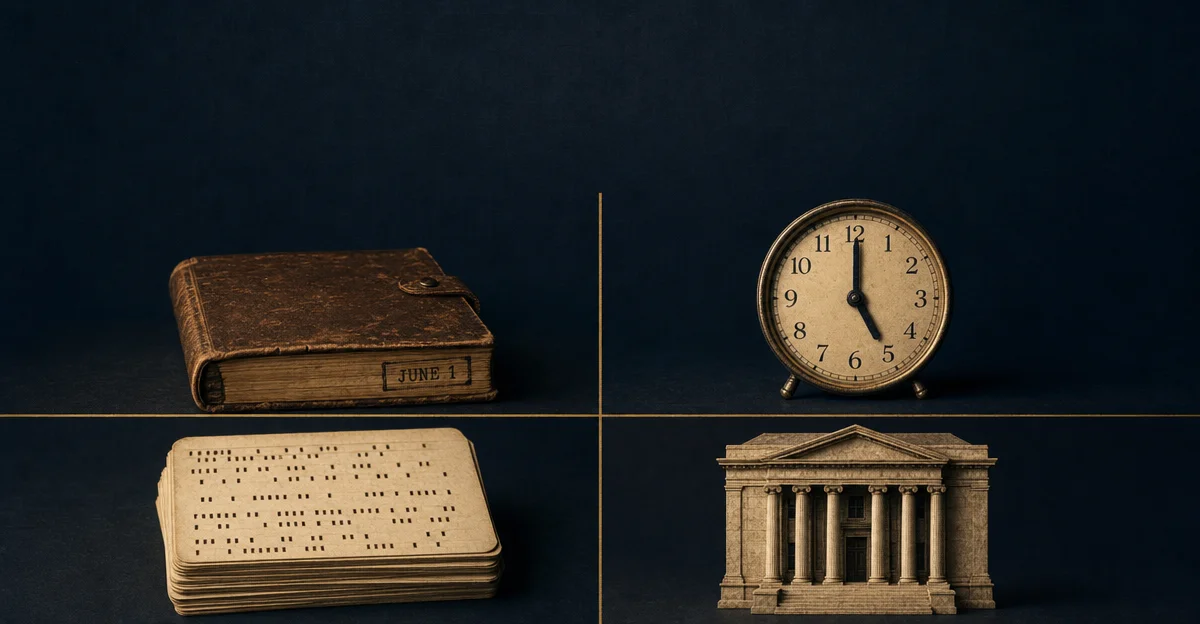

June 1: four bets the experts got wrong

Four June 1 decisions across 119 years — GM's 2009 Chapter 11 restructuring ($82B in assets, resolved in 40 days via a 363 sale at a $10.5B taxpayer loss), CNN's 1980 launch on $20M against every network's skepticism (five loss years before a $13M profit), Herman Hollerith's 1890 Census tabulating machine deployment (the one government procurement that begat IBM in 34 years), and the CIBC merger of 1961 (largest Canadian bank merger, a building block of the concentrated system that produced zero bank failures in 2008). Each carried a delayed cost that only surfaced long after the decision was celebrated.

Four June 1 decisions across 119 years — a government that dismantled and rebuilt the world's largest manufacturer in 40 days (2009), a broadcaster who bet $20 million on a format every network called financially insane (1980), a statistician whose census machine spawned an industrial giant (1890), and two Canadian banks that chose consolidation over independence (1961). Each decision was taken against the grain of expert opinion. Each carried a cost that only showed up later.

2009 — GM files Chapter 11: the largest industrial bankruptcy in American history, resolved in 40 days

At 8:00 AM EDT on June 1, 2009, General Motors filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Southern District of New York, case number 09-50026. 1 The filing listed $82.29 billion in assets and $172.81 billion in liabilities — the fourth-largest bankruptcy in U.S. history and the largest industrial bankruptcy ever, surpassed only by financial institutions (Lehman Brothers, Washington Mutual, WorldCom). 1 On the same morning, President Obama appeared in the White House Grand Foyer to explain why the federal government was betting another $30 billion on a company that had just lost $80 billion in four years.

