–10% of hull value versus under 1% pre-war. Bockmann said it was "too early to say" whether rates will start coming down. 20

- Mine clearance: MOU Article 5 requires demining within 30 days, but G7 allies were still reluctant to deploy minesweepers as of mid-week, and no start date or operator had been confirmed by June 18. 18

- Israel: The IDF published a forward-defense map Thursday showing control zones up to 10 km inside southern Lebanon, and Israeli National Security Minister Ben-Gvir posted publicly that "Trump's agreement does not bind us." 21 Iran has stated that continued Israeli occupation of Lebanese territory constitutes an MOU violation that would nullify the deal. 22

John Kilduff (Again Capital) framed the binary cleanly: "Full resumption of oil flows through the strait has been priced back in. Anything short of that will be a problem." 23 Goldman Sachs' Jerome Dortmans said the market will likely "grind lower" but "this is by no means over" — Goldman's floor estimate sits at $70–75/bbl initially, with BNP Paribas placing a "durable floor" at $75. 24

The EIA inventory data underlying that floor thesis remains tight: the week ending June 12 recorded a 10th consecutive weekly crude draw of 8.3 million barrels, bringing commercial stocks to 418.2 million barrels — 6% below the five-year average and the lowest level since 1985. 25 Cushing stocks sat near 20 million barrels, also the lowest in years. 25

Russia supply overhang

Ukraine struck Moscow with a record 555 drones Thursday morning, hitting the Gazprom Neft refinery at Kapotnya — 16 km from the Kremlin — for the second time in three days. 26 27 Four Moscow airports suspended operations. The Kapotnya facility supplies roughly one-third of Moscow's fuel and had not fully recovered from Tuesday's strike.

Russian refining capacity has dropped below 4 million barrels per day — a 21-year low per Energy Intelligence. 28 Fuel shortages now span 25+ regions, and Russia is importing gasoline by sea for the first time. The UAE's exit from OPEC+ (effective May 1, with plans to lift output above 5 mb/d) means the cartel has lost one of its few members with meaningful spare capacity precisely when post-Hormuz supply management matters most. 29

Gold and silver: Day 2 post-FOMC selloff

COMEX Gold GCQ6 (August) settled at $4,227.90, down $48.70 (−1.14%) and the lowest close since before the Fed meeting. 4 The two-day drawdown from the June 16 peak at $4,354.20 now totals roughly $126 — the FOMC's hawkish turn has erased two weeks of safe-haven premium. 30 Intraday range was wide at $4,220.30–$4,350.20, and volume was extreme at 135,490 contracts — 290% of the 65-day average. 4 The 200-day exponential moving average, which sits near $4,200, is now the key technical floor to watch. 31

The immediate driver is mechanical: rate hike expectations rose to 37bp of cumulative tightening priced through year-end, the DXY hit its highest close in over a year at 100.82, and gold-financing costs moved in lockstep. 15 Warsh's statement used the phrase "price stability" 12 times in a 40-minute press conference and opened five Fed task forces, but ruled out changing the 2% inflation target. 2 His exact framing: "Persistently high prices are a burden for the American people, but the recent past need not be prologue." 32

Silver fell harder. July silver futures opened at $68.04, down 3.8% from Wednesday's close of $70.76, and traded to a low of $66.96 by mid-morning. 33 34 The gold/silver ratio widened to approximately 63:1. Yahoo Finance's Tim Manni noted that silver investors are "more focused on inflation levels... and on the Fed seriously considering raising borrowing costs later this year" than on the Iran peace news. 33

The structural gold demand backdrop remains supportive but acted as no floor today. The World Gold Council's April data (published June 3) showed central banks resumed net purchases of 19 tonnes, led by Poland (+14t, bringing its total to 595t) and China's PBOC (+8t, extending an 18-month buying streak to a total of 2,322 tonnes). 35 Structural buying coexists with rate-sensitive liquidation in the short run.

Copper: range-bound flat

COMEX Copper HGN6 settled near $6.385/lb, +$0.009 (+0.14%) from Wednesday's close — essentially unchanged in very thin after-hours data. 9 Copper has been range-bound since the start of May according to Neil Sethi's chart analysis, with the Iran deal having provided a floor above $6.35 after a brief dip below $6.15 when Middle East tensions escalated earlier in June. 16

Jefferies reiterated its structural supply-deficit thesis this week, projecting an average annual shortfall of 491,000 tonnes through 2030, citing slower-than-expected production recovery at the Grasberg mine. 36 Potential US import tariffs on copper remain a second upside risk premium embedded in current pricing.

