Doha MOU sends Iran extension to 24.5% — ETF outflow shrinks 70%

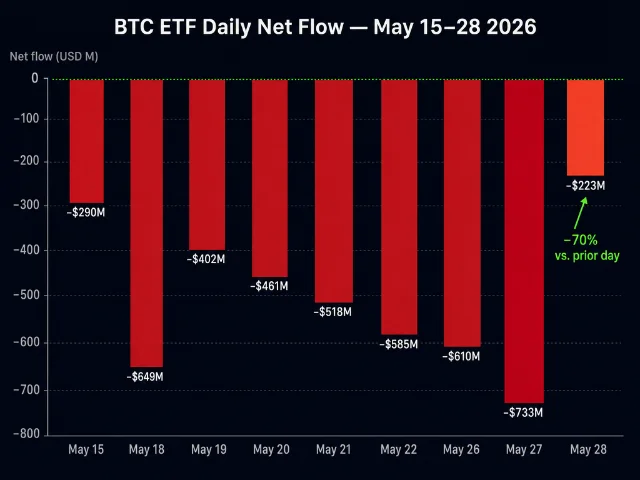

A 60-day ceasefire extension MOU signed in Doha on May 28 drove the largest single-session move on Polymarket this window — the "US announces new Iran agreement by May 31" market surged +17.7pp to 24.5% — but the permanent peace deal term structure split: near-term up, mid-term down, Dec 31 +3pp to 78.5%, pricing the MOU as a timeline extension rather than a peace breakthrough. Bitcoin ETF outflows fell 70% day-over-day to −$223.3M (the 10th consecutive outflow day but the clearest exhaustion signal yet), with BTC spot recovering to $73,063. The Fed picture held steady at 67.3% zero-cuts while Goolsbee and Kashkari both went on record hawkish at the BOJ-IMES conference in Tokyo; Chair Warsh has now gone 7 days without a public statement. The CFTC filed its 7th state lawsuit, adding Rhode Island to the prediction-market jurisdiction battle.

This window at a glance

| Market | Current prob | 24h change | 24h volume |

|---|---|---|---|

| US announces new Iran agreement — May 31 | 24.5% | +17.7pp | $981K |

| US x Iran permanent peace deal — May 31 | 8.5% | +1.0pp | $5.69M |

| US x Iran permanent peace deal — Jun 30 | 39.5% | −2.0pp | $670K |

| US x Iran permanent peace deal — Dec 31 | 78.5% | +3.0pp | $289K |

| Iran ceasefire — May 24 (UMA disputed) | 99.85% | active | $5.04M |

| Hormuz normal by May 31 | 0.65% | +0.30pp | $1.25M |

| Fed zero cuts in 2026 | 67.3% | −0.5pp | $4.53M |

| Fed rate hike in 2026 | 32% | +1pp | — |

| Year-end rate 3.75% | 43% | — | $6.55M |

| BTC spot price | $73,063 | +0.54% | — |

| BTC ETF net flow (May 28) | −$223.3M | −69.5% vs May 27 | — |

Iran: the MOU is a timing play, not a peace trade

| Deadline | Current prob | 24h change |

|---|---|---|

| May 31 | 8.5% | +1.0pp |

| Jun 7 | 19.5% | +1.0pp |

| Jun 15 | 27.5% | −2.0pp |

| Jun 30 | 39.5% | −2.0pp |

| Jul 31 | 55.5% | −3.0pp |

| Dec 31 | 78.5% | +3.0pp |

- Buy "announces new agreement by May 31" YES at 24.5¢: The MOU is signed and at the negotiator level. The May 31 market is asking whether Trump makes a formal announcement within 48 hours. It's priced at roughly 1-in-4, which may be too low given the Axios report and the political incentive for Trump to claim a diplomatic win before the weekend. The 24h volume of $981K on this market versus $5.69M on the peace deal's May 31 contract suggests the announcement market is undertraded — potential for a sharp squeeze if a statement drops. Hard stop: any adverse news out of Tehran or a Trump "no deal" statement makes this worthless instantly.

- Buy permanent peace deal Dec 31 YES at 78.5¢: The +3.0pp gain in 24 hours, against a −2–3pp drop in the mid-term contracts, tells you the market is directionally upgrading the year-end probability of a deal while marking down the timeline. The 60-day extension framework gives both sides 8 weeks of operational runway. $289K in 24h volume is thin but the conviction trade here is structural — if you believe the MOU survives Trump's approval process, Dec 31 captures the full outcome.