The decline was not sudden. GM posted a $10.6 billion loss in 2005, followed by a $38.7 billion loss in 2007 (heavily weighted by a non-cash deferred tax write-down) and a $30.9 billion loss in 2008 as U.S. auto sales collapsed from 17 million annually to below 10 million. 1 Legacy costs — retiree healthcare and pension obligations exceeding $100 billion — made it structurally uncompetitive against Toyota and Honda, whose U.S. workforces carried no comparable defined-benefit legacy. By November 2008, GM warned it would run out of cash without government aid. 2 David Cole, chairman of the Center for Automotive Research, described conditions plainly: "We have an auto depression, not a recession." 2

The mechanism that made the bankruptcy work — a Section 363 asset sale — was itself the product of an unlikely meeting. In November 2008, turnaround specialist Jay Alix drove to Rick Wagoner's home and proposed splitting GM into "NewCo" (good assets, brands, viable plants) and "OldCo" (liabilities, pension obligations, shuttered facilities). 3 This structure — initially opposed by GM's own lawyers as "unorthodox and lacking precedence" — became the government's chosen path when the Obama Auto Task Force, led by Steven Rattner, took over restructuring demands in early 2009. On March 29, 2009, Obama demanded CEO Wagoner's resignation. 4 Fritz Henderson stepped in. Obama's condition for support was stark: "I determined that the original restructuring plans submitted by GM and Chrysler earlier this year did not call for the sweeping changes these companies needed to survive." 5

The bankruptcy itself ran 40 days. NGMCO Inc. — "New GM" — was the sole bidder at auction. Judge Robert Gerber approved the sale on July 5; it closed July 10. 1 New GM retained four brands (Chevrolet, Cadillac, Buick, GMC) from an original eight; Pontiac was discontinued, Saturn and Hummer wound down, Saab sold. The debt load fell from $94.7 billion to $17 billion overnight. Workforce cut from 88,000 to 68,000 U.S. employees; dealerships from 6,000 to 3,600; plants from 47 to 34. 1 The U.S. Treasury held 60.8% of the new company, Canada and Ontario 11.7%, the UAW health trust 17.5%, and unsecured bondholders 10%.

Obama called the speed decisive: "Many experts said that a quick, surgical bankruptcy was impossible. They were wrong." 5 The total TARP investment in GM came to $49.5 billion. 6 By November 2010, GM had completed a $23.1 billion IPO — the largest in North American history at the time — priced at $33 per share, reducing Treasury's stake from 60.8% to about 36%. 7 GM's 2010 full-year profit reached $4.7 billion, its first profitable year since 2004. 8 UAW workers received $4,300 profit-sharing checks that year — the highest in company history.

The final accounting came December 9, 2013, when Treasury sold its last 31.1 million shares. Total recovered: $39 billion against a $49.5 billion investment — a $10.5 billion taxpayer loss. 6 9 The Center for Automotive Research estimated the rescue saved 1.2 million jobs and preserved $34.9 billion in tax revenue; without intervention, nearly 1.9 million jobs would have been lost in 2009–2010. 6 Treasury Secretary Jacob Lew's framing: "The President understood that inaction could have cost the broader economy more than one million jobs, billions in lost personal savings, and significantly reduced economic production." 6

The rescue carried a delayed cost that the "clean break" architecture did not anticipate. The 363 sale transferred assets to New GM "free and clear" of Old GM's liabilities. When GM recalled nearly 30 million vehicles for faulty ignition switches in 2014 — defects known to engineers since at least 2005, costing roughly 57 cents per vehicle to fix — New GM initially argued it bore no responsibility for Old GM's actions. 10 The Second Circuit Court of Appeals ruled otherwise in 2016, and the Supreme Court declined to hear the appeal. 11 GM paid $900 million in criminal forfeiture in 2015 and ran a victims' compensation fund that confirmed 124 deaths. 10

