I wrote this early this morning and I wasn't sure if I would actually publish it, but here it is

Five founder essays that cut through the AI noise

A bootstrap-edition digest covering six long-form pieces by five writers. Elad Gil's two April essays deliver dense data and five decision-ready frameworks. Sam Altman, Paul Graham, Jensen Huang and Andy Jassy each converge on a single thesis: this is a once-in-a-generation buildout — and every section closes with a concrete implication for early-stage AI founders.

Five months into 2026, some of the sharpest founder thinking is scattered across personal blogs, shareholder letters, and commencement stages — not on X feeds or in press releases. This edition covers February through mid-May: six long-form pieces by five writers who collectively influence how capital, talent, and models flow through the AI stack. For each piece, the publication date is noted so you can weigh the freshness yourself.

Elad Gil on where the money is actually concentrating

Published 2026-04-16 1

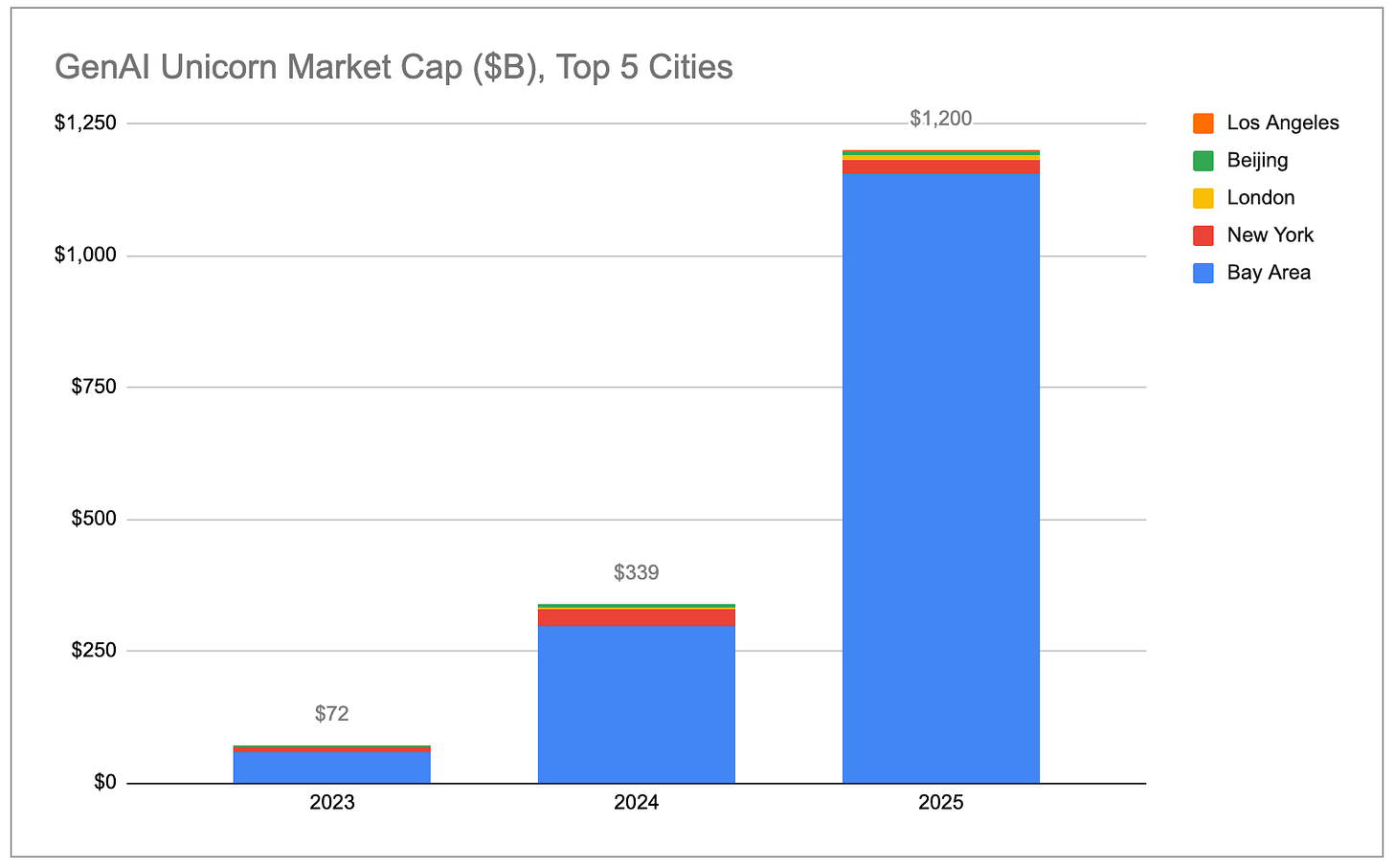

Elad Gil (investor, former Color Genomics co-founder and CEO; early exec at Twitter and Google) ran CB Insights data through analyst Shreyan Jain and published results that should reframe how you think about location.

The headline number: the San Francisco Bay Area holds 91% of global GenAI unicorn market cap. 1 No other city exceeds 2%.

For overall unicorn market cap (not just GenAI), the Bay Area's share rose from 29% to 39% in a single year — more than 4× the next city. 1 The U.S. as a whole now holds 65% of global unicorn market cap, up from 58%.

The less-obvious finding: new unicorn formation has collapsed. Only about 300 new unicorns were created between 2022 and 2025 — compared to over 900 in the three years before that. 1 But the companies that do cross the $1B mark are bigger and faster-growing than in prior cycles. As Gil puts it: "While it's harder to become a unicorn, those companies that do pass the $1B mark are on average more valuable and faster-growing than previous years." 1