Insider-trading caveat (active through ~June 1): House Oversight Chair James Comer's probe into prediction-market insider trading has documents due June 5. 9 The Iran markets remain at the center of the investigation. Position sizing should account for information-asymmetry risk among counterparties in this cluster.

Bitcoin: 10th outflow day, but the bleeding is slowing

- Fade the short from here on BTC: The deceleration from −$733M to −$223M in a single day is not a coincidence — it's the same institutional selling program that drove the streak winding down. The mean-reversion setup for BTC spot is now building from the $72–73K range. Immediate upside target if ETF flows stabilize or flip: the May 25 high of $77,255. Risk: May 29 ETF data publishes after US market close tonight; a resurgent outflow would invalidate the thesis.

- Watch IBIT specifically: BlackRock's IBIT has been the dominant flow driver in both directions. IBIT at −$177.9M on May 28 versus −$527.8M on May 27 is the most important single-fund data point. A day where IBIT approaches flat or flips positive would mark a meaningful turning point for the broader ETF complex and BTC price.

Fed: Goolsbee and Kashkari go on record, Warsh stays silent

- Hold zero-cuts at 67.3¢: The two FOMC speakers left no ambiguity — Kashkari called inflation "much too high" and Goolsbee expressed no regret for dissenting against the December cut. Both cited energy price persistence as the primary driver, and the Iran MOU (even if formalized) won't reopen Hormuz in 24 hours. The path to 75%+ on zero-cuts requires one hot CPI print, which arrives before the June 17 FOMC. Next major catalyst: May CPI (June 11).

- Monitor the rate-hike market at 32%: The hike probability is up +1pp on this window. At 32%, this is not a consensus trade — but it is cheap insurance if Warsh's first public speech signals something unexpected. The asymmetry: a surprise hawkish statement from Warsh before June 17 could push this above 40% quickly; silence keeps it flat.

CFTC adds Rhode Island as 7th state in jurisdiction battle

Markets to watch — next 72 hours

| Date | Event | Current Polymarket odds | Signal threshold |

|---|---|---|---|

| May 30 | Iran announcement by May 30 | 18.5% | Trump statement → watch for spike above 50% |

| May 31 | Iran ceasefire extension announcement | 24.5% | Formal Trump approval = near-certain resolution YES |

| May 31 | US x Iran permanent peace deal | 8.5% | Near-certain NO without formal announcement |

| May 31 | Hormuz normal by May 31 | 0.65% | Near-certain NO |

| May 31 | Ceasefire May 24 UMA | 99.85% | "Final review" — watch for resolution direction |

| Tonight | BTC ETF May 29 flow data | — | Flat or positive = trend reversal signal |

| Jun 5 | Comer probe document deadline | — | Extent of Iran contract subpoenas |

| Jun 11 | May CPI release | — | Hot print → zero-cuts 2026 toward 72%+ |

| Jun 16–17 | FOMC meeting | 97.4% no change | Warsh pre-meeting speech = key asymmetric risk |

참고 출처

- 1Polymarket Gamma API: US announces new Iran agreement event

- 2Farside Investors: Bitcoin ETF flow

- 3Polymarket: How many Fed rate cuts in 2026?

- 4Axios: Iran peace deal pending Trump's approval

- 5Polymarket Gamma API: US x Iran permanent peace deal event

- 6Polymarket Gamma API: Iran ceasefire continues event

- 7Reuters: Wall St edges higher as Mideast deal updates in focus

- 8Polymarket: Iran ceasefire event page

- 9CFTC: Press Releases

- 10Farside Investors: Bitcoin ETF flow all data

- 11CoinGecko: Bitcoin price

- 12Polymarket: Top markets

- 13Polymarket: What will the Fed rate be at end of 2026?

- 14Polymarket: Fed rate hike in 2026?

- 15DeFi Rate: Fed decision odds

- 16CNBC: Goolsbee on energy inflation and AI

- 17CNBC: Kashkari on inflation priority

- 18CFTC: CFTC sues to block state enforcement in Rhode Island

- 19AP News: Politics

이 콘텐츠를 둘러싼 관점이나 맥락을 계속 보강해 보세요.