www.scotiabank.com

The Global Week Ahead: Is This One For Real?

Scotiabank Economics on the bond selloff, Fed hike risk, and the payroll revision time bomb coming in September.

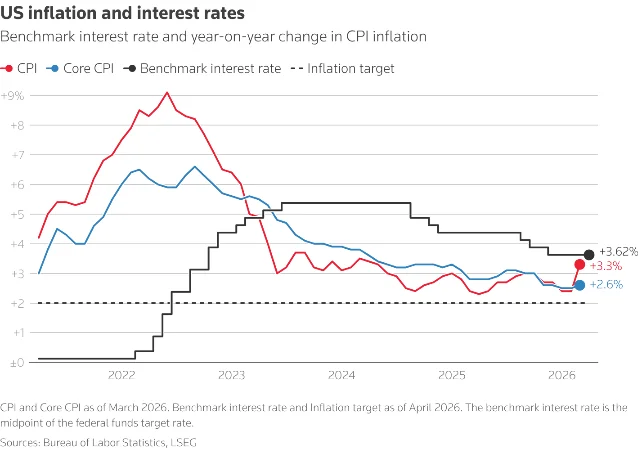

Brent crude swung from $112 to $102 and back to $105, pulling Treasuries, FX, and equities with it. The FOMC minutes confirmed a hawkish shift, Kevin Warsh was sworn in as Fed Chair, UK and European PMIs slipped into contraction, and Japan's soft April CPI clouded BoJ hike timing — all while markets start pricing a Fed rate increase by year-end.

| Central bank | Current rate | Recent decision | Bias this week |

|---|---|---|---|

| Fed | 4.25–4.50% | Hold (Apr 29–30, 8-4 vote) | Hike watch: ~25 bps priced by year-end; Warsh sworn in Fri |

| ECB | 2.00% | Hold (Apr); first hike likely June | Hawkish; Eurozone CPI at 3.0% y/y in April |

| BoJ | 0.75% | Hold; 3 dissenters voted to hike Apr | Soft Apr CPI (1.4% vs 1.6% est.) briefly cooled hike bets |

| BoE | 3.75% | Hold; 1 dissent for hike | UK flash PMI collapsed to 48.5; hike timing uncertain |

| RBA | Hold after 3 hikes | Pause favored | Weak jobs; trimmed-mean CPI still near 3.5% y/y |

| PBoC | 1-yr LPR 3.0%; 5-yr 3.5% | Hold | Easing pressure building into H2 amid slower growth |

Scotiabank Economics on the bond selloff, Fed hike risk, and the payroll revision time bomb coming in September.

이 콘텐츠를 둘러싼 관점이나 맥락을 계속 보강해 보세요.