Grains: China soybean return faded by profit-taking

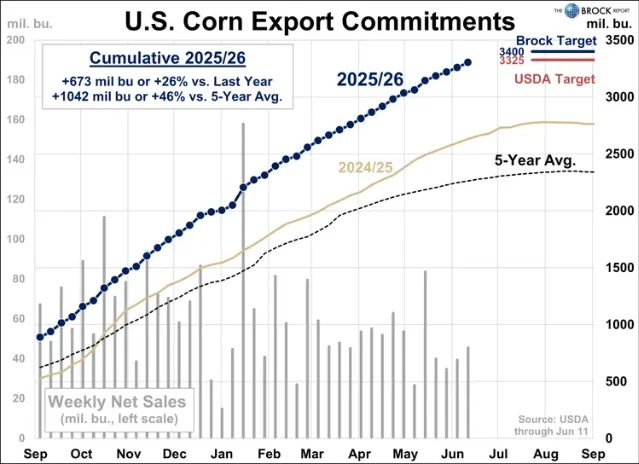

The day's most structurally significant development for grain traders was a USDA confirmation that had been feared and hoped for in equal measure: China broke its 127-day zero-buy soybean streak. USDA FAS reported flash sales on June 18 of 132,000 MT of soybeans to China (2026/27 crop) and 120,000 MT to unknown destinations (likely also China-directed), 37 on top of Wednesday's 372,000 MT to unknown destinations. 37 The two-day total of 624,000 MT represents the largest burst of US soybean demand from China in months. USDA also confirmed 285,775 MT of corn sold to Mexico on June 18. 37

The weekly export sales report released at 8:30 AM ET showed old-crop soybean net sales of 424,900 MT for 2025/26 — comfortably above analyst expectations of 100,000–300,000 MT. 38 Combined old- and new-crop soybean commitments of 729,000 MT landed on the higher end of the 400,000–850,000 MT analyst range. Corn net sales reached 1.157 MMT for 2025/26, up 16% from the prior week. 39

The bullish USDA data did not save prices. CBOT Corn ZCN6 settled at 417.50¢, down 3.50¢ on the day, and soybeans ZSN6 at 1,122.00¢ (−10.00¢, or −0.88%). 7 8 Mark Schultz (Northstar Commodity) said the 4.85 million bushel China flash sale was "too small to move the market — we need a lot more demand to really shift the trend." 40 Karl Setzer (Consus Ag Consulting) called out the real culprit: "Consolidation was the primary objective of trade today... This was the final trading session for the week, elevating contract squaring as US markets will be closed tomorrow for the Juneteenth holiday." 38

Soybean implied volatility (SVL) rose 0.44 to 20.71, a one-month high. Corn CVL jumped to 30.61 — also a one-month high — as the option market repriceed weather uncertainty ahead of the late-June to early-July pollination window. 41 DTN estimated heavy fund long liquidation in bean oil of as much as 15,000 contracts by noon, which dragged July bean oil to 69.69¢ (−185 points), a two-month low, and pulled soybean meal to $301.30 (−$3.50), a 4.5-month low. 42

Weather: bearish near-term, El Niño the longer tail

Near-term Corn Belt weather is bearish for prices. World Weather Inc. said soybean yield potential will remain "very high" through the next two weeks, with regular Midwest rain and mild temperatures. Pro Farmer editors summarized it directly: "Very good growing conditions over most of the Corn Belt are squelching the bulls. Extended weather forecasts for the Corn Belt are reaching out into early July with no significant perils seen for the US corn crop." 39

NOAA officially confirmed El Niño on June 18, reporting a 63% probability that this event ranks among the largest in the historical record since 1950. 43 NOAA's Jon Gottschalck said the near-term US agriculture impact is generally beneficial — El Niños bring heavier rainfall to the South and keep Corn Belt temperatures moderate — but the 63% historic-magnitude probability sets up re/insurance repricing as the event is expected to peak in late fall or early winter 2026. UN Secretary-General António Guterres issued the broader warning: "El Niño conditions will pour fuel on the fire of a warming world." 43 Tropical Storm Arthur's remnants continued dumping 5–10 inches of rain across the Gulf Coast (Louisiana, Mississippi, Alabama), with isolated totals approaching 20 inches — no Corn Belt threat, but HRW wheat harvest progress in Kansas (28% complete) and Texas (75% complete) faces continued interference from repeated rain bands. 44

Jim Wiesemeyer (AG Bull) made a credibility argument for watching the China corn front next: "Beijing has allowed weeks to pass since the Trump/Xi summit with minimal follow-through on non-soybean commodities, creating political pressure to demonstrate good faith." A corn purchase would partially fulfill the $17 billion agricultural commitment. 45 Scott Varilek (Kooima Kooima Varilek) said he "can't confirm a low" in grains yet — the market needs more demand confirmation or a weather event before any trend reversal: "If we get to July 4 and we still had a dry spell here that was lingering we could put some weather premium in, but we just don't have that ability right now." 40

Positioning signals to watch after the Juneteenth weekend

- WTI roll: CLN6 expires June 22. With volume collapsing to 30% of average, the active contract shifts to CLQ6 ($75.57 Thursday). The spread between the two is the immediate structural signal for front-month positioning. 5

- Lebanon withdrawal deadline: Iran has explicitly conditioned MOU compliance on full Israeli withdrawal from Lebanon. 21 IDF published maps Thursday showing no intention to withdraw. Any diplomatic breakdown over the weekend would immediately revisit the $76 WTI floor.