In 2025, 48 GenAI unicorns grew their combined valuation by $778 billion — more than the remaining 1,100+ non-AI unicorns combined. 1 The average GenAI unicorn added ~$2.2B in valuation year over year, versus ~$440M for non-AI companies — a 5× gap that holds even after excluding OpenAI and Anthropic.

What this means for you: The supercluster effect compounds. If you're building AI infrastructure or an AI-native application with ambitions to raise a Series A or B, the gravitational pull of Bay Area hiring, investor density, and customer access is stronger than it has ever been. The question is less "should I be there" and more "how long can I afford not to be."

Elad Gil on 13 things he's watching at the AI frontier

Published 2026-04-20 2

Four days later, Gil published what he called "human idea slop & random thoughts" — 13 numbered observations, each worth its own essay. Here are the ones with the most direct bearing on early-stage decisions.

1. AI is already a significant fraction of the economy, and growing fast. OpenAI and Anthropic each have revenue run rates of roughly $30B — about 0.1% of U.S. GDP ($30T) each. AI overall (including cloud services) is running at 0.25–0.5% of GDP. "This is insanely fast," Gil writes. 2 If the two leading labs hit $100B revenue by end of 2026, AI would represent roughly 1% of GDP.

2. Memory supply will cap model progress through 2028 — and that might actually help you. GPU compute buildout is bottlenecked by SK Hynix, Samsung, and Micron's HBM memory production capacity. 2 Gil's read: this likely preserves the LLM oligopoly structure until around 2028, barring an algorithmic breakthrough. For application-layer founders, this matters — the frontier model landscape you're building on today is probably stable for 18–24 months. Plan around it rather than waiting for a disruption that may not arrive on your timeline.

