Burry: FISV's CEO exit is a thesis violation — not a sell signal

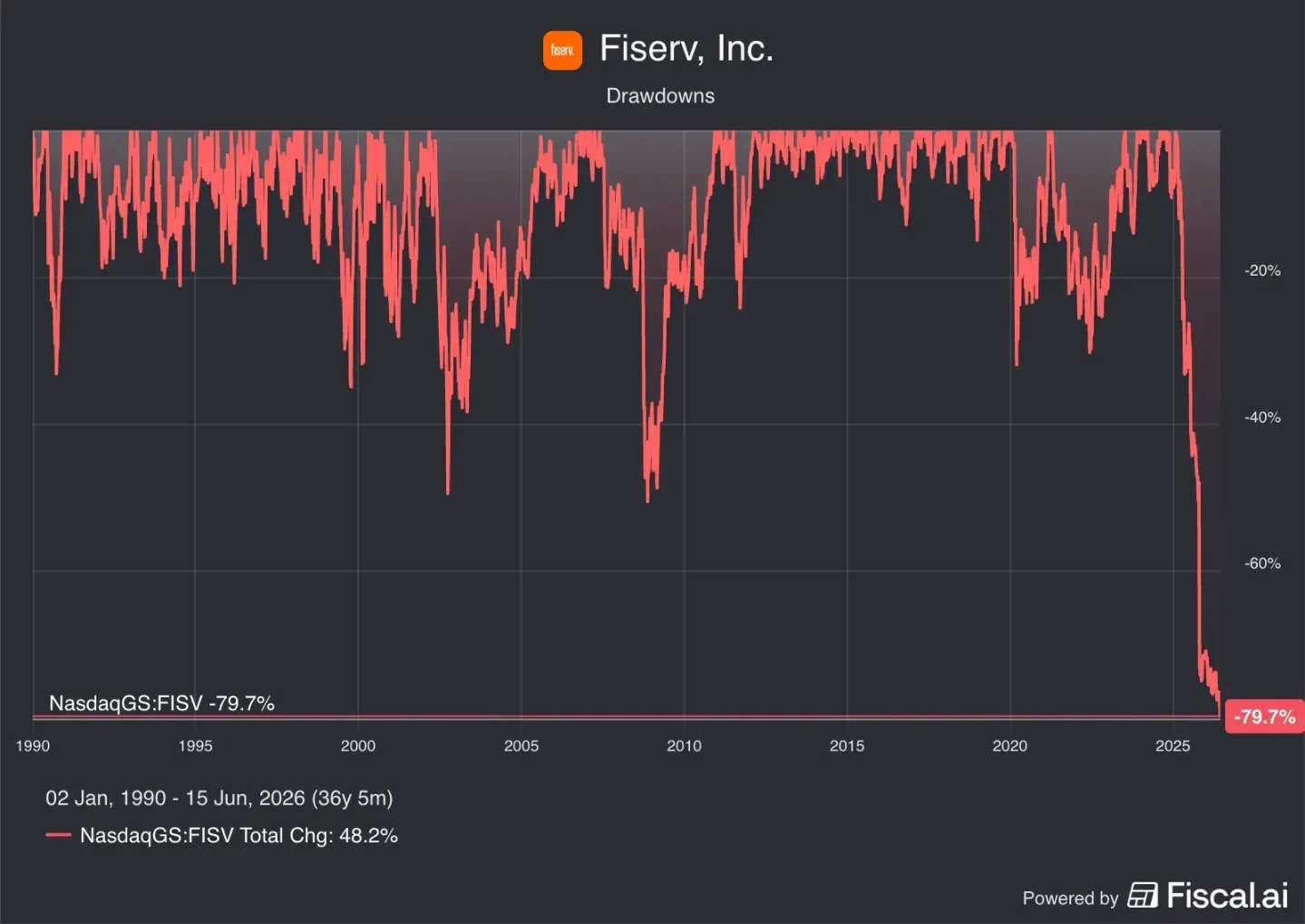

Michael Burry published a detailed bull case for Fiserv (FISV) on June 15 after the stock fell another 11% on CEO Mike Lyons's surprise departure. Rather than selling, Burry bought more at ~$48.50 — his third CEO in as many years — arguing the 79% collapse from $226 reflects governance panic, not a broken business. His scenario table shows even the bear case implies meaningful upside from current prices.

Michael Burry, founder of Scion Asset Management (the fund immortalized in The Big Short for its 2007 mortgage-short), published a detailed bull case for Fiserv (FISV) on June 15 after the stock dropped another 11% on news that CEO Mike Lyons had resigned to take the top job at Truist Financial. Burry bought more shares the same day. 1

"Talk about a dog of a stock, now under $48 from $226 early last year." 1

That $226 → $48 move — a 79% decline — happened while the S&P 500 was in one of its strongest bull runs in decades. Burry called it a ten-year low in price. The drawdown puts Fiserv in the same ballpark as dot-com casualties, except the underlying business never actually broke.

"Thesis violation does not mean sell"

The framing of the Trading Post is the interesting part. Burry explicitly labeled Lyons's departure a thesis violation — his term for an event that cuts against a core assumption of the original investment thesis. Most investors treat a thesis violation as a stop-loss trigger. Burry treats it differently.