The mirror: The 363 sale is the cleanest model available for separating viable assets from legacy liabilities under time pressure — 40 days to close a $173 billion debt pile is remarkable by any measure. But the GM rescue also surfaces the conditionality question: the government required Wagoner's departure and imposed real structural demands before writing checks. That sequence — accountability first, then capital — distinguishes a rescue from a subsidy. The liability shield paradox is worth filing separately: the mechanism that made the rescue work (the "free and clear" transfer) also created a moral vacuum that the courts eventually refused to honor. When you architect a clean break, the question is not just whether the new entity is viable. It is what obligations you have implicitly inherited.

1980 — Ted Turner launches CNN: the "Chicken Noodle Network" that rewrote how the world absorbs news

At 5:00 PM Eastern Time on June 1, 1980, the first broadcast of the Cable News Network went live from Atlanta, Georgia — a converted country club building on Techwood Drive — with husband-and-wife anchors Dave Walker and Lois Hart, and a lead story about a live civil rights development in Fort Wayne, Indiana. 12 13 Initial subscriber reach: 1.7 million cable households — well below the threshold to cover operating costs. Startup capital: approximately $20 million, drawn from profits Turner had earned from his WTBS superstation. 13 The media establishment had a name for what he was attempting: the "Chicken Noodle Network." 14

Ted Turner had been planning this since 1978, publicly announcing CNN in May 1979 with Reese Schonfeld, a former UPI Television News manager. 14 Turner's premise was that cable's distribution economics and the public's appetite for real-time news would make the three-network duopoly of 30-minute evening broadcasts obsolete. The networks had a budget advantage of roughly 10:1. Turner had something they did not: he would never go off the air. He announced as much directly: "We won't be signing off until the world ends. We'll be on, and we will cover the end of the world, live, and that will be our last event." 14

CNN lost a cumulative $77 million in its first five years before turning an operating profit of $13 million in 1985. 14 By then it had reached 33 million households. The validation moments came in sequence: CNN's Bernard Shaw was first on air with the Reagan assassination attempt in March 1981; 14 CNN was the only American network carrying the Space Shuttle Challenger launch live when it exploded in January 1986; 15 and during the Gulf War in January 1991, after most foreign journalists were expelled from Baghdad, CNN's Peter Arnett, Bernard Shaw, and John Holliman reported from the al-Rashid Hotel while Iraqi anti-aircraft fire lit the sky behind them. 14 President George H.W. Bush, it was said, was learning more from CNN than from the CIA. Time named Turner its Man of the Year in 1991.

Turner Broadcasting was acquired by Time Warner in September 1995 for approximately $7.5 billion in stock, making Turner the company's largest individual shareholder at roughly 11%. 16 The subsequent AOL-Time Warner merger in 2001 diluted Turner's stake from about 11% to roughly 4%, and CEO Jerry Levin stripped Turner of his management authority over the cable networks entirely. 17 Turner resigned as Vice Chairman in 2003 and liquidated nearly all his stock — collecting approximately $3 billion for a stake worth around $11 billion in 1999. His own assessment: "I lost more money than anybody in the history of capitalism!" 17 He died on May 6, 2026, at age 87, after publicly revealing in 2018 that he had Lewy body dementia. 18

The platform risk Turner built on became CNN's most serious structural problem. U.S. cable TV subscriptions peaked around 2010 at approximately 105 million households; by 2026, only 68.7 million households subscribe to traditional pay TV. 16 CNN's own U.S. subscriber base fell from 80 million in March 2021 to approximately 69 million by December 2023. 16 The attempted escape — CNN+ — lasted 23 days after launching March 29, 2022, spending an estimated $300 million before Warner Bros. Discovery CEO David Zaslav killed it on April 21. 16 CNN's current parent has since cut hundreds of positions and consolidated three separate newsrooms into one.

