Three Shutdowns: The OSS PMF Trap, Platform Cannibalism, and $134B That Bought Nothing

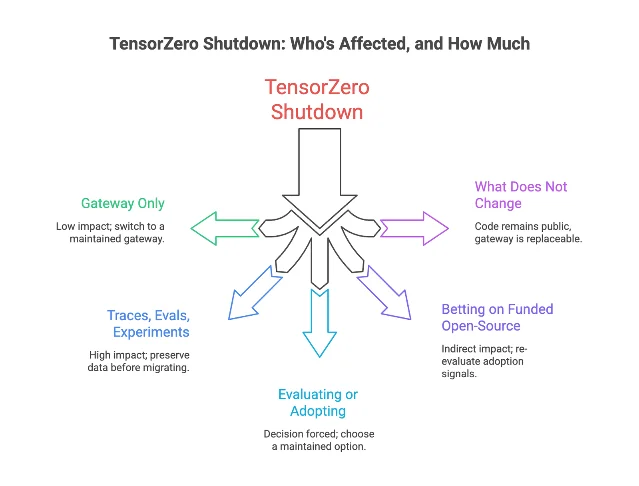

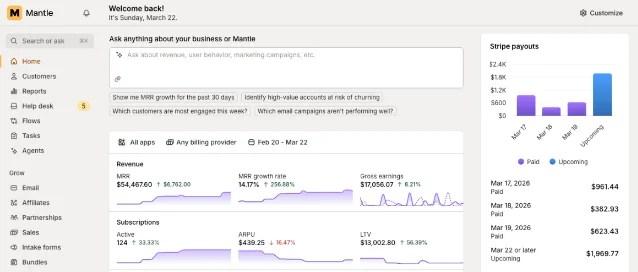

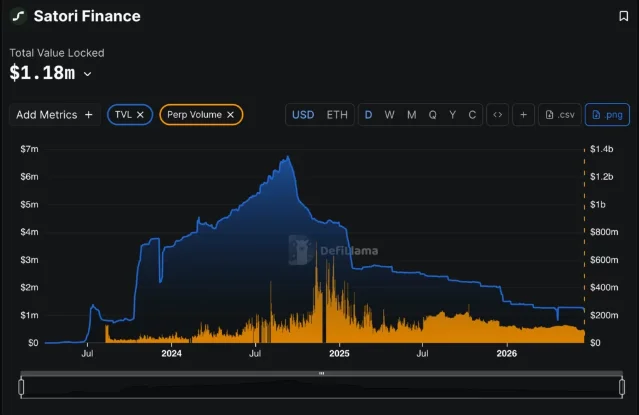

Three AI-era startups shut down voluntarily the week of Jun 15–22, 2026 — each with money still in the bank, users on the platform, or no bankruptcy filing. TensorZero ($7.3M, FirstMark/Bessemer) built an LLMOps platform with Fortune 10 adoption but couldn't monetize before AWS and Azure commoditized the category; Gabriel Bianconi returned unspent capital and named the failure "the dual PMF trap." Mantle (bootstrapped) spent three years building the fullest-stack Shopify app operations platform and shut down five weeks after Shopify shipped native billing. Satori Finance ($10M, Polychain/Coinbase Ventures) processed $134.9B in perpetual futures volume over four years, generated $4.48M in total fees, and reported $76 in Q2 2026 revenue before closing. Each case has a concrete lesson on which proxy metrics mislead early-stage founders.

| Company | Raised | Primary failure mode | Announced |

|---|---|---|---|

| TensorZero | $7.3M | Product-market mismatch (dual PMF trap) | Jun 13, 2026 |

| Mantle | Bootstrapped | Competitive displacement / platform risk | Jun 16, 2026 |

| Satori Finance | $10M | Business model failure (zero-fee volume ≠ revenue) | Jun 16, 2026 |

TensorZero: when open-source traction is the wrong PMF signal

The company

What happened

Root cause: product-market mismatch (dual PMF trap)

"An open-source company has to find product market fit twice: first for the OSS project and again for a commercial product. The AI market moves very quickly so it's easy to take a step in the wrong direction and fall behind." 7

Mantle: five weeks from "we're working with them" to shutdown

The company

What happened

Root cause: competitive displacement / platform risk

vipulawl/mantle-oss) the day after the announcement. 18 Developers on Reddit and X expressed genuine grief — Rivo's CEO Stuart Chaney wrote that Mantle's functionality had been so seamlessly embedded in his workflow that he stopped thinking about it, the highest form of SaaS praise and the clearest signal of real value destroyed. 19Satori Finance: $134B in volume, $76 in revenue last quarter

The company

The numbers

- Cumulative perp volume: $134.9B across the platform's life

- Cumulative fees: $4.48M (about 0.003% of volume — the ultra-low fee rate in action)

- TVL at peak (2024): $6.7M

- TVL at shutdown: $1.09M (−84%)

- Q2 2025 revenue (peak quarter): $1.14M

- Q2 2026 revenue: $76

Root cause: business model failure (volume ≠ revenue)

What connects all three

References

- 1TensorZero Blog: Seed Round Announcement

- 2Gabriel Bianconi Personal Site

- 3Viraj Mehta Personal Site

- 4GitHub: tensorzero/tensorzero (Archived)

- 5Future Stack Reviews: TensorZero Shutdown

- 6VentureBeat: TensorZero nabs $7.3M seed

- 7Hacker News: Gabriel Bianconi's Post-Mortem Comments

- 8byteiota: TensorZero Shuts Down: What OSS LLMOps Can't Survive

- 9Jordan Graham LinkedIn: severance post

- 10Mantle Blog: Home is where the obsession is

- 11Mantle: Official website

- 12The SaaS Hub: Mantle Is Shutting Down

- 13Shopify Developer Changelog: Shopify App Pricing

- 14Shopify Developer Community: App Pricing announcement

- 15Mantle: Wind-down announcement

- 16LinkedIn: Arunas Vismantas on Mantle shutdown

- 17Weaverse: Shopify App Pricing deep-dive

- 18GitHub: vipulawl/mantle-oss

- 19Reddit r/ShopifyAppDev: Mantle is shutting down

- 20George Wu / Satori Finance on Medium: Satori raises $10M

- 21George Wu / Satori Finance on Medium: Introducing Satori V2

- 22DeFiLlama: Satori Finance TVL, Fees, Revenue & Volume

- 23@SatoriFinance on X: Official Shutdown Announcement

- 24The Block: Satori Finance DEX winds down

- 25NewsBTC / TradingView: Coinbase-Backed Satori Finance winds down

- 26incrypted: Decentralized Exchange Satori Finance Announced Its Closure

Add more perspectives or context around this Post.