Three June 2026 cases: $500, $1,500, $4,440 saved

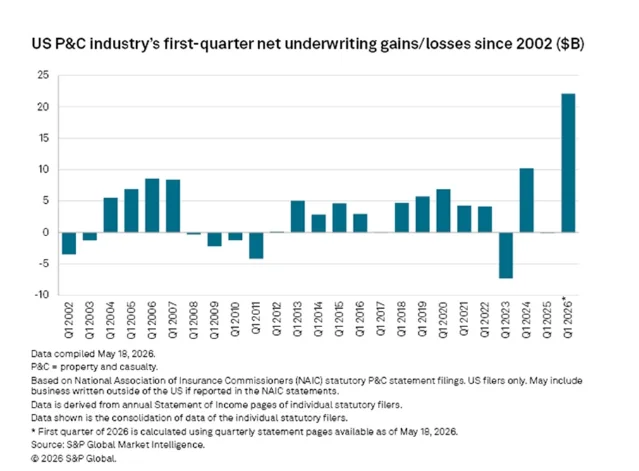

Three near-qualified r/Insurance switch cases from the 60-day expanded window (April 11–June 10, 2026): a Travelers→American Family bundle switch saving ~$500/year that doubled as a textbook retention-department gambit; a New Jersey veteran's NJM→USAA move saving ~$1,500/year on auto; and a decade-long Progressive customer in New York who dropped from $550 to $180/month with Geico. Set against a genuinely softening market: USAA's $500M Florida dividend, all five major FL carriers cutting rates, and the industry's best Q1 underwriting profit in 25 years.

The industry just posted its best first-quarter underwriting profit in 25 years. 1 USAA is writing $500 million in checks to Florida members starting June 15. 2 All five major Florida carriers are cutting rates — not raising them. This is a soft market. There is no better time to pull a competing quote than when insurers are competing for your business.

This week's expanded 60-day window surfaced three publicly disclosed switch experiences — all near-qualified, all missing some details, all presented with explicit gap flags so you know exactly what's verified and what isn't.

Rate climate: the market has shifted

None of the six major carriers — Geico, Progressive, State Farm, Allstate, Liberty Mutual, or USAA — filed a new rate increase in the past 30 days. 1 Instead, decreases filed months ago are now flowing through renewals. The national average full-coverage premium stands at $2,236/year ($186/month) as of June 7, 2026 — essentially flat for the past month. 3

USAA's $500M Florida dividend is the headline event. On June 8, USAA announced it would distribute $500 million to approximately 830,000 eligible Florida members — an average of $760 per qualifying policyholder, with more than a quarter receiving $1,000 or more. 2 Distribution starts June 15. Eligibility covers members who held a Florida USAA auto policy at any point from 2023 through 2025. 4 This dividend is part of a broader $1 billion return to Florida members running from December 2025 through July 2026: USAA already paid $160 million in December 2025 and has cut Florida auto rates twice, saving members $250 million more. 2

CEO Juan C. Andrade attributed the returns to Florida's 2023 tort reform: "As the cost of living rises, we are focused on putting real money back into our members' pockets in multiple ways. From rate reductions to rewards programs and direct returns, our goal is to deliver meaningful, immediate relief while preserving the financial strength our members depend on." 2 Nationwide, roughly half of USAA policyholders will see their six-month auto premium fall in 2026. 2

Florida is the clearest case of market-wide softening. All five carriers that dominate roughly 80% of the Florida market — Allstate, Geico, Progressive, State Farm, and USAA — have filed rate decreases multiple times since January 2025, with average cuts in the double digits. 5 The Florida personal auto liability loss ratio fell to 52.5% in 2025 — the lowest in the state in 15 years and the lowest in the nation. The physical damage loss ratio dropped to 49.5%, down from 112% at its 2022 peak. 5 Those numbers are why carriers are cutting instead of hiking.

State Farm disclosed in a May statement that it cut Illinois auto rates twice over the past year — down 5.7% in July 2025 and down 9.6% in December 2025 — and has reduced auto rates in 40 states over the same period. 6 Michigan lawmakers on June 10 introduced a bill targeting insurance price optimization — the practice of raising premiums based on a policyholder's estimated willingness to pay, not their actual risk. 7 If enacted, carriers could no longer charge loyal customers more simply because predictive models flag them as unlikely to shop.