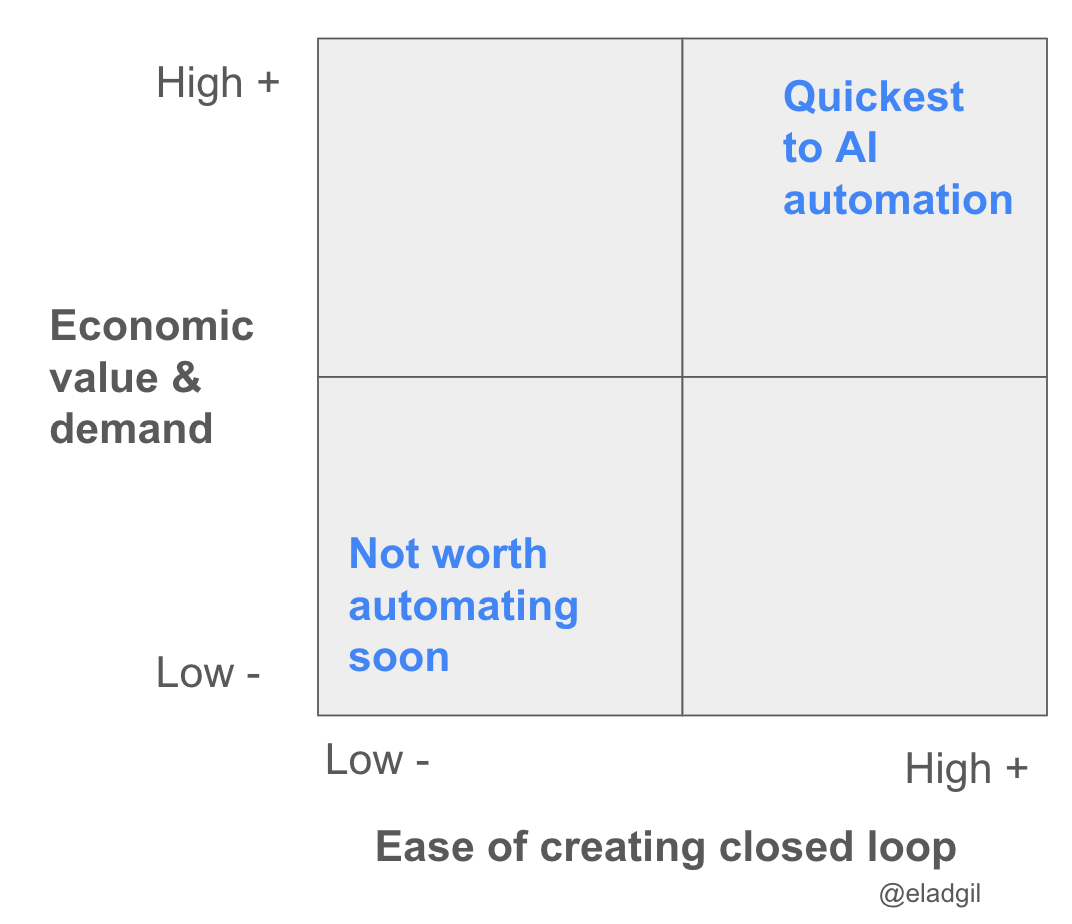

3. "AI will eat closed loops first." This is Gil's most useful framing for thinking about where AI displacement moves fastest.

The logic: AI accelerates fastest in domains where there's a tight feedback loop for judging whether output is correct. Code is the canonical example — you run tests, the answer is right or wrong. 2 When you're deciding which workflows in your company to automate first, ask: does this task have a closed feedback loop? If yes, it's ready to automate now.

4. "Selling work, not software." The framing Gil uses: AI companies aren't selling seats or licenses, they're selling units of labor. 2 Zendesk sells customer service agent seats; Decagon and Sierra (AI customer service companies) sell customer service outcomes. This unlocks markets that traditional software never reached. If your pricing model still looks like SaaS, it's worth asking whether you're leaving TAM on the table.

5. Most AI companies should consider exiting in the next 12–18 months. Gil draws the analogy to 1995–2001: roughly 2,000 internet companies went public, and fewer than twenty built durable businesses. 2 His view is that the few companies that clearly should not exit (OpenAI, Anthropic) are obvious outliers. If you're not obviously in that category, the window for a well-timed acquisition or secondary is open now, and may not stay open.

Sam Altman on AGI, a Molotov cocktail, and the ring of power

Published 2026-04-10 3

At 3:45 AM on April 10, someone threw a Molotov cocktail at Sam Altman's (OpenAI co-founder and CEO) San Francisco home. It bounced off the house and no one was hurt. The suspect later made threats outside OpenAI's offices and was arrested. Hours later, Altman published his only blog post of the Feb–May window — structured in three sections, written at 4 AM.

コンテンツカードを読み込んでいます…

The post connected the attack to a 16,000-word New Yorker profile published days earlier. "I have underestimated the power of words and narratives," he wrote. 3 The tweet announcing the post drew 7.04 million views and 15,927 likes. 4

The most analytically useful section is his account of why AI competition gets so ugly: "Once you see AGI you can't unsee it. It has a real 'ring of power' dynamic to it, and makes people do crazy things." 3 His proposed solution — share the technology broadly so no single actor holds the ring — is also the strategic logic behind OpenAI's API and partnerships.

