June 11 in business history: FM suppressed, China reopened, North Sea oil split, Compaq's $9.6B mistake

On June 11, four decades of business history converge: Edwin Armstrong demonstrates FM radio to the FCC in 1936 only to have RCA spend two decades killing it through regulatory capture; Nixon lifts a 21-year China trade embargo in 1971 for purely geopolitical reasons that compound into $500B+ in annual bilateral trade; the first North Sea oil flows from the Argyll field in 1975, setting the stage for a governance fork that leaves Norway with a $2 trillion sovereign fund and the UK with nothing equivalent; and Compaq's shareholders approve the $9.6B DEC acquisition in 1998, the largest tech deal of its time, that collapses within four years.

Four events across 62 years — one inventor's tragedy, one geopolitical masterstroke, one resource governance fork in the road, and one M&A case study that every board still reads. The common thread: the announcement date rarely determines the outcome. What happened after is where the lesson lives.

1936 — Edwin Armstrong demonstrates FM radio, and RCA buries it

In mid-June 1936, Edwin Armstrong gave a demonstration of his wideband FM radio system at the Federal Communications Commission in Washington before roughly 500 radio engineers. He played a jazz record first on AM — static-filled, as AM always was — then switched to FM. A United Press correspondent reported that "if the audience of 500 engineers had shut their eyes they would have believed the jazz band was in the same room. There were no extraneous sounds." 1

The technology was unambiguously superior. Armstrong had spent more than two decades building it. He had already invented the regenerative circuit (1912), the superheterodyne receiver (1918) — still the architecture inside virtually every radio and phone receiver today — and the super-regenerative circuit (1922), which RCA bought from him for $200,000 plus stock, making Armstrong RCA's largest private shareholder at the time. 2

David Sarnoff, RCA's chief, had been Armstrong's friend since 1913. Armstrong had even married Sarnoff's secretary. But when Armstrong brought FM to Sarnoff, expecting enthusiasm, he got obstruction. RCA's entire business model rested on AM radio and the NBC network. FM would require scrapping billions of dollars in transmitters and receivers. Sarnoff had expected "an evolution in the AM system that would reduce static" — what he got was a revolution, and he spent the next decade trying to kill it.

RCA orchestrated a decisive blow at the FCC: in June 1945, the commission moved the FM band from 42–50 MHz to 88–108 MHz, rendering 395,000 existing FM receivers obsolete overnight. Armstrong believed — and subsequent historians largely agree — that RCA and its allies engineered the band shift specifically to disrupt FM's momentum. 3

Armstrong filed patent infringement suits against RCA in 1948. RCA deployed lawyers who dragged out discovery for years — interrogating Armstrong about his income taxes and why he used Columbia University letterhead. His patents expired in 1950. His fortune was consumed by legal fees. By late 1953, Armstrong told his wife Marion he had used up nearly all his financial resources. She declined to release their retirement savings to continue the litigation. Armstrong struck her with a fireplace poker in a rage; she left and never saw him again. On the night of January 31–February 1, 1954, he stepped out of the window of his 13th-floor Manhattan apartment. His note ended: "God keep you and Lord have mercy on my Soul." 1

He died believing he had failed.

His widow Marion pursued the remaining 21 patent cases. By 1967, she had won every significant one, collecting roughly $10 million in total settlements. RCA paid $1 million in late 1954. The National Park Service confirmed: "all of the suits were decided in Armstrong's favor." 4 By 1980, FM accounted for half of all US radio listeners. Today it dominates the medium AM once owned.

The mirror: When a superior technology threatens an incumbent's installed base, expect regulatory capture, not just market competition. Armstrong was technically right for 18 years before the law caught up. The question for any innovator facing entrenched resistance is whether they have the capital — and the temperament — to outlast it. Armstrong had neither. Marion did.

1971 — Nixon ends 21 years of US trade embargo on China

On June 10, 1971, President Nixon ended the trade embargo on the People's Republic of China, in effect since the Korean War. White House Press Secretary Ronald Ziegler announced that 47 categories of non-strategic goods were authorized for export under general license, and all restrictions on Chinese imports were lifted. The New York Times ran the story on its front page on June 11. 5

The economics were, at that moment, nearly irrelevant. US officials privately conceded that the relaxation would "probably do little to increase United States exports" in the short term. 5 Chinese imports to the US were projected to reach perhaps $100–200 million within a few years — mainly hog bristles, tungsten, ceramics, and textiles. Pre-embargo annual bilateral trade had been roughly $200 million. The logic was entirely geopolitical: Kissinger's strategy was to "play China against the Soviet Union, the Soviet Union against China, and both against North Vietnam," per a Miller Center assessment. 6

One month after the trade opening, Kissinger made a secret trip to Beijing via Pakistan to meet Premier Zhou Enlai. Nixon then announced publicly in July 1971 that he would visit China — "a journey for peace, peace not just for our generation but for future generations on this earth we share together." 7 He arrived in Beijing on February 21, 1972, the first sitting US president to set foot in mainland China. The Shanghai Communiqué followed on February 27.

