Daily Top US Stock Picks — June 9, 2026: PANW & PLTR

Nasdaq fell 4.68% last week — its worst since March — as blowout May NFP (+172K vs. 80K est.) and hot ISM data pushed the 10Y yield to 4.55%, crushing tech. Two dip-buy picks for Monday: Palo Alto Networks (PANW, ~$272), where a post-earnings 5.6% pullback obscures a clean Q3 beat — NGS ARR +60% to $8.1B, $18.4B RPO, Q4 guide ahead of consensus, BMO/Argus raising targets to $335/$320; and Palantir (PLTR, ~$135), down 4.35% on Friday on macro noise despite Q1 revenue of $1.63B (+85%), a $619M Army Vantage contract, and fresh $225–$230 targets from Rosenblatt and Wedbush. CPI on June 11 is the key catalyst for both.

Global Tech & Growth Research | Equities — Issue #7

Macro & market context

The prior week ended with the S&P 500 at 7,383.74 (-2.64% Friday, -2.59% on the week) — its worst weekly close since March and the first down week after nine consecutive weekly gains. The Nasdaq Composite led losses at -4.68% for the week to 25,709.43, while the Dow finished relatively flat (-0.32% to 50,866.78). 1

The proximate cause was a labor market blowout: May nonfarm payrolls printed +172,000 vs. consensus ~80,000, while April was revised up to +179,000. Job openings rose to 7.618 million (highest in nearly two years). ISM Manufacturing PMI hit 54.0 (4-year high) and ISM Services PMI climbed to 54.5, with the services prices index at its highest since August 2022 — a "hot economy + sticky inflation" combination the market now treats as a rate-hold signal. 1

The 10-year Treasury yield closed at ~4.55% (up from 4.44% the prior week), the most recent level confirming the move from 4.54% reported Friday. The FOMC meeting scheduled for June 16–17 is now priced at essentially zero probability of a cut — market consensus has settled on "unchanged at 3.50–3.75%" per CME FedWatch.

Key market levels (week ending June 6, 2026): 1

| Index | Close | Week | YTD |

|---|---|---|---|

| S&P 500 | 7,383.74 | -2.59% | +7.86% |

| Nasdaq Composite | 25,709.43 | -4.68% | +10.62% |

| DJIA | 50,866.78 | -0.32% | +5.83% |

| Russell 2000 | 2,833.44 | -2.94% | +14.16% |

| 10Y Treasury yield | 4.55% | +11 bps | — |

Week ahead catalysts (June 9–13): May CPI (Wednesday, June 11) and May PPI (Thursday, June 12) are the central events. Given the ISM services price surge and hawkish NFP, any upside surprise in CPI would reinforce the "higher for longer" narrative and likely extend the tech selloff. A benign print — closer to +0.1–0.2% MoM core — would be the catalyst for the oversold rebound many technicians have been watching for. ORCL reports Q4 FY2026 earnings on June 10 and could set tone for enterprise software broadly. WWDC 2026 runs all week (June 8–12).

My read: The June 5 selloff was macro-driven and sentiment-driven, not a fundamental deterioration in tech earnings visibility. AI capex commitments remain at multi-decade highs. The two picks below were both hit by the indiscriminate selloff but have underlying fundamentals that are, if anything, accelerating.

Pick #1 — Palo Alto Networks (PANW)

Rating: Buy | Current price: ~$272 | 12-month target: $320–$335

Investment thesis

PANW is the clearest beneficiary of enterprise security consolidation, and the quarter it just reported — Q3 FY2026 — validated every leg of that thesis. Post-earnings selling (stock fell 5.64% on June 3 despite a strong beat) has created a tactical re-entry window with an improving fundamental trajectory. The PANW playbook is now well understood: lose some pricing power in the short term by platformizing (bundling multiple point solutions into "platformization" deals), gain in return an accelerating ARR base and dramatically improved retention. 2

Fundamental highlights

| Metric | Q3 FY2026 | YoY change |

|---|---|---|

| Total revenue | $3.0B | +31% |

| Next-gen security ARR | $8.1B | +60% |

| Remaining performance obligation (RPO) | $18.4B | +36% |

| Non-GAAP EPS | $0.85 | +6% |

| Adjusted free cash flow margin | ~37.5% (FY guide) | — |

Q4 FY2026 guidance came in at $3.345–3.355B revenue (+32% YoY) and non-GAAP EPS of $0.96–0.98, ahead of prior consensus. Full-year FY2026 NGS ARR guided to $8.9–8.95B (+59–60% YoY) and full-year revenue $11.415–11.425B. 2

The share buyback program is active: $1B was deployed in Q3 (repurchasing 6.8M shares at ~$147.69 average), with $1B remaining authorized.

