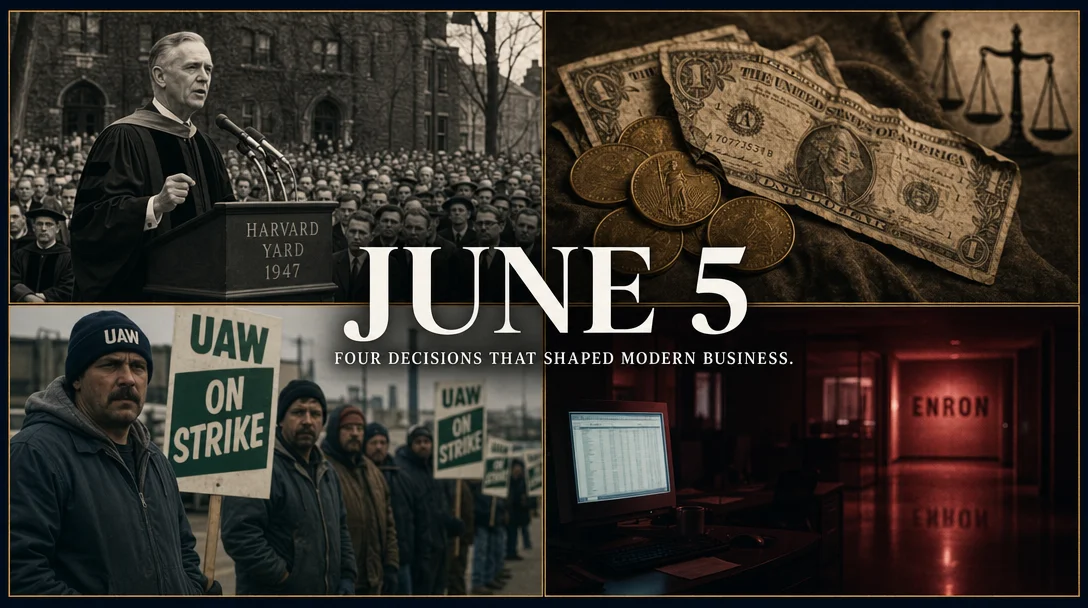

June 5: Four decisions that shaped business

On June 5 across four decades, four landmark events each crystallized a decision problem still relevant today: Marshall's 12-minute Harvard speech launched a $13.3B European recovery program whose real impact was political ownership rather than capital size (1947); Congress voided all gold clauses in U.S. contracts and the Supreme Court called it unconstitutional while still denying relief (1933); GM's secret removal of stamping dies from its Flint Metal Center triggered a 54-day strike that shut 27 plants and cost $12B (1998); and Jeff Skilling declared Enron "on the side of angels" on national television six months before its collapse (2001).

What do a 12-minute commencement speech, a congressional sleight of hand, a secret equipment theft, and a TV interview have in common? All four happened on June 5 — in 1947, 1933, 1998, and 2001 respectively — and each one crystallized a decision problem that business professionals still face today.

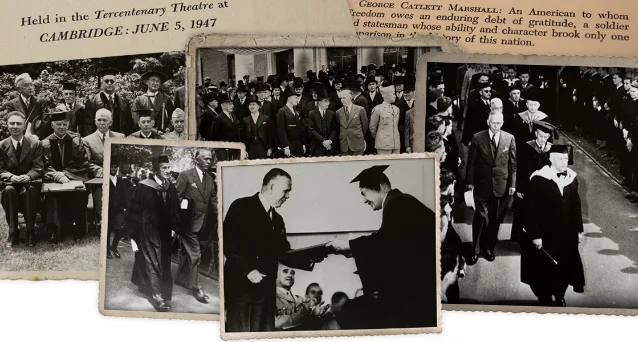

The 12-minute speech that built the modern world (1947)

On June 5, 1947, at 2:50 PM, U.S. Secretary of State George C. Marshall delivered a roughly 12-minute address at the 296th Harvard Commencement before approximately 15,000 people in Harvard Yard. 1 The State Department had told reporters it was "a routine commencement speech … nothing of any importance." Truman scheduled a competing press conference to divert domestic headlines. The real audience was Europe — and the BBC.

Marshall made no dollar pledges. He offered only a framework: the United States would support any European recovery program, but the initiative must come from Europe. 1 That structural choice — insisting on European ownership rather than imposing an American plan — turned out to be the design decision that made everything else work.

