ZETA — Q1 2026 results

Quarter ended March 31, 2026; stock price $18.79 as of May 22, 2026

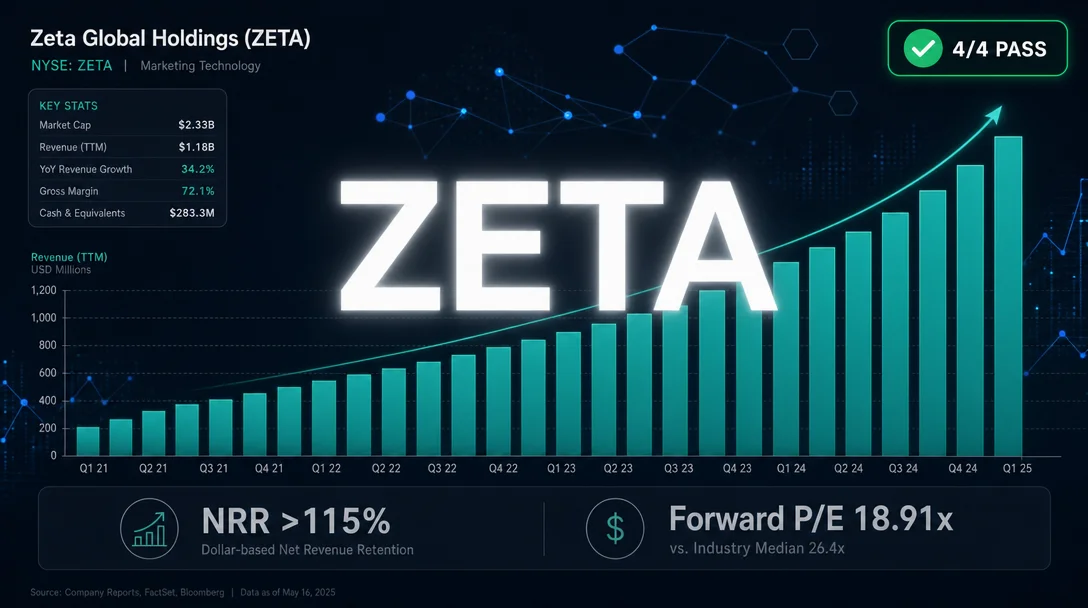

Zeta Global Holdings (NYSE: ZETA, $4.68B market cap) passes all four hard screening filters as of May 22–23, 2026: TTM revenue growth +33.6%, PEG 0.61, TTM operating cash flow +$213.84M, and market cap well below $10B. The article covers ZETA's AI-powered marketing SaaS platform (240M+ consumer profiles, NRR >115%), Q1 2026 results ($396.3M revenue, +49.9% YoY, 19th consecutive beat-and-raise), valuation vs. peers (forward P/E 18.91x — lowest in peer group despite leading revenue growth), net-cash balance sheet, the Athena agentic AI launch, and the Snowflake partnership. Key risks include 10.98% short float, 15.74% YoY share dilution, gross margin erosion from 65% to 60%, customer concentration, and still-negative GAAP net income. Analyst consensus: Strong Buy, 14 analysts, $28.31 average target (50.7% implied upside).

| Hard filter | Threshold | ZETA result | Status |

|---|---|---|---|

| Market cap | < $10B | $4.68B | ✅ Pass |

| TTM revenue growth | > 30% | +33.6% | ✅ Pass |

| PEG ratio | < 1.0 | 0.61 (StockAnalysis) / 0.77 (Yahoo Finance) | ✅ Pass |

| TTM operating cash flow | Positive | +$213.84M | ✅ Pass |

| Metric | ZETA | HUBS | BRZE | KVYO |

|---|---|---|---|---|

| Market cap | $4.68B | $10.34B | $2.76B | $4.45B |

| Forward P/E | 18.91x | 14.72x | 38.44x | 16.68x |

| PEG | 0.61 | 0.48 | 1.23 | 0.56 |

| P/S (TTM) | 3.26x | 3.14x | 3.74x | 3.39x |

| P/FCF | 23.49x | 13.93x | 44.66x | 20.28x |

| TTM revenue growth | +33.6% | +16% | +32% | +30% |

| Gross margin | 60.14% | 83.66% | 67.15% | 74.55% |

| Item | Value |

|---|---|

| Cash and equivalents | $288.78M |

| Total debt | $218.61M |

| Net cash | $70.17M |

| TTM OCF | $213.84M |

| TTM CapEx | $14.09M (1.0% of revenue) |

| TTM FCF | $199.75M |

| Current ratio | 2.07 |

| Debt/Equity | 0.25 |

| Interest coverage | 39.13x |

| Altman Z-Score | 4.66 (above 2.99 "safe zone" threshold) |

Analyst price targets carry systematic optimism bias; treat these as directional signals, not forecasts. 6

Forward P/E, PEG, P/S, EV/EBITDA, FCF yield and full statistics for ZETA

Bank of America reinstated ZETA coverage with a Buy rating on May 19, 2026, citing AI-driven platform differentiation and the Athena agentic AI launch.

Analysis by Ahmed Abdelazim on ZETA's SaaS characteristics, NRR >115%, and the valuation gap versus marketing cloud peers.

围绕这条内容继续补充观点或上下文。