HeyGen's growth playbook: $1M to $100M ARR in 31 months on $69M raised

How HeyGen turned watermarked free videos into a viral acquisition engine, custom Digital Twins into the strongest possible switching cost, and a credit-based tier system into a self-serve expansion motion — reaching $100M ARR in 31 months on just $69M raised, profitable since Q2 2023.

HeyGen crossed $100M ARR in October 2025 — three years after launch, on $69M in funding, having reached profitability in Q2 2023.1 The company built that trajectory without a large sales motion: it grew through watermarks, viral moments, and a retention mechanic that most observers miss. The product doesn't just hold users — it holds their faces.

Acquisition: the watermark was the GTM

HeyGen launched on July 29, 2022 under a freemium model with one intentional constraint: free-tier videos carried a prominent watermark.2 This wasn't a limitation they apologized for. CEO Joshua Xu, who came from Snap's advertising team, treated the watermark the same way consumer apps treat branded sharing — the video becomes the ad, and every viewer is a potential user.

The system crashed three times in the first few months because user-generated videos went viral on social media.2 That's not a bad PR problem. That's product-market fit in log form.

A few other mechanics reinforced this flywheel:

- Fiverr before SaaS. Before building the full product, Xu ran an AI-video gig on Fiverr to validate demand — first without disclosing the AI, then after revealing it, watching customers stay. That validated ICP before a single subscription existed.2

- TalkingPhoto as PLG accelerant. Customers asked if they could use photos instead of recorded footage. HeyGen built TalkingPhoto. It was "creative and fun," boosted social sharing, and opened a new surface for video ads that required almost no production overhead.

- Generative AI map visibility. Sequoia Capital first mentioned HeyGen on October 24, 2022 — roughly 90 days after launch. That third-party credibility signal became a secondary acquisition engine and helped convert researchers into trial users.

- Milei moment. In January 2024, Argentinian President Milei's Davos speech was translated from Spanish to English using HeyGen and posted on X. Elon Musk shared it.3 The lip-sync quality surprised viewers who had no idea a $24/month tool could do that. That single event was more distribution than most companies get from six months of paid channels.

コンテンツカードを読み込んでいます…

- 20% affiliate commissions. HeyGen runs a structured affiliate program managed by Affiverse Agency, offering 20% commissions — a cost-per-acquisition model that scales with revenue rather than ahead of it.1

The ICP at launch was broad by design: creators, SMBs, non-profits, Fortune 500s, and individuals. That breadth is actually a strategic choice. By mid-2024, HeyGen reported over 40,000 paying business customers from European manufacturers to Salesforce to McDonald's — a distribution that would look strange for a developer tool but makes sense for a video production replacement.3

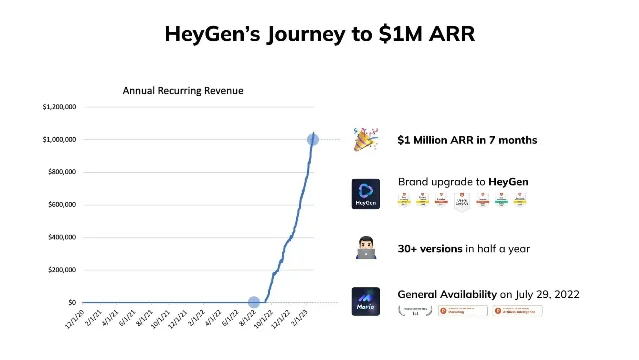

By March 2023, the company hit $1M ARR in 178 days. By October 2023, $10M. By the June 2024 Series A, it had passed $35M.4 As of October 2025, it crossed $100M.5

Retention: the avatar is the lock-in

The standard video SaaS retention story is habit formation — users log in regularly, outputs accumulate, canceling means losing content history. HeyGen has that, but its deeper retention mechanism operates at a different level.

Custom Digital Twin creation is identity migration. When a user records 2+ minutes of footage and creates a personalized avatar — their face, voice, and movement model — that asset exists only inside HeyGen. It cannot be exported, transferred, or ported to Synthesia, D-ID, or any competitor. The cost of migration is not switching fees or data export hassles. It's re-recording yourself.

This creates a retention dynamic similar to ElevenLabs' voice cloning: the more a user invests in building their digital identity inside the platform, the higher the switching cost becomes. A solo founder who has recorded their custom avatar and built a library of branded training videos, product demos, and sales outreach videos faces a significant emotional and operational hurdle to leave.

The second retention layer is workflow lock-in through integrations. By April 2025, HeyGen had embedded into HubSpot's marketing automation platform — meaning enterprise buyers who already manage contacts, sequences, and campaigns in HubSpot can generate personalized avatar videos from within that workflow.4 The Canva integration (live March 2026) goes further: HeyGen avatars are available as a native feature inside Canva's 150M-user base.6

Once HeyGen is embedded in the tools where a marketing team already spends 40+ hours per week, cancellation requires switching both the video platform and the surrounding workflow — a much heavier lift than canceling a standalone SaaS.

The third layer is video library accumulation. Enterprise accounts generating dozens of localized video assets — training videos, ad variants, investor communications — accumulate a body of work that is meaningless without the avatar models used to generate it. Trivago, which used HeyGen to simultaneously localize TV ads across 30 markets, cut post-production time in half and saved 3–4 months on average.7 For a marketing team operating at that scale, the switching cost is the entire localization infrastructure they built around HeyGen's pipeline.