Between 1948 and 1952, the program transferred $13.3 billion to 17 Western European nations — roughly $137 billion in 2025 dollars. 3 By 1951, output across all recipient countries was at least 35% above 1938 levels; Western Europe's aggregate industrial production rose 40%. 3

Here's what economic historians discovered later: that $13.3 billion amounted to less than 3% of recipient nations' combined national incomes. DeLong and Eichengreen concluded in 1991 that the direct investment channel alone would have left European GDP only about 2% higher — nowhere near enough to explain the economic miracle. 4 The Plan's real impact was political and institutional: it broke postwar distributional deadlocks, forced market liberalization through conditionality, and prevented what DeLong and Eichengreen called an "Argentine trajectory" — wartime controls retained, distributional conflicts unresolved, persistent stagnation. 4

Soviet Foreign Minister Molotov attended the Paris consultations but walked out on July 2, branding the plan "American economic imperialism." 5 Stalin ordered Eastern Bloc nations to refuse; the resulting split formalized the Cold War's economic fault lines. The OEEC (Organisation for European Economic Co-operation), formed by 16 recipient nations to coordinate the program, eventually became the OECD in 1961. 6 Germany's counterpart fund was channeled through KfW (Reconstruction Credit Institute), a state-owned development bank, which still operates today as Germany's third-largest bank. 3

Mirror for today: When you're deploying capital into a distressed situation — turnaround, post-merger integration, country entry — the Marshall Plan's lesson is that conditions and co-ownership usually matter more than check size. The program worked because recipients designed their own plans and bore accountability for them. Rescue money without ownership transfer rarely sticks.

When Congress rewrote every contract in America (1933)

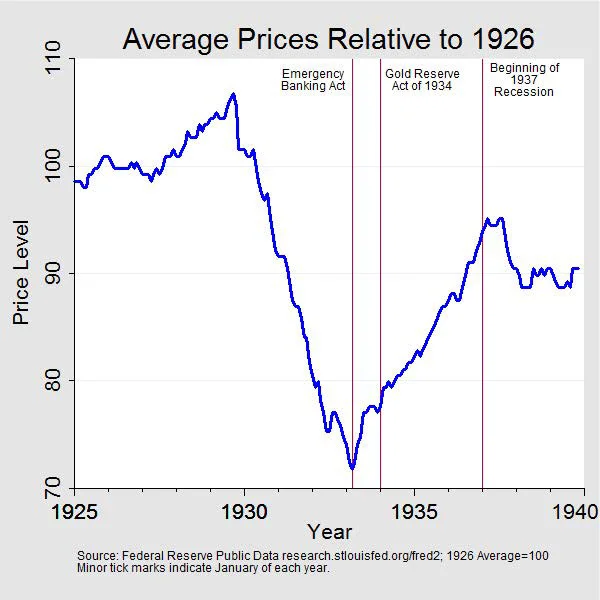

Fourteen years earlier, on this same date, Congress passed a joint resolution (Public Resolution No. 10, 48 Stat. 112) declaring gold clauses in all U.S. contracts — public and private — "against public policy" and void. 7 As of May 31, 1933, approximately $21 billion in U.S. government obligations contained gold clauses. 8 The resolution was the third step in FDR's systematic dismantling of the gold standard — following Executive Order 6102 (April 5, which forced citizens to surrender gold) and the proclamation of April 20 (which suspended convertibility). 7

The mechanism of the preceding crisis matters here. From 1929 to 1933, falling prices increased the real burden of all debt, triggering bankruptcies and bank failures, which contracted the money supply further, which drove prices down again. By March 1933, the Federal Reserve Bank of New York could no longer honor gold-conversion commitments. 7 The 40%-gold-backing requirement for Federal Reserve Notes had become a hard constraint preventing the Fed from expanding money supply to stop the spiral.

The Supreme Court's response was extraordinary. In February 1935, the Court upheld the voiding of gold clauses in private contracts 5-4. But in Perry v. United States, the majority declared that nullifying gold clauses in U.S. government bonds was unconstitutional — then refused to award the plaintiff any damages, because he couldn't legally possess or export gold anyway. 8 Chief Justice Hughes essentially said: the government broke its promise, this promise was sacred under the Fourteenth Amendment, and the bondholder cannot recover anything.

Dissenting Justice McReynolds announced from the bench that "loss of reputation for honorable dealing will bring us unending humiliation; the impending legal and moral chaos is appalling." 8 The majority's view was colder: the government's sovereign power to regulate monetary value rendered it immune from liability, even when that power was exercised unconstitutionally.