Full diplomatic recognition came under Carter in 1979. China joined the WTO in 2001. Bilateral trade eventually exceeded $500 billion annually — roughly 2,500 times what US officials had projected in 1971 as a "few years" upside. 8

The mirror: Nixon's trade opening was not a trade policy — it was a geopolitical instrument whose economic consequences compounded over 50 years in ways no one in the room anticipated. The decision to lift the embargo was made with essentially zero short-term economic case, purely on strategic grounds. The practitioners who tend to find this mirror most useful are those facing a major market entry or partnership decision where the near-term numbers don't pencil out but the long-term structural position does. The constraint, then and now: those long bets require political cover that most executives don't have for more than one cycle.

1975 — The first North Sea oil flows, and two neighbors make opposite choices

On June 11, 1975, crude oil began flowing from the Argyll field in the central North Sea — UK Blocks 30/24 and 30/25, roughly 310 kilometers east-southeast of Aberdeen. The operator was Hamilton Brothers Oil of Denver, with Texaco holding 24% and RTZ Oil & Gas 25%. The Transworld 58, a converted semi-submersible drilling rig, produced at a design throughput of 25,000 barrels per day. 9 A week later, UK Energy Secretary Tony Benn ceremonially opened the valve at BP's Isle of Grain refinery, telling the crowd: "This really is in its own way exactly as significant as the first run of Stephenson's Rocket... It is a turning point." 10

He was right about the turning point. He was wrong about where it would turn.

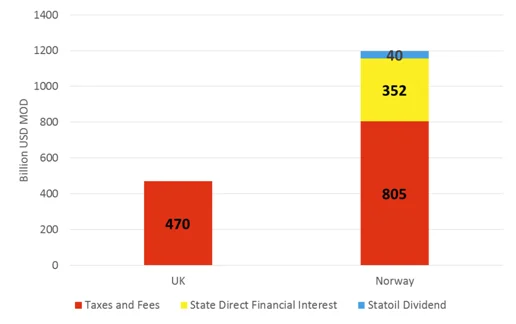

Norway's Ekofisk field had come online slightly earlier. Both the UK and Norway produced comparable volumes over the following decades — the UK extracted approximately 42.8 billion barrels of oil equivalent, Norway around 40 billion. But the fiscal outcomes were radically different. UK government revenues totaled roughly $470 billion in real 2014 dollars. Norway's came to $1,197 billion — more than double, on nearly identical production. 11

The gap traces to three specific policy differences. Norway retained majority state ownership through Statoil (now Equinor) and the State Direct Financial Interest (SDFI), holding controlling stakes in 11 of its 14 billion-barrel fields. The UK privatized: BP was fully divested by 1987, the British National Oil Corporation was sold in 1982, and Enterprise Oil spun off in 1983 — generating roughly £1.2 billion in receipts that a 1980 Cabinet Office review had already warned would prove poor value against the long-term revenue stream being surrendered. 11 Norway also maintained higher and more stable tax rates; the UK's effective rate on North Sea profits fell from around 50% in the early 1980s to roughly 10% by the early 1990s. And Norway established a sovereign wealth fund in 1990 to invest surplus revenues offshore, insulating the domestic economy. By May 2026, that fund held approximately $2.049 trillion — roughly $390,000 per Norwegian citizen, the largest sovereign wealth fund on earth. 12

PwC's then-chief economist John Hawksworth estimated in 2014 that the UK could have had a £400 billion sovereign fund had it followed the Norwegian model. Sukhdev Johal of Queen Mary University put the missed opportunity at £850 billion — roughly £13,000 per person, or 33% of UK national debt at the time. 11 By March 2026, approximately 90% of UK North Sea reserves had already been extracted.

The mirror: The UK and Norway made the same discovery on roughly the same day from the same geological formation. Fifty years later, Norway has a $2 trillion fund; the UK has the receipts from a privatization exercise. Resource governance decisions made in the 1980s — about ownership structure, tax rates, and whether to save or spend — compounded quietly until the scoreboard became undeniable. For any organization sitting on a one-time windfall today — an asset sale, a patent royalty stream, a market position that won't last forever — the Norway/UK fork is the cleanest available model of what the choice looks like in retrospect.