- JMIC rating downgrade: The first reduction from SUBSTANTIAL toward MODERATE would be the clearest insurance-cost normalization signal. Bockmann at Windward said daily premium recalculation is ongoing but no directional shift has emerged. 20

- China corn: USDA flash sales run on a rolling basis. A corn purchase from China — even a partial tranche — would validate Wiesemeyer's credibility-pressure thesis and could break corn's downtrend before next week's Crop Progress report.

- CME FedWatch July probability: The July meeting hike probability sat at approximately 33% on June 18. 2 Any movement toward 50%+ without fresh inflation data would accelerate the DXY/gold relationship established this week.

- Demining timeline: No G7 minesweeper deployment had been agreed by June 18. The 30-day clock under MOU Article 5 runs from signing (June 17), making mid-July the contractual deadline for demining completion. The physical pace of Hormuz normalization depends on this more than on any headline count of transiting tankers.

Cover image: Trump signs the Islamabad Memorandum of Understanding at the Palace of Versailles during dinner with French President Emmanuel Macron, June 17, 2026. 1

参考来源

- 1Al Jazeera — Iran, US presidents sign deal

- 2CNBC — Markets are set for a much more hawkish Warsh Fed

- 3MarketWatch currencies

- 4MarketWatch GCQ26

- 5MarketWatch CLN26

- 6CNBC Brent BZN6

- 7MarketWatch Corn C00

- 8CME Soybean Futures Quotes

- 9CNBC Copper HGN6

- 10MarketWatch SPX

- 11MarketWatch VIX

- 12Investopedia — Markets News June 18 2026

- 13MarketWatch US 10Y Treasury

- 14MarketWatch US 2Y Treasury

- 15Scotia Wealth Management Morning Strategy Note

- 16Neil Sethi's Newsletter — As We Approach The Open 6/18/26

- 17NYT — Vance Defends Trump's Iran Deal, With a Blunt Warning to Israel

- 18RFE/RL — Iran Deal Provides Economic Boost, But Hormuz Shipping Is Key

- 19House of Saud — Hormuz Carried the First Saudi Barrel Since February

- 20House of Saud — The Strait Opened for One Country

- 21Middle East Monitor — Despite US-Iran deal, Israel says troops to remain

- 22Haaretz — IDF Presents Expanded Lebanon Occupation Zone

- 23Reuters — Brent rises after Vance warns Israel against breaking cease-fire

- 24Goldman Sachs — Why Oil Prices Could Grind Lower

- 25Yahoo Finance / Oilprice.com — US Crude Oil, Gasoline Inventories Still Falling: EIA

- 26Reuters — Ukraine brings the war to Moscow

- 27NPR — Ukraine hits Moscow in large-scale drone attack

- 28Bloomberg — Ukraine Launches Record Drone Attack on Moscow

- 29BankWatch Morning Briefing June 18

- 30CNBC — The Price of Gold Today, June 18, 2026

- 31Fortune — Current price of gold as of June 18, 2026

- 32RightxAlgo — Gold Crashed $100 in 15 Minutes

- 33Yahoo Finance — Silver prices today, Thursday June 18, 2026

- 34Fortune — Current price of silver as of June 18, 2026

- 35World Gold Council — Central banks resume net buying in April

- 36CapitalStreetFX — Hawkish Fed Lifts Dollar, Copper Near $6.42

- 37USDA FAS — Export Sales to China, Mexico, and Unknown Destinations

- 38Agriculture.com — Grains End Week in the Red, June 18, 2026

- 39Pro Farmer — Selling pressure returns to grain markets

- 40AgWeb — Grains see profit taking heading into the holiday

- 41CME Group — Corn Futures Quotes

- 42DTN — Periodic Updates on Grains, Livestock Futures Markets

- 43The Morning Sun / AP — El Nino is here and scientists fear it'll be big

- 44NBC News — Tropical storm remnants pound Gulf states

- 45AG Bull — Supreme Court decisions reshape agriculture

围绕这条内容继续补充观点或上下文。