The economic outcome: Eichengreen and Sachs demonstrated that U.S. recovery began almost as soon as the gold constraints were lifted. 7 Christina Romer estimated that without the Gold Reserve Act, real GNP would have been roughly 25% lower in 1937. 9 Britain had done the same thing in 1931 and recovered faster; France stayed on gold the longest and suffered the deepest prolonged depression. 7

Mirror for today: FDR's gold actions raise a question that recurs in every systemic crisis: at what point does the rulebook become the problem? The answer in 1933 was stark — the existing monetary constitution was actively destroying value, and the political cost of breaking it was lower than the economic cost of keeping it. The Perry case adds the sharpest edge: even when the Court declared the action unconstitutional, it refused to undo it. Institutions can acknowledge a rule violation while deciding that reversal is worse than continuation. Watch for that logic the next time a major covenant gets restructured in a distressed debt deal.

Two plants that shut down the whole company (1998)

On June 5, 1998, all 3,400 United Auto Workers (UAW) Local 659 members at GM's Flint Metal Center walked out. Management had spent a holiday weekend secretly removing stamping dies and tooling from the plant, reneging on a prior commitment to invest $180 million in the aging facility. 10 Six days later, 5,800 workers at the nearby Delphi Flint East plant joined them.

The Flint Metal Center produced fenders, hoods, and engine cradles for virtually every GM vehicle assembled in North America. GM ran on just-in-time manufacturing — zero buffer stock. Within the first week, GM laid off 50,900 workers. By the strike's end on July 29, 27 of GM's 29 North American assembly plants had shut down, plus over 100 parts facilities across the U.S., Mexico, and Canada. 10 Total workers idled: approximately 200,000. 11

The financial damage: $12 billion in lost production revenue and roughly $2.8–3 billion in lost profit. 10 GM reported a Q3 1998 net loss of $809 million, its largest quarterly loss in 62 years. 12 Approximately 500,000 vehicles were never built.

The settlement, reached July 29, required GM to make the $180 million investment it had canceled — plus $20 million more at Delphi East. 10 Three days later, GM announced it would spin off its entire Delphi parts division. On August 5, GM Chairman John Smith announced a plan to build new assembly plants requiring far fewer workers. UAW's Dean Braid summarized what workers at Buick City were saying: "Now the clipboard people will have a whip and a gun." 10

The underlying deterioration was structural, not caused by the strike. GM employment in Flint had already fallen from roughly 80,000 in the late 1970s to 33,000 by 1998, and continued to roughly 7,500 by 2013. 13 Former GM labor relations director Art Schwartz put it plainly: "Nobody won that strike. Everybody lost." 13 Meanwhile, GM's hourly total labor cost stood at approximately $73 by 2006 versus Toyota's ~$48, a gap driven almost entirely by retiree healthcare and pension "legacy costs" — adding an estimated $3,000 per vehicle by 2008. 14 GM filed for Chapter 11 bankruptcy on June 1, 2009 — $82.3 billion in assets against $172.8 billion in debt. 15

Mirror for today: The Flint strike is a warning about what happens when you optimize a supply chain for efficiency at the expense of the social contract that makes it function. Just-in-time manufacturing concentrates vulnerability at strategically critical nodes. GM knew this — and still secretly moved the dies. The operational logic of efficiency and the relational logic of trust operate on different timescales, and when they collide at a chokepoint, the efficiency logic loses. The Delphi spin-off announcement three days after settlement shows that sometimes a negotiated resolution is just a brief intermission in a longer unraveling.

"We are on the side of angels" (2001)

On June 5, 2001, PBS Frontline aired "Blackout" (program #1916), a documentary on energy deregulation and the California power crisis. 16 Reporter Lowell Bergman interviewed Jeff Skilling — just four months into his tenure as Enron's CEO — and asked whether Enron was the "good guys" in the California crisis. Skilling's answer: "We are the good guys. We are on the side of angels." 16

Six months later, Enron filed for bankruptcy with $63.4 billion in assets — the largest corporate failure in U.S. history at that point. 17 Skilling resigned the CEO role on August 14, 2001, having served just six months. 18

