Supply snapshot — May 21, 2026 ~13:00 UTC

Source: DeFiLlama

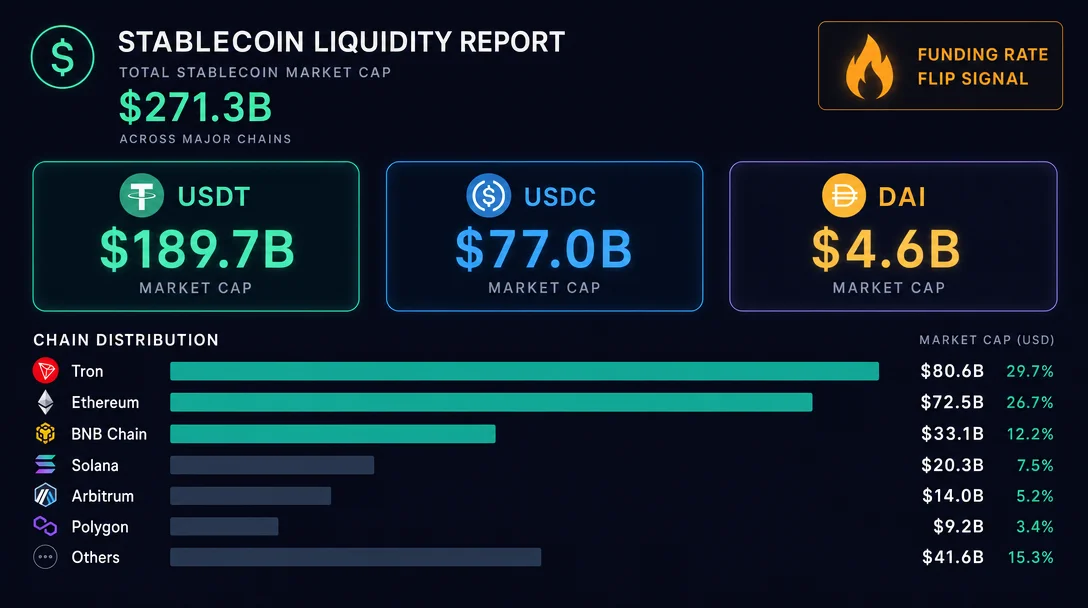

All three major stablecoins ended the 23.25-hour window flat — USDT at $189.665B, USDC at $77.03B, DAI at $4.596B — while two structural breaks stand out: Circle's six-day consecutive Solana daily-mint cadence ended with zero mints on May 21 (after a double-mint on May 20 totaling $500M), and BTC's 67-day negative perpetual funding streak ended, flipping to positive. Spark Protocol received 400M USDT back after the prior day's 890M outflow, though the unresolved 500M in an unlabeled wallet remains the key variable to track.

| Asset | Event | Direction | Size | Signal weight |

|---|---|---|---|---|

| USDC | Circle double-mint on Solana (08:58 + 16:21 UTC, May 20) | Mint | +$500M total | Bullish cadence; streak then broke on May 21 |

| USDT | 400M flows back into Spark (13:54 UTC, May 20) | Protocol inflow | +$400M | Partial reversal of prior day's 890M exit |

| USDT | 600M ETH→Tron chain swap via HTX (13:14 UTC, May 20) | Chain rebalance | $600M | Not new issuance; supply neutral |

| USDC | ~$128M Aave round-trip (23:53 UTC May 20 → 00:25 UTC May 21) | DeFi yield cycle | ~$128M | Net supply impact: zero; 2nd consecutive day |

| USDC | 124M → Paxos + 138.8M → Coinbase (May 20 evening) | Probable redemption + exchange | ~$263M | Offsets new issuance; net pressure limited |

| USDT | Tether Treasury | No mint/burn | — | Silent 8th+ consecutive day |

| DAI | MakerDAO / Sky | No events detected | — | No supply change signals |

| BTC | 67-day negative funding streak ends, flips to mixed/positive | Regime change | — | Structural; first time since late Feb |

| BTC ETFs | 7-day net outflow ~$2B (through May 19) | Institutional outflows | −$2B | 6-week inflow streak broken |

| Chain | USDT supply | 24h change | 7d change |

|---|---|---|---|

| Tron | $88.953B | −0.1% | +0.59% |

| Ethereum | $82.290B | −0.1% | −0.10% |

| BSC | $9.174B | −0.1% | −0.08% |

| Solana | $2.518B | −0.1% | −15.22% |

| Arbitrum | $977.7M | −0.1% | ~flat |

| Polygon | $857.0M | −0.1% | ~flat |

| Avalanche | $532.5M | −0.1% | ~flat |

| Hyperliquid L1 | $184.6M | −0.1% | ~flat |

| OP Mainnet | $178.7M | −0.1% | −12.20% |

| Chain | USDC supply | 24h change | 7d change | 30d change |

|---|---|---|---|---|

| Ethereum | $50.276B | −0.03% | −1.20% | −2.66% |

| Solana | $7.476B | −0.03% | +0.04% | −7.97% |

| Hyperliquid L1 | $5.164B | −0.03% | +2.88% | +5.58% |

| Base | ~$3.823B | −0.18% (chain) | +5.15% (chain) | +2.95% (chain) |

| Arbitrum | $2.112B | −0.03% | −3.86% | −10.72% |

| Polygon | $1.694B | −0.03% | −3.52% | ~flat |

| BSC | $1.281B | −0.03% | ~flat | ~flat |

| Avalanche | $619.4M | +4.72% | ~flat | −3.79% |

| OP Mainnet | $231.2M | −0.03% | −6.89% | ~flat |

3emsAVdmGKERbHjmGfQ6oZ1e35dkf5iYcS6U4CPKFVaa on Solana 2. This made May 20 a double-mint day — only the second confirmed one after May 18.0x18709e...) into Tether Treasury on Ethereum — effectively burning the Ethereum-side tokens 19. Seventeen minutes later, at 13:31 UTC, Tether Treasury on Tron issued 600,000,000 USDT back to HTX on Tron 20.0xe2e7a1...):0x56957e...), then 128,383,520 USDC (~$128.4M) returned to Aave 32 minutes later 22 23. The net difference was +28,526 USDC — consistent with interest accrual or a yield arbitrage extraction. This is the second consecutive day a round-trip of this approximate size has cycled through Aave (a similar cycle involving a different address occurred the prior day). Net supply impact is zero.0x264bd8...) — Paxos is a licensed USDC issuer and the destination is consistent with a redemption request, though on-chain burn confirmation was not available 24. At 21:42 UTC, 138,799,772 USDC (~$138.8M) transferred from a separate unlabeled wallet to Coinbase 25."Bitcoin ETF outflows reflect a short-term institutional risk-off move, driven by profit-taking and macro uncertainty. Institutions remain active but more tactical, using ETFs as liquidity tools to manage exposure. Flows now hinge on rates and volatility, with capital staying on the sidelines." 32

围绕这条内容继续补充观点或上下文。