Three cases from this window

The 60-day window (April 11 – June 10, 2026) produced three publicly disclosed switch experiences from r/Insurance. None clears the full qualification bar — all are missing vehicle details and/or confirmed coverage equivalence at the limit level. Each is presented with its specific gaps clearly labeled.

Case 1: Travelers → American Family, home/auto/umbrella bundle, ~$500/year saved (near-qualified)

What's verified: u/lambertSTL on r/Insurance posted on June 1, 2026. The driver had held home, auto, and umbrella policies with Travelers for three years through an independent agent. After deciding to shop around, they obtained a quote from a local American Family (AmFam) agency and found combined savings of approximately $500/year. 8 Switch path: the driver gave the Travelers agent a heads-up a month before renewal and offered a chance to match. The agent went silent for a week. When she finally responded, her counter-proposal raised deductibles considerably and was still $200 more expensive than AmFam. The driver moved ahead and bound new AmFam policies.

| Travelers (old) | American Family (new) | |

|---|---|---|

| Combined annual savings | ~$500 | |

| Agent counter-offer vs. AmFam | $200 more expensive, higher deductibles |

What's missing: Old and new exact premiums (only the net savings of ~$500 is disclosed). Driver profile (age, state, vehicle). Specific coverage limits. Whether the AmFam policy matches Travelers' limits exactly.

Why this case still matters: $500/year is the lower bound of what makes a switch worth the logistics — and the switch path here is a textbook execution of the retention-department gambit. The driver gave the incumbent agent first right of refusal, documented the unresponsiveness, sent a written cancellation letter as a backup, and moved on. The case also surfaces a real operational trap: after binding with AmFam, the Travelers agent became hostile, Travelers corporate refused to process cancellation without the agent, and the policies nearly auto-renewed with no payment on file. The driver had done everything right — and still had to fight for the exit. If you use an independent agent, build in extra lead time for cancellation logistics. 8

Case 2: NJM → USAA, New Jersey, two vehicles, ~$1,500/year saved on auto (near-qualified)

What's verified: u/No_Will_8933 on r/Insurance posted on June 3, 2026. Two vehicles insured, New Jersey, 20+ year clean record (no accidents, no violations). NJM (New Jersey Manufacturers Insurance) had raised rates twice over two years, adding more than $600 to the annual premium. The driver is a veteran and went directly to USAA: "So — as a vet I go to USAA and get a quote — same coverage $1500 less." 9 The USAA bundle (auto + homeowners) came out slightly less than the prior NJM auto policy alone: "Now — I have auto and homeowners for slightly less than what my auto insurance alone was going to cost me for the upcoming year." 9

| NJM (old) | USAA (new) | |

|---|---|---|

| Annual auto savings | ~$1,500 | |

| Homeowners savings | ~$160 | |

| Auto + homeowners bundle vs. prior auto-only | Slightly cheaper |

What's missing: NJM's exact dollar premium. USAA's exact dollar premium. Vehicle details. Driver age. Specific liability limits and deductibles.

A legitimate concern about this case: u/Ok_Risk_8467, who identified as an insurance professional, pushed back in the thread: "For all we know, USAA gutted your coverage in turn for savings." 9 The OP did not post a declarations-page comparison. Coverage equivalence here is based on the driver's self-report ("same coverage"), not a side-by-side limit comparison. Take this case as a prompt — if you're a veteran in a high-rate state like New Jersey, call USAA for a quote on your current coverage spec. The $1,500 gap is plausible given NJM's recent rate increases and USAA's consistent pricing for eligible members. But verify limits before binding.

USAA eligibility note: USAA requires military affiliation — active duty, veterans, pre-commissioned officers, or qualifying family members. NerdWallet's June 2026 data shows USAA at $1,584/year nationally for full coverage — the cheapest of any major carrier for eligible drivers. 10 ValuePenguin shows USAA at $125/month — the single lowest rate of any carrier in any source reviewed. 11 If you qualify and haven't gotten a USAA quote in the past 12 months, that's the first call to make.