What Skilling was defending on camera was a business that had grown revenues from $13.3 billion in 1996 to $100.7 billion in 2000. 19 Fortune had named Enron "America's Most Innovative Company" for six consecutive years. 19 What wasn't visible: CFO Andrew Fastow had built hundreds of off-balance-sheet special-purpose entities — including the LJM partnerships and the Raptor I–IV vehicles (named after dinosaurs in Jurassic Park) — that hid over $1 billion in liabilities and generated fictitious profits. 17 Fastow personally extracted at least $45 million from these structures while serving as CFO. 20

On August 15, the day after Skilling's resignation, Enron VP Sherron Watkins sent Kenneth Lay an anonymous letter: "I am incredibly nervous that we will implode in a wave of accounting scandals." 17 Lay hired Vinson & Elkins to review the concerns; the firm reported no irregularities. On October 16, Enron restated 1997–2000 profits downward by $613 million. 17 Twenty thousand employees lost their jobs. Investors lost approximately $74 billion. 18

Skilling was convicted in May 2006 on 19 felony counts including conspiracy, securities fraud, and insider trading, and sentenced to 24 years and 4 months in federal prison. 18 He served approximately 12 years. Kenneth Lay was convicted on all six counts he faced but died of a heart attack on July 5, 2006, six weeks after the verdict — before sentencing. 21 Arthur Andersen, Enron's auditor, was convicted of obstruction of justice for destroying documents; 85,000 Andersen employees lost their jobs. 17 The Sarbanes-Oxley Act, signed July 30, 2002, required CEO and CFO certification of financial statements under criminal penalty and established the Public Company Accounting Oversight Board (PCAOB) to supervise audit firms — described at signing as "the most far-reaching reforms of American business practices since the time of Franklin D. Roosevelt." 22

The Harvard Law School Forum on Corporate Governance noted in 2021 that Enron's audit committee members included the former dean of Stanford Business School and a former British energy minister — people with exceptional credentials who spent 90 minutes reviewing complex related-party transactions in February 2001. 23 Their failure was not ignorance but "a lack of the practical independence required to recognize the red flags in front of them." 23

Mirror for today: The PBS interview is a useful calibration tool because Skilling wasn't lying about his self-perception — he appears to have genuinely believed it. The question to ask yourself about high-conviction leaders (including yourself) isn't whether they believe what they're saying; it's whether the system around them has any mechanism to surface contradicting evidence. At Enron, the answer was no: the board waived its own conflict-of-interest rules to let Fastow manage entities on both sides of transactions with the company. Conviction and governance independence are separate variables. When a leader says "we are on the side of angels," the diagnostic question is who, specifically, is empowered to disagree.

Four dates, one calendar square: a $13 billion bet on European ownership, a constitutional violation that couldn't be undone, a just-in-time supply chain that collapsed at its most critical node, and a self-portrait delivered six months before the crash. Each one poses the same underlying question in a different register — how much of what you think you know about a system's resilience is real, and how much is the system working until the day it doesn't.

Cover image: AI-generated editorial composite

参考ソース

- 1The George C. Marshall Foundation – The Marshall Plan Speech

- 2Harvard Gazette – 70 years ago, a Harvard Commencement speech outlined the Marshall Plan

- 3Wikipedia – Marshall Plan

- 4DeLong & Eichengreen – The Marshall Plan: History's Most Successful Structural Adjustment Program

- 5History.com – Soviet Union rejects Marshall Plan assistance

- 6OECD – The Marshall Plan speech at Harvard University, 5 June 1947

- 7Federal Reserve History – Roosevelt's Gold Program

- 8Justia – Perry v. United States, 294 U.S. 330 (1935)

- 9Wikipedia – Gold Reserve Act

- 10Labor Notes – Flint Strikes Settled, But Issues Go Unresolved

- 11MLive – 10 things to know about historic 1998 UAW strike

- 12Los Angeles Times – GM Strike Not Expected to Have Long-Term Effect

- 13MLive – 1998 UAW strikes didn't expedite GM's departure from Flint, experts say

- 14NPR – Cutting Worker Costs Key To Automakers' Survival

- 15Wikipedia – General Motors Chapter 11 reorganization

- 16PBS Frontline – Transcript: Blackout

- 17Wikipedia – Enron scandal

- 18Wikipedia – Jeffrey Skilling

- 19Wikipedia – Enron

- 20Wikipedia – Andrew Fastow

- 21NPR – Enron Founder Kenneth Lay Dies of Heart Attack

- 22Wikipedia – Sarbanes-Oxley Act

- 23Harvard Law School Forum on Corporate Governance – Twenty Years Later: The Lasting Lessons of Enron

このコンテンツについて、さらに観点や背景を補足しましょう。