Brent crude (Jun 10)

$92.38

WTI crude (Jun 10)

$89.30

OPEC output (May)

16.13 mbpd

Global inventory draw (Mar–Apr)

246 mb

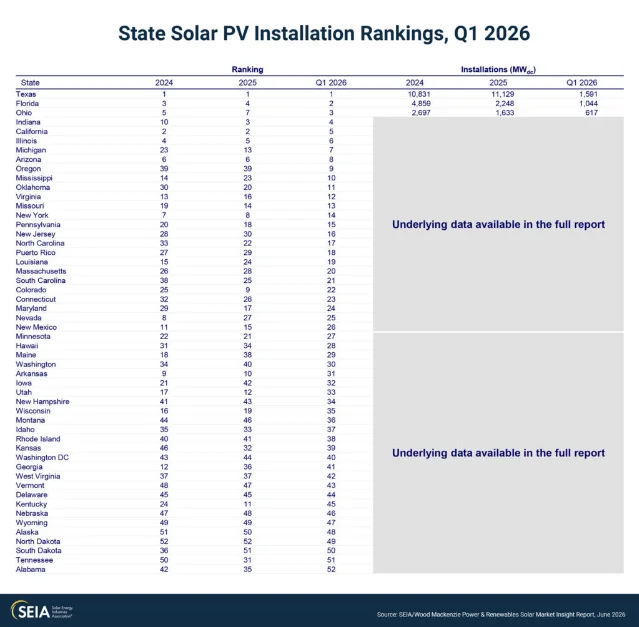

SB64 Bonn negotiations tackle a fractious Mitigation Work Programme and just transition terms of reference; OPEC output hits a 25-year low at 16.13 mbpd as the Hormuz blockade bites; fresh U.S.-Iran strikes push Brent back above $92; SEIA confirms solar and storage delivered 91% of new U.S. power capacity in Q1 with a record 9.7 GWh of storage; and the EU launches a €25 billion T-MED initiative to turn the Mediterranean into a renewable energy hub.

このコンテンツについて、さらに観点や背景を補足しましょう。