Global Energy & Climate Weekly — May 26–June 1, 2026

Bonn SB64 opens June 8 with fossil fuel transition text in focus; India submits its 2035 NDC; OPEC+ approves a third 188,000 bpd hike that remains largely on paper as Hormuz stays closed; Brent seen averaging $90 in 2026; IEA confirms $3.4T global energy investment with solar at $365B; Rowan closes $3bn green data-centre debt; Orsted and HASI lock in 1 GW; CleanMax raises $575M in India.

As SB64 preparations enter their final week before Bonn, this issue tracks a cascade of market signals that cut across all four coverage areas: India files its 2035 NDC, OPEC+ ratifies a third straight output hike that exists largely on paper, and a new IEA report confirms $3.4 trillion in global energy investment for 2026 — two-thirds of it outside fossil fuels.

Climate summits & policy

SB64 opens June 8 in Bonn; NDC implementation dominates the agenda. The 64th sessions of the UNFCCC Subsidiary Bodies (SBI and SBSTA) will run June 8–18 at the World Conference Center in Bonn, Germany, convening national delegates, civil society groups, and technical experts ahead of COP31 in Antalya, Turkey in November. 1 The agenda centres on turning Paris Agreement pledges into verifiable national plans: climate finance mobilisation, NDC implementation pathways, adaptation and resilience frameworks, transparency and accountability mechanisms, and just transition roadmaps. A COP30 Mutirão decision also mandates that the first Climate and Trade Dialogue take place at SB64, with the SB Chairs set to host three such dialogues at intersessional meetings through 2026. 2

India submits its 2035 NDC — raising the non-fossil power target to 60%. India formally approved and submitted its updated Nationally Determined Contribution for the 2031–2035 cycle in late March 2026, committing to reduce emissions intensity of GDP by 47% relative to 2005 levels by 2035 and to raise the share of non-fossil-fuel-based installed electricity capacity to 60%. 3 The submission frames these goals as India's "highest possible ambition" and was filed through India's High Commission. 4 India's IEA-projected $170 billion in energy investment for 2026 — driven by solar and oil refining — gives the NDC concrete near-term backing; total non-fossil capacity is already approaching 500 GW.

Fossil fuel transition diplomacy: post-Santa Marta implementation scrutiny at Bonn. The IISD notes that one of SB64's sharpest tests will be whether the three workstreams launched at the Santa Marta conference — which covered coal, oil, and gas phasedown timelines — can produce draft decision text before COP31. 5 SB64 is also expected to recommend a draft decision on operationalising the Just Transition Mechanism for adoption in Antalya.

Energy transition

US renewables Q1 2026: 11% generation growth, 28.6% of total output. Renewable sources grew US electrical generation by more than 11% in the first quarter of 2026, accounting for 28.6% of all domestic output, according to the SUN DAY Campaign's review of federal data. 6 Utility-scale solar led at +23.9%, hydropower at +21.9%, small-scale solar at +11.9%, and wind at +2.1%. Combined wind and solar reached 20.3% of production, outpacing both nuclear (+14.3% margin) and coal (+31.1%). Coal generation fell 11.4% in the same period.

The EIA projects utility-scale renewable capacity will increase by 57,081 MW between April 2026 and March 2027, led by 42,626 MW of solar and 14,157 MW of wind (including 4,155 MW offshore). Battery storage is forecast to add another 23,524 MW over the same period, bringing installed US BESS capacity to nearly 70 GW by early spring 2027. 6