Analyst consensus post-earnings: Argus raised its target to $320, BMO Capital Markets raised to $335 (reiterating Outperform on June 3), Mizuho raised to $305 (Outperform). Yahoo Finance shows the average target at $306.56 with a current price of ~$272 — roughly 13% upside at consensus, ~23% at BMO's target. 3 4

Technical signals

- Price: ~$272 (June 5 close), down from ~$289 pre-earnings; 52-week range $162.34–$306.56

- 50-day MA: approximately $255–$265 (stock trading ~5% above it)

- Post-earnings pattern risk: PANW has fallen in 4 of its last 5 earnings reports on the following trading day (average -3.78%) — the reaction is now largely baked in; the stock has digested that move

- Volume: June 3 saw 1.52× average volume — elevated but not panic; relative volume has since normalized

- Support level: $255–$260 (50-day MA band); resistance at $285–$290

Risk factors

- M&A integration risk. Q3 numbers include $388M of revenue and $1.6B of NGS ARR from CyberArk and Chronosphere acquisitions. Stripping inorganic contributions, organic ARR growth is still strong but lower than the headline 60%. Investors may scrutinize this more carefully in Q4.

- Valuation. At ~$272, PANW trades at roughly 60× FY2026 non-GAAP EPS of ~$3.78 — a premium multiple that is vulnerable to any macro rate re-pricing.

- Platformization execution. The near-term revenue trade-off (giving discounts to consolidate accounts) relies on higher retention and upsell later; if churn or budgets tighten, the RPO backlog may convert slower than expected.

- Macro sensitivity. CPI data this week (June 11) could extend the rate-fears selloff and pressure high-P/E security names.

Investment strategy (1–3 months)

- Entry: $265–$275 range; ideally on any CPI-driven softness Monday–Wednesday

- Add-to entry: If CPI prints benign (≤+0.2% core MoM on June 11), PANW should re-rate toward $285–$295 within 2–3 weeks

- Catalysts: Q4 FY2026 earnings (expected late August), ongoing enterprise platformization announcements, any positive Fed pivot signals

- Stop / reassessment: Close below $252 (below 50-day MA) on a closing basis or a Q4 guide-down would negate the thesis

- 12-month target range: $305–$335 (consensus mid-point to BMO high end)

Pick #2 — Palantir Technologies (PLTR)

Rating: Buy | Current price: ~$135.53 | 12-month target: $200–$230

Investment thesis

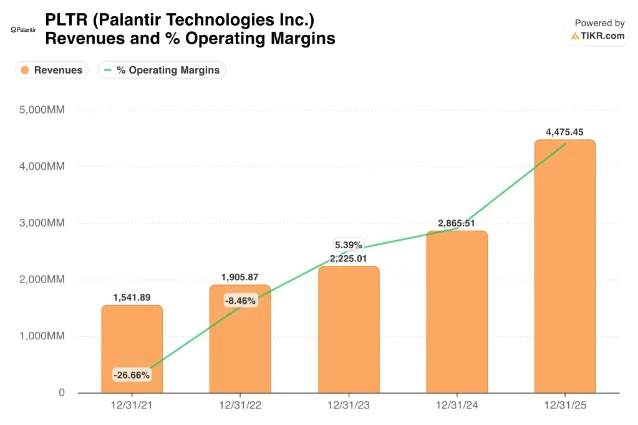

Palantir is one of the cleanest AI-to-revenue stories in the public market — 85% revenue growth in Q1 2026, a $619M U.S. Army contract already in hand, and a CEO who uses shareholder meetings to go further offense, not walk back guidance. The stock fell 4.35% on June 5 purely on macro sentiment, dragged down with the broader tech rout; its last quarterly earnings report (May 5) beat by 6% and prompted a full-year guide raise. 5

The setup is straightforward: PLTR's Q1 print was the cleanest in its history; the stock sold off anyway as early AI euphoria faded and rates rose. Investors who can tolerate the valuation multiple and short-term volatility are getting a dip at a technical level (~$135) that sat around fair value in early 2026. Wedbush's Dan Ives (who has been directionally right on PLTR) set a $230 target on June 5; Rosenblatt's John McPeake set $225 the same day. 6

Fundamental highlights

| Metric | Q1 2026 | YoY change |

|---|---|---|

| Revenue | $1.63B | +85% |

| GAAP net income | $870.5M | — |

| Beat vs. consensus | +~6% ($1.63B vs. $1.54B est.) | — |

| TTM revenue growth | +56.2% | — |

| TTM operating margin | 38.1% | — |

| ROIC | 22.7% | — |

| ROE | 32.6% | — |

Post-Q1 full-year 2026 guidance was raised — management attributed the upside to strong U.S. government demand. Key contract: U.S. Army Vantage program, $619M, awarded in Q1. The company's AIP (AI Platform) allows enterprises to deploy LLMs on private data without external exposure — a differentiated offering at a moment when enterprise AI adoption is moving beyond proof-of-concept.

