How embarrassing.

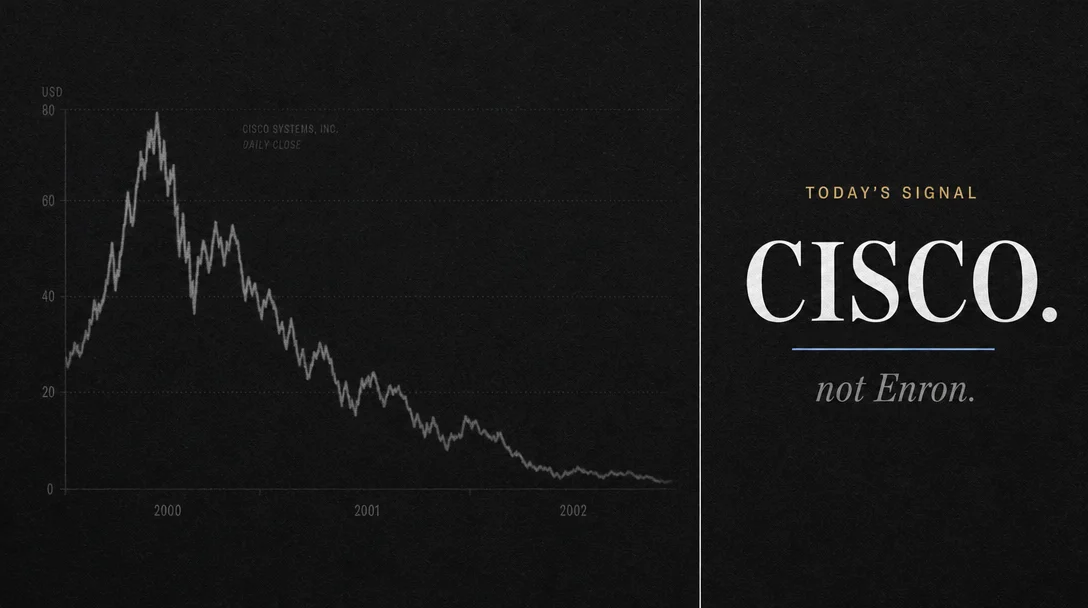

Burry: Nvidia is "clearly Cisco" — not Enron

Michael Burry clarifies his Nvidia thesis: it's a Cisco-2000 scenario, not Enron. He cites $182B in non-cancellable supply obligations, temporary tokenmaxxing-driven demand, and $662B in hyperscaler off-balance-sheet exposure — published in response to Nvidia's own seven-page analyst rebuttal.

Michael Burry (Scion Asset Management, founder; best known for his 2008 subprime short detailed in The Big Short) published a new Substack essay on May 25 titled "Short Thoughts May 25, 2026 — Patterns, NVIDIA's Settled State & the Hong Kong Crackdown." 1 The post is paywalled, but Burry announced it on X and secondary sources captured its core arguments in detail.

The occasion for the piece: Nvidia had circulated a seven-page memo to Wall Street analysts defending its business against what it called inaccurate characterizations — including, evidently, Burry's prior critiques. Burry's response, posted on X at 2:39 AM UTC on May 26, was succinct: "How embarrassing." 2 The full rebuttal came in the essay itself.

コンテンツカードを読み込んでいます…

コンテンツカードを読み込んでいます…

The core claim: Cisco, not Enron

Burry was precise about what he is and is not arguing:

"I stand by my analysis. I am not claiming Nvidia is Enron. It is clearly Cisco." 3

The distinction matters. Enron was a fraud — its collapse was about fabricated financials. Cisco in 2000 was a real, dominant company selling real equipment into a genuine infrastructure buildout. Its stock still fell more than 85% from peak to trough as the buildout demand proved temporary and inventory overhang crushed margins. Burry is saying the same mechanics — not fabrication, but over-commitment to a demand curve that won't hold — apply to Nvidia now.

What the mechanics look like

Burry's essay identifies several interlocking pressures, according to coverage by Stocktwits: 4

Demand is temporary, not structural. Burry argues that a significant portion of current GPU demand is driven by what he calls "tokenmaxxing" — companies forcing employees to burn through token allocations via unpaid prompt work to feed training pipelines — along with benchmarking runs and trace-harvesting. These activities are classified as permanent demand in financial models but represent a training-phase artifact. Once models are trained, the need drops.

Customer concentration amplifies the risk. Burry contends Nvidia is selling into "a concentrated set of buyers whose demand is being distorted by a training phase that will not last." 4 He quantified the exposure: if Microsoft alone cuts its Nvidia chip capex by 20%, that translates to a 4.2% hit to Nvidia's total revenue.

The supply side is locked in. Nvidia has made $119 billion in non-cancellable production commitments to TSMC. Total forward non-cancellable obligations reach $182 billion — more than Nvidia's annual operating cash flow. If demand softens, the company cannot pull those contracts. Nvidia's purchase obligations have grown from $16.1 billion a year ago to $95.2 billion today.

Off-balance-sheet risk at the customer layer. Moody's has identified $662 billion in off-balance-sheet commitments across the five largest hyperscalers — Microsoft, Amazon, Alphabet, Meta, and Oracle. Burry argues these commitments "will become very real in a correlation event and create strong motivation to walk away from data centers en masse." 4

Accounts-receivable anomaly. Microsoft's share of Nvidia's receivables has risen even as its share of Nvidia's total revenue has fallen — a pattern Burry reads as front-loading, where inventory is pulled forward into the books ahead of actual need.

リンクプレビューを読み込んでいます…

Why this view matters now

The Cisco analog is not new for Burry — he has gestured at it before. What is new is the specificity: $182 billion in locked supply-chain obligations, a named mechanism for how demand gets overstated (tokenmaxxing), and the quantified revenue sensitivity to a single customer reducing orders.

Nvidia itself chose to respond — the seven-page memo distributed to analysts is unusual; companies don't typically publish formal rebuttals to individual short-sellers unless the arguments are gaining traction with institutional buyers. The fact that Burry's response to the memo ("How embarrassing") reached 590,000 views on X within hours suggests the audience for this debate extends well beyond his subscriber base. 2

For investors with Nvidia exposure: Burry's thesis does not require fraud. It requires only that current GPU demand is partly a training-phase artifact, and that Nvidia's supply commitments leave it with limited room to maneuver when that phase ends. The Cisco comparison is instructive: Cisco's revenues recovered over the following decade. Its stock price, from its 2000 peak, has not.

Cover image: AI-generated illustration.

このコンテンツについて、さらに観点や背景を補足しましょう。