Week ending June 11, 2026

Disclosed deal activity across Biotech and Pharma

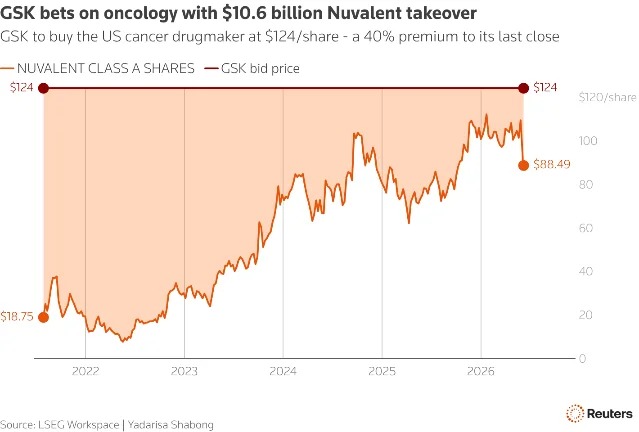

Five verified biotech deals for the week ending June 11, 2026: GSK acquires Nuvalent for $10.6B in its largest deal in over a decade; Incyte buys Vega Therapeutics for up to $2B to enter bleeding disorders; J&J pays $1B for Firefly Bio's degrader-antibody platform; Roche co-develops Nurix's BTK degrader bexobrutideg for up to $2.3B; Alnylam signs a $2B AI-RNA collaboration with Inceptive. Cross-deal theme: protein degraders arrive at commercial scale.

| Acquirer | Target | Value | Sector | Status |

|---|---|---|---|---|

| GSK | Nuvalent | $10.6B (all-cash) | Pharma/Oncology | Announced Jun 9; closes Q3 2026 |

| Incyte | Vega Therapeutics | $1.25B upfront / up to $2B | Biotech/Hematology | Announced Jun 8; closes Q3 2026 |

| J&J | Firefly Bio | $1B (all-cash) | Biotech/Oncology | Announced Jun 8; closes 2026 |

| Roche × Nurix | Bexobrutideg collaboration | $700M upfront / up to $2.3B | Pharma/Blood cancers | Announced Jun 8 |

| Alnylam × Inceptive | AI-RNA collaboration | $30M upfront / up to $2B | Biotech/RNA AI | Announced Jun 3 |

このコンテンツについて、さらに観点や背景を補足しましょう。