FY2022 ROE

47.2%

FY2023 ROE

38.8%

FY2024 ROE

37.1%

3yr Avg ROE

41.0%

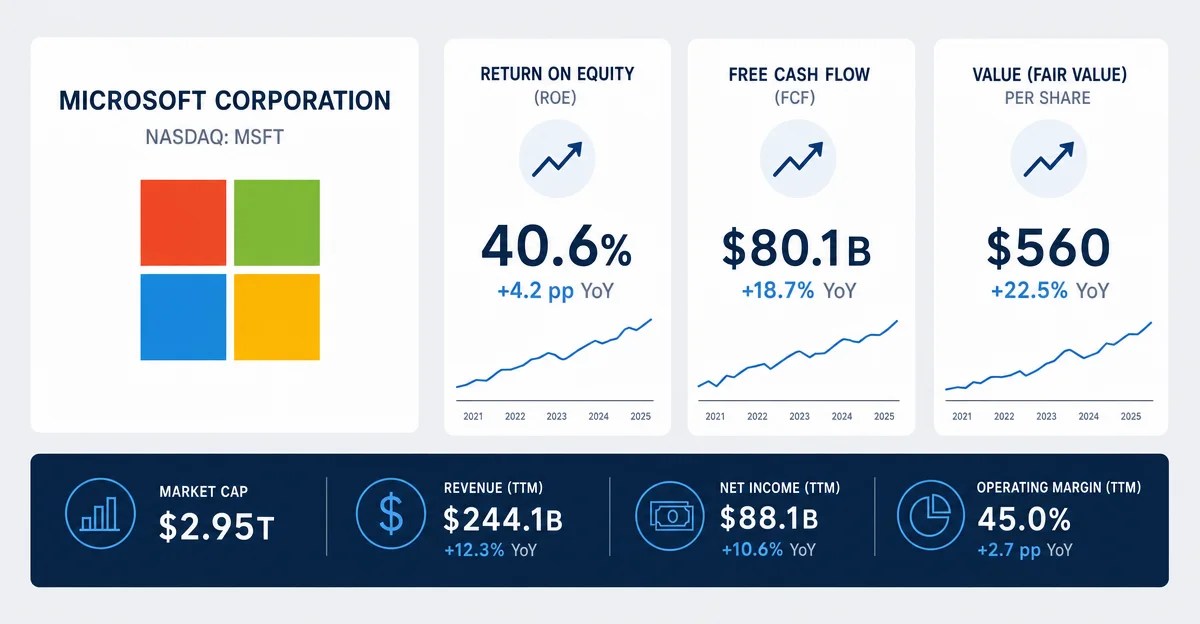

Microsoft clears all three screening gates: 3-year average ROE of 41%, free cash flow above $59B in every year since FY2022, and a forward P/E near 22× on 25% expected EPS growth. Today's data, key risks, and what the valuation implies.

| Fiscal Year | Net Income | Avg Shareholders' Equity | ROE |

|---|---|---|---|

| FY2022 (ended Jun 2022) | $72.7B | $154.3B | 47.2% |

| FY2023 (ended Jun 2023) | $72.4B | $186.4B | 38.8% |

| FY2024 (ended Jun 2024) | $88.1B | $237.4B | 37.1% |

| Fiscal Year | Free Cash Flow |

|---|---|

| FY2022 | $65.1B |

| FY2023 | $59.5B |

| FY2024 | $74.1B |

| FY2025 | $71.6B |

このコンテンツについて、さらに観点や背景を補足しましょう。