Case 3: Progressive → Geico, New York, ~$4,440/year saved (near-qualified)

What's verified: u/Prevalencee on r/Insurance posted on June 10, 2026, reporting a switch from Progressive to Geico in New York state. Old premium: $550/month (down from $590/month after a prior renewal reduction). New premium: $180/month, quoted immediately when the driver called Geico. Annual savings: approximately $4,440. The driver had been with Progressive for over a decade; relocating to New York triggered a rate explosion that finally prompted a switch. 12

| Progressive (old) | Geico (new) | |

|---|---|---|

| Monthly premium | $550 | $180 |

| Annual premium | ~$6,600 | ~$2,160 |

| Annual savings | ~$4,440 |

What's missing: Vehicle make, model, and year. Driver age. Credit tier. Coverage type (liability-only vs. full coverage) and specific limits. Coverage equivalence is unconfirmed — the post does not state whether the Geico policy matches Progressive's limits.

Why this case still matters: The savings gap is large enough that even if Geico's quote reflects slightly lower limits, the pattern is real. u/Savings-Attitude-295 put the structural problem plainly in the thread: "You never stay with the same company for more than a year max unless you are getting the best deal. They don't give loyalty discount but the other way." 12 A decade with one carrier, with small annual increases the customer barely noticed, compounded into $550/month. Geico quoted $180 on the first call.

One material caution: u/demanbmore, a regular r/Insurance contributor, flagged that this rate may not be final: "Sometimes you get the 'we'd rather not insure you' rate instead of an actual non-renewal." 12 New carriers have 60 days to complete underwriting and adjust the rate after binding. The $180/month quote could change after Geico pulls the MVR, CLUE report, and credit file. If the post-underwriting rate rises but stays below $400, this driver is still ahead.

The four-step pre-flight checklist

Run all four before requesting any quote. Each step is a trap that can erase savings after you've already committed.

Step 1 — Pull your credit score. Credit-based insurance scoring is legal in 46 states. Insurify's June 2026 data shows drivers with excellent credit averaging $131/month for full coverage; poor credit averages $191/month on the same vehicle and coverage. 3 That 46% gap changes which carrier quotes you should prioritize. If your credit tier has improved since your last switch, carriers that weight credit heavily — Geico, Travelers — may now price you better than they did before.

Step 2 — Lock your current coverage limits. Pull your declarations page and write down every field: bodily injury liability per person and per accident, property damage liability, UM/UIM limits, comprehensive and collision deductibles, and any add-ons. A competing quote that drops UM/UIM or cuts liability from 100/300 to 50/100 is not a comparable quote — it's a coverage reduction dressed as savings. u/Clubhouse9 put it simply: "Most of the time when people start searching for their own option they end up with lower limits or missing coverages." 13

Step 3 — Document continuous coverage. A gap of 30 or more days triggers higher-risk pricing at most carriers. Have your current policy's effective dates and a proof-of-prior-insurance letter ready before binding anything new. Insurify data shows a gap can push rates up by as much as 25%. 3 When switching, start the new policy first, then cancel the old — never the other way around.

Step 4 — Protect multi-car and bundle discounts. If you're currently bundling home + auto or have two or more vehicles on one policy, quote the full household at the new carrier — not just the car you want to move. Quoting a single vehicle and switching it will typically break the multi-car discount on the remaining policies, erasing savings before the math even closes. Roslyn Ayers at ValuePenguin offers a relevant data point: "Every year when my policies are up for renewal, I get both separate and bundled quotes for car and home insurance to see which is a better deal. I'm actually saving money by not bundling right now." 11 Bundle discounts are worth checking but not worth assuming.

Quote-shopping path by life stage

Benchmark rates from Insurify, NerdWallet, and ValuePenguin's June 2026 data.

25-year-old single driver. National average: $196/month for full coverage. 3 Geico and Travelers each lead on price in roughly 12 states. 11 Progressive's Snapshot telematics program cuts 10–20% for clean-record young drivers. Auto-Owners ($87/month nationally, available in 26 states) is worth a quote if it operates in your state. 3

30s family, two vehicles. NerdWallet's June 2026 single-car baseline: Travelers $1,664/year, Progressive $2,006/year, Geico $2,055/year. 10 Multi-car discounts run 10–25%. Quote all vehicles and all drivers together — splitting them forfeits the household discount.