"The CEO left unexpectedly, which is a thesis violation if there ever was one. Thesis violation does not mean sell. It means re-evaluate." 1

His re-evaluation produced three conclusions. First, Lyons's job was to clean up the mess left by his predecessor Frank Bisignano — specifically, what Burry described as "aggressive accounting and short-term sales tricks." When Lyons spoke publicly about those problems, the stock cratered. But the telling of the story is not the story itself. Second, Lyons spent 13 months at Fiserv and the business ran fine during his tenure. His departure, Burry argued, probably says more about the appeal of the Truist CEO role than about any hidden rot at Fiserv. Third — and most pointed:

"To be clear, the business itself runs just fine no matter who is CEO." 1

He added that Fiserv's operations are too large and too automated to be switched on or off by any single executive.

What Fiserv actually is

Part of what makes this an interesting case for retail investors is the mismatch between how the stock has traded and what the company does. Fiserv is the largest financial technology infrastructure company in the United States: it processes 10,000 transactions per second, serves 1.8 billion card-issuing accounts, covers 339 million deposit and loan accounts, and reaches 95% of U.S. households. 1 2 Its core banking processing business has a 99% customer retention rate — a metric Burry described as "practically a license to print money." For the third consecutive year it ranked first in the IDC FinTech 100. 2

The consumer-facing Clover merchant network — 900,000 merchants across 3.9 million small businesses — competes directly with Block, Toast, Stripe, Shift4, and Adyen. Clover's edge, in Burry's view, is that it runs on top of Fiserv's existing bank and credit-union relationships rather than having to build distribution from scratch. The new CEO, Takis Georgakopoulos (56), ran Clover and the broader Merchant Solutions and Technology division before this appointment. He previously spent 17 years at JPMorgan Chase, where his last role was Global Head of Payments, and was a partner at McKinsey before that. 1

"The new CEO seems to have technology expertise in payments that the old one did not." 1

Burry noted Georgakopoulos is an internal hire but not a creature of the old guard — someone who grew the company's fastest business and came in through the competitive meritocracy of JPMorgan payments, not through legacy Fiserv politics.

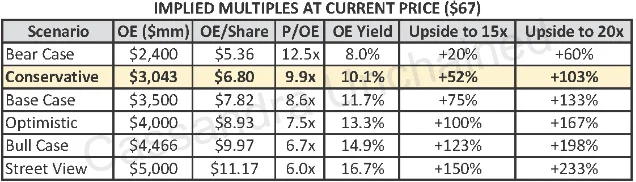

The valuation table

Burry included what he calls a "bingo sheet" — a scenario table mapping different operating earnings assumptions to implied multiples at a price of roughly $67 when the post was written (the stock has since traded lower). Even the bear-case row, which assumes operating earnings of $2.4 billion, implies only 12.5x P/OE at that price, with an operating earnings yield of 8%.

At the conservative case ($3.04 billion OE), 15x operating earnings implies a price roughly 52% above current levels; 20x implies roughly 103% upside. The street consensus scenario ($5 billion OE at 6x P/OE) implies 233% upside to 20x. Burry did not specify a price target — he gave the framework and left the conclusion to the reader.

"In something like this, buying very cheap is important." 1

He also flagged an emerging technical signal: trading volume in FISV has been running above its 50-day average for several months, a pattern he reads as a possible early stage of base-building. He counted eight gap-downs of more than 3% and three of more than 10% in the past 18 months — the kind of distribution that can precede a durable bottom. 1

The broader market backdrop

About 2.5 hours before the Trading Post went up, Burry posted a 10-word message on X: "It has been ridiculous for a very very long time." 3 The tweet collected 500,000 views, 4,093 likes, and 452 replies with no hashtag, no link, and no specified target. It arrived on the same day SpaceX's stock (SPCX) extended its post-IPO gains to a 19.6% single-day move, adding to a $750 billion market cap from its June 13 debut. 4

Burry did not clarify whether the tweet referred to the AI trade, SpaceX's valuation, FISV's own collapse, or all three. He has previously described the semiconductor sector as a dot-com-era repeat, shorted Nvidia and Palantir, and in earlier posts this year warned that 87% of venture capital flowing to AI exceeds the concentration seen at the 1999 peak. The Trading Post itself contains a line that works in any of those directions: "This is a resilient business that has stumbled badly after years of catering to what Wall Street wants to see more than what was really fundamentally good for the business long-term." 1

コンテンツカードを読み込んでいます…

Why this matters

Burry disclosed he bought more FISV on June 15 at approximately $48.50 per share, bringing his position to roughly 5–7% of his portfolio — comparable in size to his MercadoLibre and Birkenstock holdings. 2 He was explicit that FISV "will not soon romance the growth crowd" — meaning the catalyst for re-rating isn't near-term earnings acceleration but a multiple normalization from what he regards as governance-panic pricing. 1

For investors watching this position: Jana Partners is reportedly pushing Fiserv to sell assets and restructure the board, adding activist pressure that could accelerate or complicate any recovery timeline. 5 The full Trading Post is behind a paywall at Cassandra Unchained on Substack; the public teaser tweet can be read at the link above.

参考ソース

- 1Michael Burry — Trading Post June 15, 2026

- 2MENAFN — Michael Burry Stays Bullish On FISV Stock Despite 'Thesis Violation' Triggered By CEO Exit

- 3X/@michaeljburry — "It has been ridiculous for a very very long time"

- 4Benzinga — Michael Burry Makes An Observation As Investors Embrace AI And SpaceX

- 5Stocktwits — Michael Burry Stays Bullish On FISV Stock Despite 'Thesis Violation' Triggered By CEO Exit

このコンテンツについて、さらに観点や背景を補足しましょう。