1998 — Compaq's shareholders approve the DEC acquisition. The integration was already failing.

On June 11, 1998, Digital Equipment Corporation shareholders voted to approve Compaq's acquisition at a special meeting. The deal formally closed the following day, June 12. Compaq had announced the transaction on January 26, 1998, at $9.6 billion — $30 cash plus 0.945 Compaq shares per DEC share, a 33% premium over DEC's prior close of $45.75. At announcement, this was the largest acquisition in computer industry history. 13 14

Compaq CEO Eckhard Pfeiffer had a coherent strategic thesis: DEC brought a $6.5 billion services business, enterprise client relationships, and the Alpha processor — assets that would transform Compaq from a PC manufacturer into a full-spectrum computing company capable of challenging IBM. "The combined revenues of the two companies for 1997 was $37.5 billion," Pfeiffer said. "That makes us the No. 2 computing company." 13

The thesis was plausible. The execution was not.

Compaq hired three separate consulting firms to manage the integration and produced no coherent plan. DEC was an engineering-first culture; Compaq was a volume-oriented PC shop. Pfeiffer never articulated a unified product roadmap for the combined entity. While Compaq was distracted by the merger, Dell seized significant PC market share. Dell surpassed Compaq as the world's number-one PC maker in 1999, and again in 2001. 15

Ten months after the deal closed — on April 18, 1999 — Compaq's board forced Pfeiffer out. Chairman Benjamin Rosen, who had also engineered the ouster of Compaq co-founder Rod Canion in 1991, cited execution failures. The Q1 1999 profit warning that triggered the board's move showed earnings roughly half of Wall Street's $540 million consensus. Compaq's stock had fallen from $51.25 in January 1999 to $23.625 by the Friday before Pfeiffer left — a 54% decline in three months. 16

Compaq CFO Jeff Clarke — himself a former DEC executive — later admitted the three things Compaq failed to do: define clear product roadmaps before closing, build an organizational structure without too many political compromises, and establish financial accountability for the combined entity. "When Compaq bought DEC," Clarke said in 2002, "the company was not clear enough on several key pillars of a successful integration." 17

By September 2001, HP announced it would acquire Compaq for approximately $25 billion in stock. Compaq had accumulated $1.7 billion in short-term debt and market observers believed it could not survive independently for another year. The deal closed in May 2002. The DEC brand, along with Compaq's, was retired. 18

The trajectory: DEC shareholders voted June 11, 1998. The CEO was gone by April 1999. The acquirer was acquired by May 2002. Four years and one month from vote to disappearance.

Harvard Business School turned the DEC acquisition into a case study (HBS Case 800-199) used to teach M&A failure. The key variable Clarke identified — "clear enough on several key pillars" — is banal in retrospect. At the time, under price pressure and competitive anxiety, each compromised decision seemed individually defensible.

The mirror: Compaq entered the shareholder vote on June 11 with a sound strategic thesis and no integration plan. The $9.6 billion paid for the assets; the integration plan was supposed to capture the value. It never materialized. For any executive approaching a transformative acquisition today: the board vote is not the hard part. The 90 days after closing — product roadmap, org structure, financial accountability — determine whether the thesis survives contact with reality.

Cover image: The New York Times, June 11, 1971 front page — Wikipedia / public domain

参考ソース

- 1Wikipedia: Edwin Howard Armstrong

- 2Columbia Magazine: Edwin Armstrong, Pioneer of the Airwaves

- 3DamnInteresting: The Tragic Birth of FM Radio

- 4National Park Service: Edwin H. Armstrong House

- 5New York Times: President Ends 21-Year Embargo on Peking Trade

- 6Miller Center, University of Virginia: Nixon on China

- 7Wikipedia: 1972 visit by Richard Nixon to China

- 8EBSCO Research Starters: Nixon Opens Trade with China

- 9Wikipedia: Argyll oil field

- 10The Guardian: The first North Sea oil is pumped ashore in Britain, 1975

- 11Natural Resource Governance Institute: Did the UK miss out on £400 billion worth of oil revenue?

- 12Norges Bank Investment Management: The fund's value

- 13CNET: Compaq to buy Digital for $9.6 billion

- 14New York Times: Compaq to Buy Digital Equipment for $9.6 Billion

- 15Wikipedia: Compaq

- 16New York Times: Compaq Computer Ousts Chief Executive

- 17CRN: Compaq: We Learned Our Merger Lesson With DEC

- 18Stanford GSB: Compaq and HP — Ultimately, the Urge to Merge Was Right

このコンテンツについて、さらに観点や背景を補足しましょう。