50s household, two cars. Average: $122/month nationally. 3 The State Farm → Travelers Kansas case from last issue (65-year-old, gap widening through four renewals) applies directly. USAA-eligible: $1,584/year nationally per NerdWallet. 10

65+ retiree, low mileage. Average: $115/month nationally at 65. 3 Ask each carrier explicitly about low-mileage programs; the standard quote won't reflect your annual mileage unless you volunteer it. Drivers under 7,500 miles/year can see 15–30% reductions. USAA-eligible: $1,584/year nationally per NerdWallet. 10

The retention-department gambit

Before completing any switch, call your current carrier's retention department — not the main customer service line — and give them the best competing quote you've pulled. Name the carrier, the exact coverage limits, and the annual premium. Ask whether they can match it.

Carriers can't technically "price match" — rates are filed with state regulators. What retention departments can do is apply discounts you're not currently receiving: loyalty tiers that weren't triggered automatically, multi-policy adjustments, or telematics enrollment. The gambit works best at or near renewal; many carriers block mid-term pricing changes.

Case 3 this week is a real execution: u/lambertSTL gave the Travelers agent a month's notice and an explicit chance to match. The agent's counter raised deductibles and was still $200 more expensive — which confirmed the switch. If they won't match, set the new policy start date equal to the old policy end date, cancel in writing, and get written confirmation back. Never assume a turned-off autopay equals a cancelled policy. 8

One more option worth knowing: you don't always have to leave. u/Brave-Helicopter113 saved $70/month by calling Progressive and requesting a new policy with the exact same coverage on the same vehicles. "You don't always have to leave your company, just start a new policy with all the same stuff on it." 12 Long-tenure underwriting data can inflate a rate even within the same carrier; a fresh application resets that baseline.

Switches you should not make

Dropping UM/UIM to shave the premium. Uninsured motorist bodily injury (UMBI) pays your medical bills when an uninsured driver causes your injuries — and roughly one in eight U.S. drivers carries no insurance. A 21-year-old hit this week by an uninsured at-fault driver while driving a brand-new 2026 Nissan Sentra found out exactly how that coverage chain works under pressure. 14 u/ektap12 called UMBI "an essential coverage that everyone should carry or you could be left holding the bag if an uninsured person injures you." 15 Don't cut UM/UIM to state minimums to save a few dollars a month.

Switching during an open claim. If you have an active claim, do not switch carriers until it closes. The new carrier didn't underwrite the incident. Changing policies doesn't transfer the claim — it just creates two carrier relationships on the same event. Wait for final settlement.

Accepting a post-bind underwriting surprise without pushing back. New carriers have 30 to 60 days to review their own application data and adjust the rate or cancel. An Allstate customer this window paid in full after switching home, auto, and umbrella — then received a notice demanding removal of a 60-year-old healthy tree or face cancellation. 16 A Massachusetts new driver saw their quote jump from $350/month to $700/month after underwriting corrected their prior-insurance history. 17 You have the right to cancel within the free-look period (typically 14 days) and get your premium back. Compare any revised rate to your old policy and to other quotes before accepting.

Cover image: AI-generated illustration.

Fuentes de referencia

- 1Insurance Journal: U.S. P/C Insurers Post Biggest Q1 Underwriting Profit in 25 Years

- 2USAA Newsroom: USAA Broadens National Effort to Help Military Families Navigate Rising Costs

- 3Insurify: Average Cost of Car Insurance (June 2026)

- 4CNBC: USAA to return nearly $1 billion to Florida members as legal reforms help lower insurance costs

- 5WWSB / MySunCoast: Florida auto insurance rates dropping after 2023 reforms

- 6State Farm Newsroom: Understanding the Issues in Illinois

- 7PropertyCasualty360: Michigan bill targets insurance price optimization

- 8r/Insurance: Unable to Cancel Travelers Policies After Switching to New Carrier

- 9r/Insurance: NJM

- 10NerdWallet: Average Cost of Car Insurance in 2026

- 11ValuePenguin: 10 Cheapest Car Insurance Companies (June 2026)

- 12r/Insurance: Just switched from Progressive($550 a month) to Geico($180 a month)

- 13r/Insurance: Should I leave car insurance broker? I found cheaper plan

- 14r/Insurance: HELP. in a wreck. not at fault, but they don't have insurance.

- 15r/Insurance: Exactly how does uninsured motorist coverage work if you have liability-only coverage? (California)

- 16r/Insurance: Is it common to assess UW risk after quoting? Allstate

- 17r/Insurance: My auto insurance company is trying to increase my premium

Añade más opiniones o contexto en torno a este contenido.