The mirror: The CNN story contains two lessons worth separating. The first is about first-mover advantage compounding under skepticism: Turner's five-year, $77 million burn built a brand — "the Most Trusted Name in News" — that competitors MSNBC and Fox News (both launching in 1996) took another decade to match in household reach. The value of the franchise was built during the loss years, not after. The second lesson runs in the other direction: CNN's business model was entirely constructed on the cable bundle economics that no longer exist. The subscriber-fee revenue that made CNN's news budget possible was not a function of CNN's journalism — it was a function of every pay-TV subscriber paying a per-household fee whether they watched CNN or not. When that mechanism unwound, CNN's financial floor fell with it. First-mover advantage is durable until the distribution platform it was built on stops being the platform.

1890 — Hollerith's tabulating machine runs its first Census: the government bet that seeded IBM

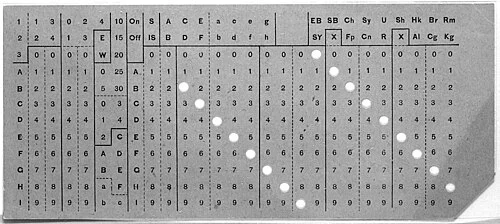

On June 1, 1890, the United States Census Bureau deployed Herman Hollerith's electric tabulating machines to process the Eleventh Census — the first large-scale use of punched-card data processing in history. 19 20 The Census Bureau rented 56 machines at $1,000 each (roughly $26,500 per machine in today's terms). 20 The result: the basic count of 62,979,766 Americans completed in six months, the full detailed tabulation in two years. The 1880 Census, conducted by hand, had taken eight years to complete — and its data was obsolete before it was published. 21 IBM later estimated the Hollerith system saved the Census Office $5 million and more than two years of labor. 20

The machine itself embodied what would later be called binary logic. Each 3.25-by-7.375-inch punched card — deliberately sized to match 1887 U.S. banknotes so Treasury containers could store them — carried rows of circular holes. 22 A spring-loaded pin pressed through an open hole contacted a mercury reservoir, closed an electrical circuit, and advanced one of 40 electromagnetic counting dials. Hole present: circuit closed. No hole: no signal. 20 IBM's own historical account notes: "This binary principle of ones and zeros is still used today in detecting the presence or absence of an electrical charge in semiconductors." An experienced operator processed 80 cards per minute on the sorting table.

Hollerith had won the 1890 contract through a competitive test in 1888, where Census Bureau officials gave three candidates the same sample of 1880 data from four St. Louis districts. Hollerith completed the data-capture phase in 72.5 hours against competitors' 144.5 and 100.5 hours; the tabulation preparation in 5.5 hours against 44.5 and 55.5. 23 The Census Bureau awarded the contract. The terms — lease, not purchase — were structural. Hollerith rented machines while selling the proprietary punched cards separately: the razor-and-blades model, a century before Gillette made it famous. 24 The lease arrangement also forced Hollerith's staff into regular client contact, since losing a maintenance relationship could mean losing the contract.

In 1896, Hollerith incorporated the Tabulating Machine Company. His machines spread to census bureaus in the UK, Germany, Russia, Austria, Canada, and Norway. 21 But in 1902, when the Census Bureau became a permanent agency, it began developing its own machines against Hollerith's expiring patents. A 1905 ultimatum — reduce prices or lose the contract — prompted Hollerith to refuse. The resulting 1910–1912 patent litigation went against him. 20 In 1911, financier Charles Ranlett Flint merged Hollerith's company with three others — a time-recording firm, a computing scale manufacturer, and a timekeeping company — to form the Computing-Tabulating-Recording Company (CTR). Hollerith sold out for $2,312,000 (approximately $65 million in 2022 dollars). 20

CTR languished until 1914, when Flint hired Thomas J. Watson Sr. as general manager — a former NCR sales executive who had been convicted on antitrust charges (later overturned) but whose sales instincts Flint still trusted. Watson doubled CTR's revenue within four years by focusing the company on the tabulating machine business, institutionalizing Hollerith's lease model as a competitive moat, and building a sales culture around the single word "THINK." 25 On February 14, 1924, Watson renamed CTR the International Business Machines Corporation. 25 From a one-government-contract census machine to the largest technology company in the world by midcentury: 34 years, one procurement decision.