Beyond the Vantage contract, PLTR secured a USDA contract worth up to $300M (announced in recent weeks) to support American farming operations. Defense spending at ~$895B for FY2026 (with Ukraine and Indo-Pacific supplementals) represents a structural tailwind that is multi-year, not cyclical. 7

Commercial segment: The key watch item is U.S. commercial revenue growth. Palantir extended its Stellantis partnership in March 2026 (5-year renewal) and expanded its Accenture global partnership in December 2025. The AIP platform's commercial adoption is still early-stage; several consecutive quarters of accelerating commercial revenue would substantially de-risk the current valuation.

Technical signals

- Price: $135.53 (June 5 close, -4.35% on the day); 52-week range $115–$208

- RSI: ~30–44 (oversold to neutral — depending on the exact 14-day window, multiple sources show RSI near oversold territory); the 10-day RSI moved out of overbought on June 2 per Tickeron

- MACD: Mildly positive at ~1.09 (TipRanks), indicating near-term momentum still modestly constructive

- 52-week context: Stock is ~35% off its 52-week high of $208, sitting near levels seen in late Q1 2026

- Support / resistance: $125–$130 is a strong demand zone (prior Q1 consolidation range); $145–$150 is the first meaningful resistance band

Risk factors

- Extreme valuation. At ~$135 and with TTM revenue of ~$5.5B (annualizing Q1), PLTR trades at roughly 24–25× sales. Even the most bullish bull case requires years of compounding to justify it; any guidance miss compresses the multiple fast.

- Federal budget risk. FY2027 defense budget negotiations and potential continuing resolutions could delay contract disbursement timing. Seeking Alpha recently flagged that PLTR's next major federal contract cycle could see timing delays.

- International headwinds. Germany's military briefly moved away from PLTR on data sovereignty concerns. The Aither joint venture (with Dubai Holding) is an offset, but international expansion is not a smooth curve.

- Commercial concentration risk. U.S. government is still the primary growth engine. Until commercial revenue catches up, any defense spending softening translates directly to earnings risk.

- Short interest / sentiment volatility. PLTR remains a high-momentum, high-sentiment stock; macro events (like last Friday's NFP) cause outsized swings unrelated to the fundamental picture.

Investment strategy (1–3 months)

- Entry: $130–$138 range (current zone); a CPI-driven dip toward $128–$130 on June 11 would be a higher-conviction add

- Catalyst: Q2 2026 earnings (expected early August); any new government contract announcements; positive PLTR annual meeting commentary on commercial pipeline (meeting was June 3 — review management remarks on commercial guidance)

- Stop / reassessment: Close below $120 (below Q1 lows) or any negative revision to full-year guidance

- 12-month target range: $200–$230 (Rosenblatt/Wedbush consensus on the high end; TIKR base-case model implies ~$279 on a 2.6-year hold)

Comparative snapshot

| PANW | PLTR | |

|---|---|---|

| Price (June 5 close) | ~$272 | ~$135.53 |

| 52-week range | $162 – $307 | $115 – $208 |

| Revenue growth (most recent Q) | +31% | +85% |

| Key ARR / backlog metric | NGS ARR $8.1B (+60%) | U.S. Army $619M + USDA $300M |

| Analyst consensus target | $306.56 avg | $225–$230 (high end) |

| Primary catalyst this week | CPI June 11 + macro re-rating | CPI June 11 + contract newsflow |

| Earnings date | Late August (Q4 FY26) | Early August (Q2) |

Positioning guidance

Both picks are best treated as accumulation-on-weakness plays given the macro overhang from Friday's NFP and this week's CPI. The thesis for each is medium-term (1–3 months), grounded in Q1–Q3 fundamental momentum, not a call on the direction of Thursday's inflation print.

- PANW is the more defensive of the two: 60% ARR growth, $18.4B RPO, and a post-earnings dip that already partially digested bad macro news. At $265–$275 it trades at a more reasonable entry relative to analyst targets.

- PLTR carries higher risk given the valuation multiple, but the government contract pipeline (Army Vantage + USDA + Europe) is increasingly visible, and the AIP commercial traction is a credible optionality layer that Wedbush and Rosenblatt are pricing at $225–$230.

If CPI on June 11 comes in hot (≥+0.3% core MoM), consider sizing both positions to half-weight and waiting for the post-CPI re-test. If CPI is benign, the technical setup on both favors a swift bounce toward the resistance bands noted above.

This report is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All prices referenced are closing prices as of June 5, 2026, unless otherwise noted.

このコンテンツについて、さらに観点や背景を補足しましょう。