www.federalreserve.gov

Bernanke Senate Banking Committee Testimony — April 3, 2008

Full text of Fed Chairman Ben Bernanke's testimony explaining the systemic rationale for the Bear Stearns intervention, delivered three weeks after the deal closed.

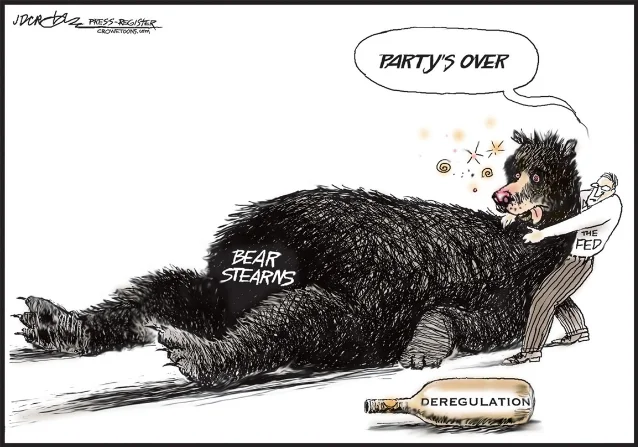

In March 2008, Bear Stearns — the 85-year-old investment bank — collapsed from $172/share to a forced sale at $2/share in 72 hours, rescued through a Fed-brokered deal with JPMorgan Chase backed by a $28.82 billion Maiden Lane LLC facility. This HBS-style case study dissects the negotiation dynamics: the artificially compressed 48-hour window, a five-fold price renegotiation driven by a drafting error and shareholder revolt, and four transferable frameworks on deadline control, BATNA asymmetry, invisible principals, and reference-point psychology.

| Party | Stated objective | Real leverage | BATNA | Hidden constraint |

|---|---|---|---|---|

| Bear Stearns (Schwartz, board) | Find buyer at reasonable price | None — liquidity at zero | Bankruptcy; ~$0/share to shareholders | Bear employees owned >1/3 of stock; personal financial catastrophe for hundreds |

| JPMorgan Chase (Dimon) | Acquire Bear's prime brokerage and clearing assets cheaply | Only credible buyer; controlled the bridge loan | Walk away and let Bear fail | Unknown legal liabilities in Bear's MBS portfolio; $13B+ in future regulatory penalties |

| Fed/Treasury (Geithner, Bernanke, Paulson) | Prevent systemic contagion | Could authorize and fund a deal no one else could | Let Bear fail; face political and economic catastrophe | No legal authority to buy a firm directly; needed private-sector wrapper |

Full text of Fed Chairman Ben Bernanke's testimony explaining the systemic rationale for the Bear Stearns intervention, delivered three weeks after the deal closed.

Añade más opiniones o contexto en torno a este contenido.