He closed with a call to the industry to "de-escalate the rhetoric and tactics and try to have fewer explosions in fewer homes, figuratively and literally." 3

The reaction from the tech community was split. Supporters argued that apocalyptic AI narratives had already caused real physical harm. Critics pointed out that Altman's own fundraising and AGI framing had helped generate the narrative he was now asking others to dial down. Both readings are fair.

What this means for you: If you're building a public-facing AI product, the backlash gradient is real and steepening — Stanford's 2026 AI Index shows more than half of surveyed users feel nervous about AI products; Gallup finds Gen Z excitement declining while anger rises. 5 How you communicate what your product does, and what it doesn't, is no longer just a marketing question.

Paul Graham on brand as the only moat AI can't dissolve

Published March 2026 6

Paul Graham (Y Combinator co-founder) published "The Brand Age" in March 2026 — his first essay of the year. The argument is compact and worth reading in full.

The case study: Swiss watchmaking. Unit sales collapsed by nearly two-thirds between the early 1970s and early 1980s as Japanese competitors, a 2.7× appreciation of the Swiss franc, and cheap quartz movements hit simultaneously. The handful of surviving makers transformed from precision-instrument companies into luxury brand operations. Revenue recovered; unit sales didn't. The lesson is in that gap.

"Brand is what's left when the substantive differences between products disappear. But making the substantive differences between products disappear is what technology naturally tends to do. So what happened to the Swiss watch industry is not merely an interesting outlier. It's very much a story of our times." 6

Graham's extension: AI accelerates commoditization faster than any prior technology. If a frontier model can replicate your product's core capability in 12 months, the technical moat isn't durable. What persists is the story attached to the product, the trust users extend to the name, and the switching cost of a community.

What this means for you: If your 0-to-1 product is technically differentiated today, that differentiation window is shorter with every foundation model release. The founders who build brand alongside product — not after product achieves scale — will have something AI cannot simply generate.

Jensen Huang and Andy Jassy on the infrastructure bet

Jensen Huang at CMU — Published 2026-05-10 7

Andy Jassy's 2025 Shareholder Letter — Published 2026-04-09 8

On May 10, NVIDIA founder and CEO Jensen Huang delivered the commencement address at Carnegie Mellon University's 128th graduation ceremony — a fitting venue, given CMU's role as one of the original homes of AI research. He described AI as driving "the largest technology infrastructure buildout in human history" and told graduates they were entering the workforce at the beginning of an industrial era, not just a software cycle. 7

Amazon CEO Andy Jassy's shareholder letter, published a month earlier, put numbers to that thesis. Amazon plans roughly $200 billion in capex in 2026, most of it AI infrastructure. 8 AWS AI revenue is already running at over $15 billion annually in Q1 2026 — a number Jassy noted is nearly 260× what AWS itself looked like at the same point in its history. His framing of why: "We're not going to be conservative in how we play this." 8

Jassy also flagged a principle that applies well beyond Amazon: the "straight line was a lie." Most durable tech businesses didn't grow linearly — they learned to redirect trajectories mid-course, sometimes from scratch. The inflection management skill is what separates companies that survive platform transitions from those that get stranded.

What this means for you: When the two largest cloud infrastructure operators are each committing hundreds of billions to AI buildout, the platform you're building on is getting significantly more capable for several years. The question isn't whether foundational compute improves — it's whether your product compounds faster than your competitors can copy it once the compute floor rises for everyone.

Cover image: GenAI unicorn market cap growth 2023–2025 (stacked by city), from Unicorn Market Cap 2026: SF is the GenAI Super Cluster by Elad Gil.

参考ソース

- 1Unicorn Market Cap 2026: SF is the GenAI Super Cluster

- 2Random thoughts while gazing at the misty AI Frontier

- 3Sam Altman personal blog post, April 10 2026

- 4Sam Altman tweet announcing blog post

- 5The Independent: AI backlash from petitions to protests to petrol bombs

- 6Paul Graham: The Brand Age

- 7NVIDIA Blog: Your Career Starts at the Beginning of the AI Revolution

- 8Amazon: CEO Andy Jassy's 2025 Letter to Shareholders

このコンテンツについて、さらに観点や背景を補足しましょう。