Monetization: two revenue streams, one credit layer

HeyGen's monetization model makes a specific architectural choice: it runs SaaS subscriptions and an API business simultaneously, with credits as the shared unit connecting both.

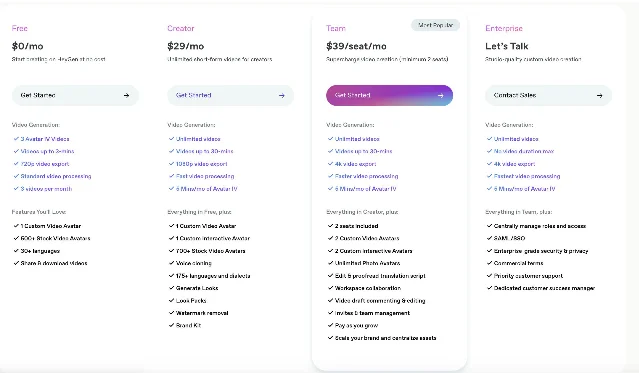

The SaaS ladder goes Free ($0, 3 videos/month, 1-minute max, watermark) → Creator ($29/month, 600 credits) → Pro ($49/month, 1,000 credits, 4K export) → Business ($149/month, 1,500 credits, team seats at $20/seat) → Enterprise (custom pricing, no video duration cap, highest concurrency).8

Credits are HeyGen's single billing currency. An Avatar III video costs 3 credits/minute; Avatar IV or V costs 20 credits/minute; full video translation with lip-sync runs 5 credits/minute.8 This creates a natural upgrade path — users who want newer, higher-quality avatar models consume credits faster, driving tier upgrades.

The Pro tier has a usage-based expansion vector built in: "All Pro tiers include the same features — only the monthly credit allocation changes. Tiers range from 1,000 credits/mo at $49 to 100,000 credits/mo at $4,300."8 A single user can scale from $49/month to $4,300/month without ever talking to a salesperson.

The API business runs on a parallel credit model: Free (10 credits/month) → Pro ($99/month, 100 credits) → Scale ($330/month, 660 credits) → Enterprise. Interactive Avatar streaming costs 0.2 credits per minute of real-time session.1 This tier serves platforms that want to embed AI avatar features without building the models themselves — Reply.io integrated HeyGen's Interactive Avatars for conversational chatbots; Icon.me and similar platforms reportedly white-label HeyGen's technology for UGC advertising.1

The API business introduces a structural tension worth noting: when HeyGen's API clients (Icon.me, Arcads, MakeUGC) sell avatar-generated content to the same SMB market that HeyGen's SaaS targets, the company ends up competing against customers who are also paying it. Sacra flags this dynamic as a long-term risk — API revenue grows, but so does the market of well-funded competitors powered by HeyGen's own infrastructure.1

Gross margin context: The company relies on ElevenLabs for voice synthesis and licenses OpenAI's real-time voice API for Interactive Avatars.1 That pass-through cost structure means HeyGen's margins are partially determined by its infrastructure supplier relationships — an unusual position for a platform that has already reached profitability at these ARR levels.

The $60M Series A from Benchmark (June 2024, $500M valuation) is being used to build the enterprise motion that requires dedicated sales engineering, customer success, and compliance infrastructure — the assets HeyGen needs to move from SMB-led growth into the Fortune 500 territory that Synthesia ($146M ARR) currently owns.9

Takeaways

1. The watermark as viral distribution. HeyGen didn't suppress the fact that free videos have limitations — it weaponized that fact. Every watermarked video is an ad with a production value that free-tier users couldn't otherwise afford. Builders building in video, voice, or any output-generating tool should ask whether their free output does something in the world that their competitors' free outputs don't.

2. Avatar as identity = strongest possible switching cost. The product most likely to retain users long-term is the one that stores a piece of themselves — literally, in HeyGen's case. This pattern appears in ElevenLabs (voice clones), Granola (shared note archives), and Cursor (proprietary model behavior learned from your codebase). The question to ask: does your product accumulate something irreplaceable for each user, or just content they could recreate?

3. Credit-based expansion is cleaner than seat-based expansion for usage-intensive tools. HeyGen's Pro tier runs from $49 to $4,300/month based entirely on credit allocation — no sales call required. A power user wanting to produce 1,000 videos/month can upgrade themselves. Compare this to per-seat models where expansion requires an admin to add users: credits scale with activity, seats scale with headcount.

4. Embedding in workflows is the moat, not the product. HeyGen's integrations with HubSpot and Canva mean that its most important retention driver isn't the avatar quality — it's the question of what marketers would have to do differently if they left. Platform distribution through established tools is harder to replicate than any single product feature.

参考ソース

- 1HeyGen Revenue, Valuation & Funding

- 2HeyGen's $0 to 1M ARR Journey

- 3HeyGen Secures $60M Series A

- 4Contrary Research: HeyGen Business Breakdown

- 5HeyGen AI Net Worth, Revenue, Marketcap

- 6Meet the new HeyGen x Canva integration

- 7Trivago Streamlines Global Ad Localization with HeyGen

- 8HeyGen Pricing

- 9HeyGen raises $60M Series A

このコンテンツについて、さらに観点や背景を補足しましょう。