The mirror: The Hollerith story is the cleanest available case study for government as first customer for transformative technology — the same arc that later defined GPS (Department of Defense), the internet (ARPANET/DARPA), and touchscreens (DARPA-funded research). The Census Bureau's 1888 competitive test — open bidding, performance-based selection, clear criteria — selected an unproven technology over established manual methods. The downstream economic consequence was IBM. The other half of the lesson is the 1905 ultimatum: the same government that created the market eventually used Hollerith's expiring patents to develop competing machines in-house. Government is simultaneously the best possible first customer and the most dangerous long-term dependency. Hollerith understood the first; he underestimated the second.

1961 — CIBC forms: the largest bank merger in Canadian history, and the foundation of a system that survived 2008

On June 1, 1961, the Canadian Bank of Commerce (founded 1867) and the Imperial Bank of Canada (founded 1873) merged to form the Canadian Imperial Bank of Commerce — the largest merger between chartered banks in Canadian history. 26 27 The combined institution had C$4.6 billion in assets and more than 1,200 branches — more resources and more branch coverage than any bank in Canada at the time. At the moment of merger, CIBC held approximately one-quarter of the total assets of all Canadian chartered banks combined. 27

The deal started with a quiet conversation. In October 1960, Imperial Bank chairman L. Stuart Mackersy appeared unannounced at the home of Commerce president Neil McKinnon at 116 Dunvegan Road in Toronto's Forest Hill neighborhood. The trigger was a threat: Barclays Bank — which had received Imperial shares as partial payment when Imperial acquired Barclays' Canadian operations in 1956 — had begun buying additional Imperial shares on the open market without informing Imperial's board. Mackersy concluded that Barclays was maneuvering toward a takeover and preferred a domestic partner. 26 According to CIBC's corporate historian Arnold Edinborough, the two men "reached an agreement to merge their banks" within ten minutes. 26

McKinnon's path to that moment was unusual. He joined the Canadian Bank of Commerce in 1925 at age 14 as a branch clerk in Cobalt, Ontario. 28 At 41, he became the bank's youngest general manager since 1886. By 1956 he was president, by 1959 chairman. On June 1, 1961, he became CIBC's first president and CEO. He served as the bank's most powerful executive until 1973. 28

The two predecessor banks brought complementary histories. The Canadian Bank of Commerce had grown through more than fifteen acquisitions since its founding in the year of Confederation — Gore Bank (1870), Bank of British Columbia (1901), Bank of Hamilton (1924), Standard Bank of Canada (1928) — becoming a national institution with over 700 branches and Canada's first personal loan offering in 1936. 29 Imperial Bank, nicknamed the "Mining Bank," had built its reputation in mineral resource financing, maintained 343 branches, and held over C$1 billion in assets by 1961. 30

The merger's long-term significance lay not in CIBC's own trajectory — the bank would fall from Canada's largest to fifth among the Big Five after a failed U.S. expansion and a $2.4 billion Enron-related class action settlement in the 2000s 31 — but in what this class of consolidation built at the system level. Canada's Constitution Act of 1867 gave the federal government sole jurisdiction over chartered banking, preventing the fragmented dual-regulator structure that characterized American banking. Mergers like CIBC's created large, diversified institutions whose geographic and sectoral spread absorbed regional shocks. 32

The payoff came in 2008. During the global financial crisis, Canada had zero bank failures and zero government bailouts of insolvent institutions. 32 This was not a one-off: Canada also had no bank failures during the 1930s Great Depression, the Panic of 1907, or the Panic of 1893 — while the U.S. experienced major banking panics in every one of those events. Bordo, Redish, and Rockoff (NBER, 2011) trace the root cause to a structural divergence: "In Canada the banking system was created as a system of large financial institutions whose size and diversification enhanced their robustness." 32

