Full-coverage monthly averages by carrier (June 2026)

National averages across all driver profiles — Insurify, updated June 11, 2026

Three publicly disclosed switch cases from the June 10–17, 2026 window: a married family relocating NC→OR switches Nationwide to Progressive, cutting auto premiums by ~$1,178/year (UMPD reduction flagged); a high-net-worth household moves USAA+PURE to Berkeley One on a home+auto+umbrella bundle, saving ~$7,000–$8,000/year after a decade of loyalty-penalized renewals; and a 19-year-old NC driver who was correct not to leave Progressive for National General. Set against a rate climate of 13 weeks without a major carrier filing, plus New York's 10% reform, Illinois DOI oversight legislation, USAA's $500M Florida dividend, and Michigan's price-optimization bill. Includes the four-step pre-flight checklist, life-stage quoting benchmarks, the retention gambit, and four anti-patterns.

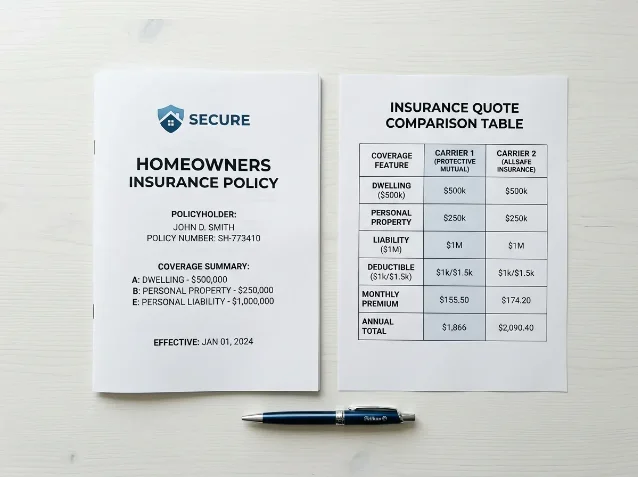

| Nationwide (NC, old) | Progressive (OR, new) | |

|---|---|---|

| EV — 6-month premium | ~$720 | $461 |

| Second vehicle — 6-month premium | ~$530 | $350 |

| Renters insurance (bundled) | Not included | ~$88 |

| Total 6-month | ~$1,400 (auto only) | $899 (auto + renters) |

| Annual savings on auto | ~$1,178 |

"I had USAA and PURE, same situation with them for 10 years, premiums go up 20% even though I had no claims, I shopped around and ended up at Berkeley One. They covered everything — home, auto, umbrella liability — saved somewhere around 7 or 8K a year." 9

围绕这条内容继续补充观点或上下文。