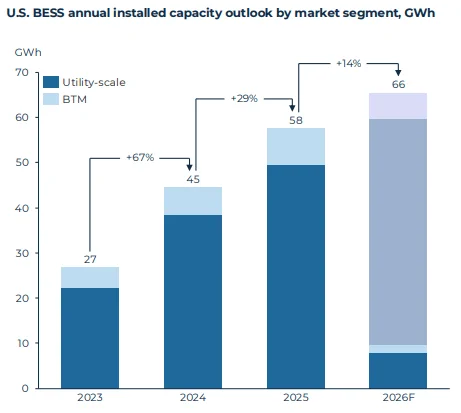

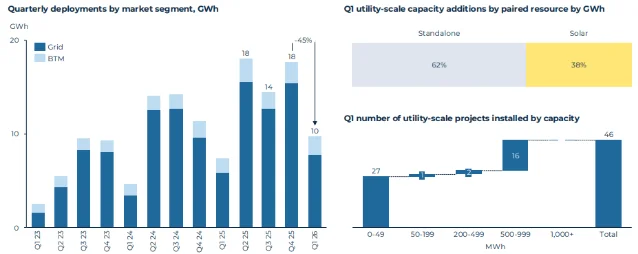

US BESS deployments up 32% year-on-year in Q1 2026. Nearly 10 GWh / 6.77 GW of utility-scale and behind-the-meter battery storage entered operation across the US in Q1 2026, a 32% increase on Q1 2025, according to SEIA data. 7 Utility-scale installations accounted for more than 75% of the total (7.8 GWh / 1.5 GW), and six states each deployed more than 500 MWh in the quarter. The sequential decline from Q4 2025's 18 GWh is partly attributed to seasonal project timing rather than underlying demand. Full-year 2026 BESS deployment is forecast at 66 GWh.

IEA's World Energy Investment 2026 confirms solar now commands $365B in annual spend. Released May 28, the IEA's flagship investment report sets total 2026 global energy investment at approximately $3.4 trillion. 8 Of that, roughly $2.2 trillion goes to low-carbon technologies, electricity infrastructure, and efficiency — around $665 billion in renewable power alone, with solar at $365 billion and wind at $200 billion. Grid investment approaches $550 billion; battery storage investment tops $100 billion. The report notes that the Hormuz disruption has acted as an accelerant for diversification investment: natural gas investment climbs to nearly $330 billion (a decade high), and nuclear is now receiving more than $80 billion per year globally across roughly 80 GW of new capacity under construction in 15 countries.

The underlying driver in the US context is stark: Q1 2026 saw more than 50 new utility-scale solar, wind, and battery projects announced as developers raced to meet the July 4 tax incentive eligibility deadline imposed by the One Big Beautiful Bill Act (OBBA), even as cancellations — exceeding 16.5 GW in Q1 alone — continue at historically high rates due to policy uncertainty and financing pressures. 9

Oil market dynamics

OPEC+ ratifies 188,000 bpd June hike — largely symbolic while Hormuz stays closed. Seven OPEC+ members (Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, Oman) agreed on May 4 to raise June output quotas by 188,000 bpd, the third consecutive monthly increase in line with the prior month's hike. 10 The decision is widely described as largely on paper: with the Strait of Hormuz still closed following the outbreak of the US-Iran war on February 28, 2026, the Gulf producers at the centre of any quota increase — Saudi Arabia, Iraq, Kuwait — cannot physically export incremental barrels. Saudi Arabia's June quota rises to 10.29 million bpd, but its actual March production was reported to OPEC at just 7.76 million bpd.

"The binding constraint is not quotas but the inability to physically move incremental barrels through Hormuz, meaning output policy becomes largely symbolic while exports remain impaired." — Tobias Keller, analyst at UniCredit 11

The group's seven core members meet again on June 7 to decide July output targets.

Reuters poll: Brent average now seen at $90.44 for 2026, up from $63.85 in February. A May 29 Reuters poll of 33 analysts and economists revised 2026 Brent expectations up for the third time since the Iran war began, to $90.44/bbl (from $86.38 last month), and WTI to $84.63 (from $80.07). 11 Since the conflict began, Brent and WTI have hit four-year highs above $126 and $119 respectively. Middle East crude exports, tracked by Kpler, have fallen from roughly 18.3 million bpd pre-crisis to under 8.8 million bpd since March — a cut of more than half.

Analysts polled projected a 2026 supply deficit ranging from 500,000 to 8 million bpd. OPEC's May report forecast demand growth of 1.17 million bpd in 2026, down from its prior estimate of 1.38 million bpd, while the EIA projected demand would contract by roughly 420,000 bpd for the year. Both agencies cite higher prices and weaker macro conditions as demand headwinds, even as supply remains severely constrained.

Canada's oil sands face fresh wildfire risk. As of May 31, wildfire season returned to Canada's oil sands region, adding a secondary supply risk to an already tight market. 12 The situation is being monitored but no material production shut-ins have been reported as of this writing.