The same researchers flag the trade-off directly: "Greater stability may have come at a cost." A concentrated, regulated system "may have been slower to innovate, may have been slower to invest in emerging sectors, and may have provided services at monopoly prices." 32 Canada's Big Five collectively hold over C$6 trillion in assets and dominate the domestic market. When Finance Minister Paul Martin blocked CIBC's proposed merger with Toronto-Dominion in 1998 — alongside the BMO-Royal Bank proposal — he argued the deals would create too much concentration and "severely reduce competition." 29 That decision is now widely cited as one reason the 2008 crisis landed more softly in Canada than elsewhere. 31

As of 2025, CIBC holds C$1.117 trillion in assets, employs 49,824 people, and serves 15 million clients globally. 26 The 1961 deal that started in a Forest Hill living room has accumulated into a balance sheet that would rank among the 40 largest financial institutions in the world.

The mirror: The CIBC story is really about regulatory architecture and the long-run consequences of industry structure decisions. Mackersy's ten-minute handshake was driven by a defensive reflex — he preferred a domestic acquirer over a British one. But the system-level effect of that choice, replicated across decades of Canadian banking consolidation, was a financial sector resilient enough to navigate the worst global crisis since the 1930s without a single failure. The concentration-competition trade-off Bordo, Redish, and Rockoff identify is genuine: stability may cost innovation speed and consumer pricing power. The question for any regulator or board is not whether concentration creates risk, but which risk is harder to manage — systemic fragility, or the slower-accumulating cost of reduced competitive pressure. Canada has spent 160 years on one side of that trade-off. The U.S. has spent the same period on the other.

Cover image: AI-generated editorial illustration.

参考ソース

- 1Wikipedia: General Motors Chapter 11 reorganization

- 2The Guardian: General Motors declares bankruptcy

- 3Forbes: How General Motors Was Really Saved

- 4White House: Remarks by the President on General Motors Restructuring

- 5NPR: Transcript: Obama's Remarks on General Motors

- 6U.S. Treasury: Treasury Sells Final Shares of GM Common Stock

- 7NPR: General Motors Shares Jump in Return to Market

- 8The New York Times: Resurgent G.M. Posts 2010 Profit of $4.7 Billion

- 9CNBC: Government sells the last of its GM stake

- 10Wikipedia: General Motors ignition switch recalls

- 11PBS NewsHour: Supreme Court turns away General Motors appeal

- 12HISTORY.com: CNN launches, June 1, 1980

- 13Library of Congress: CNN Launched 6/1/1980

- 14New Georgia Encyclopedia: CNN

- 15CNN: Defining moments from 40 years of CNN

- 16Wikipedia: CNN

- 17Fortune: Remembering Ted Turner

- 18CNBC: Ted Turner, outspoken founder of CNN, dies at 87

- 19WIRED: June 1, 1890: Census Bureau Can Finally Keep Tabs on Growing Nation

- 20IBM: The punched card tabulator

- 21Wikipedia: Herman Hollerith

- 22Columbia University: Hollerith 1890 Census Tabulator

- 23U.S. Census Bureau: The Hollerith Machine

- 24Wikipedia: Computing-Tabulating-Recording Company

- 25IBM: The origins of IBM

- 26Wikipedia: Canadian Imperial Bank of Commerce

- 27CIBC Corporate History: A New Bank, 1961–1986

- 28Wikipedia: Neil J. McKinnon

- 29Company-Histories.com: Canadian Imperial Bank of Commerce

- 30Wikipedia: Imperial Bank of Canada

- 31Wikipedia: Big Five banks of Canada

- 32NBER: Why Canada Didn't Have a Banking Crisis in 2008

このコンテンツについて、さらに観点や背景を補足しましょう。