Clean energy investment & financing

IEA: global clean energy investment reaches $2.2 trillion in 2026. The World Energy Investment 2026 report underlines that clean energy and electricity infrastructure now attract nearly two-thirds of all global energy spending. 8 Electricity supply and infrastructure investment alone approaches $1.6 trillion; including end-use electrification it climbs to nearly $2 trillion. The report flags the Hormuz disruption as a complicating factor for new deal closings in the near term, particularly in emerging markets where the cost of capital is rising fastest.

Rowan closes $3 billion green financing for 300 MW Texas data center campus. Rowan Digital Infrastructure — backed by Quinbrook and Blackstone — closed nearly $3 billion in debt financing under a green finance framework for its 300 MW Temple, Texas campus on May 28. 13 The transaction is Rowan's largest single financing to date; over the past year, the firm has raised $4.4 billion across three projects under the same green framework. The Temple campus broke ground in early 2026 and is scheduled for operations in 2027. The deal illustrates the growing pipeline of green-labelled infrastructure debt tied to AI-driven data centre demand, a theme the IEA notes explicitly in its 2026 investment report.

Orsted and HASI complete 1 GW solar and battery land deal across three US states. On May 27, Orsted and HA Sustainable Infrastructure Capital (HASI) completed land financing transactions spanning approximately 6,600 acres across Orsted's Eleven Mile Solar Center (Arizona), Sparta Solar (Texas), and Muscle Shoals (Alabama) projects, collectively representing around 1 GW of operational solar and battery capacity. 14 HASI said the deal brought its total land-finance exposure across solar and storage to more than 24 GW after providing 6 GW of similar financing in the past 12 months.

CleanMax raises $575 million for 1 GW of Indian solar and wind. India's CleanMax Enviro Energy Solutions closed approximately $575 million through a multi-lender structure on May 26 to fund 1 GW of new solar and wind projects across Rajasthan and Karnataka. 15 The round underscores India's position as one of the fastest-growing clean energy financing markets globally; the IEA projects total Indian energy investment at a record $170 billion for 2026.

European PPA market pivoting to storage-hybrid contracts. A May 27 analysis from ESS-News found that the European corporate PPA market is shifting toward solar-plus-storage hybrid contracts as price cannibalisation pressure on standalone solar accelerates. 16 Italy plans to launch three FER-X auctions between 2026 and 2027 incorporating up to 26 GW of renewables under regulated hybrid revenue schemes. The structural shift reflects broader dynamics across the continent, where standalone solar revenues are increasingly insufficient to underwrite project finance without a storage co-location component.

Next issue

- SB64 outcomes, June 8–18: Watch for draft decision text on fossil fuel transition workstreams, the Just Transition Mechanism operationalisation, and the first Climate and Trade Dialogue.

- OPEC+ June 7 ministerial: July production targets and whether any Gulf member signals a pathway to restoring Hormuz exports.

- US tax credit deadline, July 4: Q2 2026 clean energy project pipeline data and any OBBA-related legislative adjustments.

- IEA/OPEC monthly reports: June oil market reports due in approximately two weeks.

参考来源

- 1UNEP: UNEP at the June UN Climate Meetings

- 2C2ES: Considerations for the first Climate and Trade Dialogue

- 3Banking Finance: India Announces New Climate Targets for 2035

- 4HCI Nairobi: India's Statement at 173rd CPR Meeting (April 2026)

- 5IISD: Bonn Climate Talks 2026: What to expect after Santa Marta?

- 6reNews: US renewables generation jumps 11%

- 7REGlobal: US BESS Deployments Rise By 32% in Q1 2026

- 8SolarQuarter: IEA Report: Solar Investment to Hit $365B in 2026

- 9E2: Clean Economy Works Q1 2026

- 10Leadership Nigeria: OPEC+ To Raise June Output Quotas By 188,000 Bpd

- 11Reuters: Analysts hike oil forecasts again, energy flows face slow recovery

- 12Reuters: Wildfire season returns to Canada's oil sands

- 13Data Center Dynamics: Rowan closes $3bn green financing for Texas data center campus

- 14reNews: Orsted and HASI close US land finance deal

- 15Reuters: Indian renewable power firm Clean Max raises about $575 million

- 16ESS-News: The European PPA market shifts toward storage

围绕这条内容继续补充观点或上下文。